MNI ASIA MARKETS ANALYSIS: Pres Trump Ends Canada Trade Talk

HIGHLIGHTS

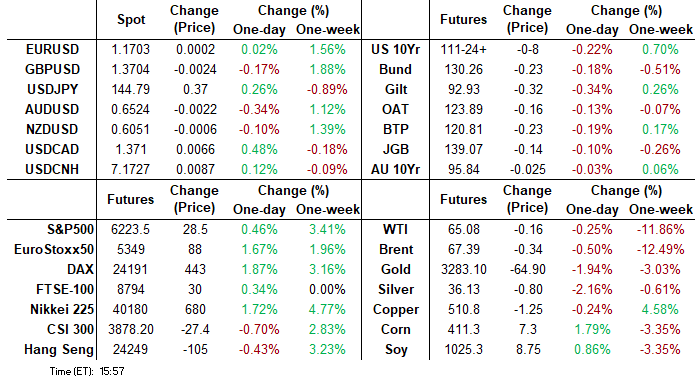

- Treasuries reversed course, look to finish near session lows after Pre Trump terminated trade talks with Canada immediately after the latter imposed a digital tax on US tech companies.

- Stocks didn't like the news either, consolidating after the Nasdaq climbed to new all-time highs late morning, while the US$ index bounced off appr Feb '22 lows.

- Earlier, Tsy Sec Bessent floated kicking the can to Labor day (September 1).

- Short week ahead with Independence day next Friday - that pulls the June employment data forward to Thursday along with weekly claims, Factory orders and S&P services/Composite PMIs.

US TSYS

MNI US TSYS: US$ Rebounds, Tsys & Stocks Retreat After Trump Cans Canada Trade Talk

- Treasuries look to finish near near lows Friday, along with stocks after President Trump unexpectedly announced via social media he would end trade talks with Canada immediately after the latter imposed a digital tax on US tech companies.

- Tsy Sep'25 10Y contract currently trades -7 at 111-25.5 after revisiting early overnight highs of 112-02 in the second half. The tech-heavy Nasdaq index is currently mildly in the red (-9.2 at 20158.80) after managing to climb to new all-time highs ahead midday (20,306.28).

- Markets see-sawed in a narrow range earlier after Pres Trump WH press conference to initially discussing Supreme Court decision on birthright citizenship - Tsys and stocks gained as Trump softened on July 4 tax bill deadline - "Not the end all". Regarding tariff deadline: "WE CAN EXTEND, SHORTEN IT" - softening the July 9 deadline expectations - after Tsy Sec Bessent floated kicking the can to Labor day (September 1) earlier.

- Regarding data: the final University of Michigan consumer survey for May saw a modest downward revision to inflation expectations to still-elevated levels, with slightly better overall sentiment than previously recorded.

- Core PCE inflation came in at 0.179% M/M unrounded in May after 0.136% in April (an upward rev from 0.116% prior), which was higher than expected (consensus roughly around 0.15%, implying a split between 0.1% and 0.2% rounded)) with a higher revision.

- Looking ahead, short week with Independence day next Friday - that pulls the June employment data forward to Thursday along with weekly claims, Factory orders and S&P services/Composite PMIs.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.40% (+0.04), volume: $2.802T

- Broad General Collateral Rate (BGCR): 4.38% (+0.05), volume: $1.104T

- Tri-Party General Collateral Rate (TCR): 4.38% (+0.05), volume: $1.071T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $124B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $282B

FED Reverse Repo Operation

RRP usage climbs to $285.742B this afternoon from $252.242B yesterday, total number of counterparties at 41. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option flow remained mixed/two-way Friday as underlying futures reversed midday highs after Pres Trump tweeted he is ending trade talks with Canada, effective immediately. Trump terminated talks after Canada opted to impose a digital service tax on US tech companies. Projected rate cut pricing, in turn, cooled vs. morning (*) levels: Jul'25 steady at -4.7bo (-5.2bp), Sep'25 at -27.6bp (-27.8bp), Oct'25 at -44.7bp (-45.7bp), Dec'25 at -64.3bp (-65.6bp).

SOFR Options:

+4,000 SFRU5 95.75/95.87 put spds 1.0 over the SFRH6 96.00/96.12 put spd

-4,000 SFRQ5 96.00/96.12/96.25/96.37 call condors, 2.25 vs. 96.265/0.10%

+2,000 SFRU5/Z5/H6/M6/U6 100 call strip

over -30,000 SFRZ5 97.00/98.00 call spds vs. 0QU5 97.50 calls, 0.25-0.0 net/0QU5 over

-4,000 SFRH6 96.50 puts, 26 vs. 96.575/0.42%

+3,000 SFRZ5 95.87/96.25 put spds 14.75 vs 96.30/0.28%

Block: 10,000 SFRN5 96.06/96.18 call spds 1.75 vs. 95.98/0.16%

-2,000 SFRZ5 95.37/95.81 put spd w/ 95.37/95.62 put spd strip, 2.75

3,136 SFRZ6 97.12/98.00 2x1 put spds ref 96.92

2,000 SFRQ5 96.25/96.37 call spds ref 95.98

2,059 SFRZ5 95.37/95.62/95.81 broken put trees ref 96.29

Block. +5,000 0QN5 96.62/96.75 put spds, 2.5 ref 96.885, more on screen

+2,000 SFRZ5 96.06/96.12/96.18/96.25 call condors, 1.0 ref 96.28

Block, 3,000 0QZ5 97.00/97.31 call spds 10.0 ref 96.92

Treasury Options:

+14,000 TYQ5 111 puts, 22 ref 111-29.5

-10,000 FVQ5 109/109.5/110/110.5 call condors, 7.5ref 108-30.25

+15,000 TYU5 114 calls, 25 ref 112-01

Block, +20,000 TYU5 115 calls, 15 vs. 112-02.5/0.05%

5,000 TYQ5 111/112/112.5 broken put trees, 9 net ref 111-23.5

10,000 TYU5 108/110 put spds, 16 ref 111-30

2,000 TYU5 108/110/112 put flys, ref 111-26.5 (pre-data)

+5,000 TYU5 107/108 put spds, 3 ref 111-27

-5,000 TYQ5 113 calls, 20

+2,500 TYU5 109 puts, 13

-2,000 TYQ5 112 calls, 45

over -6,600 TYQ5 112.5 calls, 30-33

MNI EGB BONDS: EGBs-GILTS CASH CLOSE: Curves Close Mixed, But End Week Steeper

European yields rose slightly on Friday, with mixed dynamics across curves.

- Core FI was under a bit of pressure in early trade, with factors including higher-than-expected June flash inflation readings for France and Spain, as well as a broader risk-on bid on US trade optimism.

- European yields ticked lