MNI ASIA MARKETS ANALYSIS: Projected Rate Cuts Recede Post Fed

HIGHLIGHTS

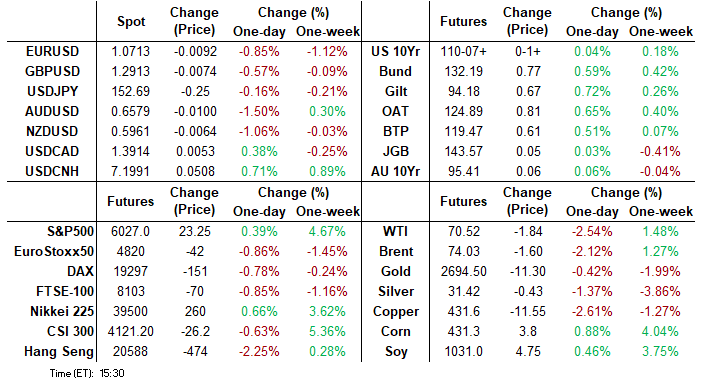

- Treasuries look to finish mixed Friday, curves twisting flatter as short end rates trade weaker the day after the Fed delivered a 25bp cut to maintain the federal funds rate in a target range of 4.5-4.75%.

- U.Mich consumer sentiment improved by more than expected in the preliminary November report -- which did NOT cover past Tuesday's election results.

- The US dollar came firmly back into favor Friday as Trump trades gained renewed confidence, aided by the cleaner positioning following the sharp post-election reversals seen late Wednesday and across Thursday’s session.

- No data Monday in observance of Veterans Day holiday. Cash FI markets closed but open on Globex, NYSE and Nasdaq open as well. Fed speakers resume Tuesday in addition to the Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS)

MNI US TSYS: Curves Twist Flatter Day After FOMC Rate Cut, SLOOS & Fed Speak Tuesday

- Treasuries look to finish mixed Friday, curves twisting flatter (2s10s -7.467 at 4.961; 5s30s -7.229 at 28.347) as short end rates trade weaker the day after the Fed delivered a 25bp cut to maintain the federal funds rate in a target range of 4.5-4.75%.

- Currently, the Dec'24 10Y contract trades +.5 at 110-06.5, well off midmorning high of 110-19.5 after the U.Mich consumer sentiment improved by more than expected in the preliminary November report at 73.0 (cons 71.0) after 70.5, still highest since April.

- There is a big caveat that the survey period ran up to Nov 4 and will have missed the presidential election results. Consumer sentiment showed markedly differing levels by political party, with democrats at 94.9 vs republicans 57.9 ahead of the election.

- The US dollar came firmly back into favor Friday as Trump trades gained renewed confidence, aided by the cleaner positioning following the sharp post-election reversals seen late Wednesday and across Thursday’s session.

- No data Monday in observance of Veterans Day holiday. Cash FI markets closed but open on Globex, NYSE and Nasdaq open as well. Fed speakers resume Tuesday in addition to the Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS).

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00566 to 4.61648 (-0.03552/ wk)

- 3M -0.00546 to 4.51617 (-0.03812/wk)

- 6M -0.00932 to 4.40107 (-0.01091/wk)

- 12M -0.02789 to 4.21872 (+0.02768/wk)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.82% (+0.01), volume: $2.266T

- Broad General Collateral Rate (BGCR): 4.82% (+0.01), volume: $807B

- Tri-Party General Collateral Rate (TGCR): 4.82% (+0.01), volume: $784B

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.83% (+0.00), volume: $102B

- Daily Overnight Bank Funding Rate: 4.83% (+0.00), volume: $285B

FED Reverse Repo Operation:

RRP usage inches up to $163.621B from $159.002B Thursday - this after usage fell to $143.243B on Tuesday -- the lowest since May 6, 2021. The number of counterparties steady at 56 prior.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option traded mixed, put flow two-way as accounts unwound or spread to longer expiries Friday as underlying futures continued to rally in the long end the day after the Fed delivered a 25bp cut to maintain the federal funds rate in a target range of 4.5-4.75%. Moderate volume in SOFR upside calls reported. Curves twisted fatter as short end rates underperformed Friday, Dec24 not fully pricing another 25bp cut: Projected rate cuts into early 2025 compared to late Thursday levels (*): Dec'24 cumulative -11.3bp (-18.7bp), Jan'25 -24.1bp (-28.8bp), Mar'25 -38.3bp (-45.5bp), May'25 -47.3bp (-55.7bp).

SOFR Options

Block, 3,350 SFRX4 95.43/95.50 3x2 put spds, 1.25 net - 2 legs over

Block, 5,226 SFRZ4 95.56/95.68/95.81 put flys, 5.0 vs. 95.59/0.19%

Block: total 10,000 SFRM5 96.50/97.00 call spd vs. 2QM5 97.00/97.50 call spd, 0.25 net on splits, front Jun over

+5,000 SRF5 95.37/95.50/95.62 put tree, 1.75 vs. 95.82/.05%

+5,000 SFRU5/SFRZ5 98.75 call strip, 4.25 db

+7,000 0QZ4 96.25/96.50 1x2 call spds, +3.0 ref 96.215

-5,000 SFRZ4 95.50/95.62 put spds, 5.5 vs 95.575/0.32%

+5,000 SFRZ4 95.43/95.56/95.68 put flys 2.75 ref 95.575

-8,000 SFRZ4 95.62 calls 4.0-3.75 ref 95.575

6,000 SFRM5 96.50/97.00 call spds .5 over 2QM5 97.00/97.50 call spds

6,000 SFRU5 95.62 vs. 2QU5 95.50 put spds, 0.0 Green Sep over

Block, 8,000 0QZ4 96.50/96.75/96.87 broken call flys, 3.5 vs. 96.255/0.10%

2,800 SFRZ4 95.50/95.56/95.62 put trees ref 95.60

5,000 SFRZ4 95.43/95.50 put spds ref 95.60

6,000 SFRH5 96.06/96.18 call spds ref 95.885

3,750 SFRF5 96.00/96.25/96.31/96.50 put condors

2,000 SFRF5 96.12/96.25 call spds ref 95.885

+4,900 SFRG5 95.50/95.62/95.75 put flys, 1.75 ref 95.885

6,000 SFRH5 95.12/95.50 put spds vs. 2QH5 95.50/96.00 put spds, 6.5 net cr/Green March over

Treasury Options

over -16,600 TYZ108 puts, 1 ref 110-11.5

-10,000 USZ4 113 puts, 5

7,500 USZ4 120/122 call spds, 13 ref 117-25

+3,000 TYF5 110.5 straddles, 205

-5,500 TYF5 107.5 puts, 3

-15,000 TYF5 112.5 calls, 21 to 19

+10,000 TYZ4 107.5/108.5 put spds, 3

+20,000 TYZ4 107 puts, 1 ref 110-10.5

2,000 FVZ4 106.5/107.5 2x1 put spds ref 107-02.25

Block, 4,000 TYZ4 109.25/110.25 2x1 put spds, 12 ref 110-13

3,700 TYZ4 108/108.5/109.5/110 put condors

3,000 TYZ4 111.25/111.75/112.5 broken call trees, ref 110-15.5

-4,000 TYZ4 110.25 straddles, 107

over 7,700 TYZ4 112.5 calls, 3 last

+10,000 TYZ4/TYF5 108.5 put calendar spd, 20 ref 110-16

+10,000 TYZ4/TYF5 109 put calendar spd, 24 ref 110-18/0.12%

-20,000 TYZ4 109 puts, 6

-10,000 TYZ4 108.5 puts, 3

4,500 Wednesday wk2 FV 106.5 puts, 3.5-4 ref 107-03.5

+5,000 TYF5 115 calls, 5 ref 110-12

-3,000 TYZ4 107.5/108.5/109.5 put flys, 7 ref 110-08.5

EGBS: Bund futures remain underpinned after a lack of upside surprises in China’s latest stimulus package. Futures are +85 at 132.27, climbing above Wednesday’s post US election high of 132.22 late Friday to October 30 levels.

- German political and fiscal risk provided the fundamental catalyst for the latest leg of the swap spread tightening move on Thursday, as speculation surrounding the potential for higher issuance and a debt brake tweak increased.

- The removal of fiscal hawk Lindner has shifted the probability distribution a little, even with the fiscally conservative Merz’s CDU in the best position to lead the next government.

- Ultimately, our political risk team has pointed to relatively low odds of a debt brake tweak, given current expectations surrounding the next government.

- Back to swap spreads; 10-Year Bund vs. 3-month Euribor ASW has briefly traded back to 0bp after yesterday’s clean break below. While valuation constraints are helping limit further tightening in Schatz spreads, sell-side names generally remain cautious when it comes to spreads further out the curve.

MNI FOREX: Greenback Finishes Week on Front Foot, AUD & EM FX Sharply Lower

- The US dollar came firmly back into favour Friday as Trump trades gained renewed confidence, aided by the cleaner positioning following the sharp post-election reversals seen late Wednesday and across Thursday’s session.

- Accordingly, AUDUSD is the notable underperformer, declining 1.7% and erasing the entirety of yesterday’s advance in the process. The moves come amid a marginally disappointing China stimulus announcement and despite the ongoing strength for US equity benchmarks, highlighting the specific sentiment towards the greenback.

- Similar sentiment has been prominent across emerging market currencies and a sharp 2.5% bounce for USDMXN into the close is evidence of the peso’s significant volatility this week, which traded in a 5% range.

- Overall, the euro has weakened roughly 1.25% against the dollar this week, primarily driven by this more optimistic USD price action in anticipation of a Donald Trump led administration. However, the single currency has shown relative underperformance across G10, largely owing to Eurozone growth concerns and an escalating political crisis in Germany. Bearish technical conditions dominate, signalling scope for an extension towards 1.0666, the Jun 26 low.

- The single currency weakness can also be seen through the lens of EURGBP, which looks set to close at its lowest level since April 2022. 0.8300 marks a multi-year inflection point for the cross and will be monitored closely in coming sessions.

- Next week’s focus will be on US inflation data, as well as a plethora of China and Uk economic data releases.

MNI OPTIONS: Expiries for Nov11 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0700(E530mln), $1.0780-00(E1.1bln), $1.0850-70(E1.2bln), $1.1050-70(E1.7bln), $1.1100(E1.6bln)

- AUD/USD: $0.6650(A$608mln)

- USD/CAD: C$1.3740($1.3bln), C$1.4065($1.4bln)

MNI US STOCKS: Late Equities Roundup: Extending Record Highs Into Weekend

- Profit taking in Materials, Communication sectors was not enough to stem the tide of support for broader indexes as they continued to climb to record highs late Friday. Currently, the DJIA trades up 391.95 points (0.9%) at 44122.84, S&P E-Minis up 31.5 points (0.52%) at 6035.5, Nasdaq up 34.9 points (0.2%) at 19305.35.

- Real Estate and Utility sectors continued to lead gainers in late trade, estate management stocks supporting the Real Estate sector: CBRE Group +3.60%, CoStar Group +1.35%. Residential and specialized REITs also traded strong Friday: Camden Property Trust +3.47%, Mid-America Apt Community +3.44%, AvalonBay +3.06%.

- Independent power providers buoyed the Utility sector: Vistra +3.99%, Ameren Corp +3.83%, CenterPoint Energy +3.44%.

- As noted, profit taking in Materials, Communication Services sectors weighed on broader markets. Metal and mining stocks weighed on the Materials sector: Freeport-McMoRan -5.52%, Celanese -4.27%, Dow Inc -4.05%.

- Interactive media and entertainment stocks scaled back from Thursday gains: Paramount Global -4.25%, Warner Bros -3.04% while Match Group declined 2.81%.

- The latest earnings cycle is nearly over with a few big names expected next week: Home Depot, Live Nation Entertainment, Hertz, Occidental Petroleum, Skyworks Solutions, Cisco, Walt Disney, Applied Materials, Williams-Sonoma, Copart and Cogent Biosciences.

MNI COMMODITIES: WTI Crude Falls, Precious Metals Decline Amid Dollar Gain

- Crude has extended the fall on the day but is up around 1.3% on the week. The market is weighing any potential impact of new US energy policies, uncertainty around 2025 OPEC+ production, and abating supply risks associated with Hurricane Raphael.

- WTI Dec 24 is down by 2.7% today at $70.4/bbl.

- A bearish theme in WTI futures remains intact, with attention on $65.99, the Oct 1 low, and $64.16, the Sep 10 low and key support.

- Against the backdrop of a stronger dollar today, spot gold has fallen by 0.8% to $2,686/oz, leaving the yellow metal 1.8% lower on the week.

- Despite this week’s dip, UBS analysts say that gold will likely see support as a hedge against the inflationary pressures of higher US government borrowing.

- From a technical perspective, the trend condition remains bullish and the latest pullback is considered corrective.

- Attention is on a key support at $2,647.4, the 50-day EMA. For bulls, a reversal higher would refocus attention on the bull trigger at $2,790.1, the Oct 31 high.

- Meanwhile, silver has underperformed, falling by 2.5% today and 3.8% on the week, to $31.2/oz.

- Copper has also fallen by 2.8% $430/lb, amid disappointment on Chinese stimulus news, which revealed no firm signals of fresh consumption support.

- For copper, initial support is at $422.60, the Nov 6 low, followed by $415.93, a Fibonacci retracement point. Clearance of this level would strengthen a bearish theme.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 11/11/2024 | 0700/0800 | *** | CPI Norway | |

| 11/11/2024 | - | *** | Money Supply | |

| 11/11/2024 | - | *** | New Loans | |

| 11/11/2024 | - | *** | Social Financing | |

| 11/11/2024 | - | DMO quarterly investors/GEMM consultation |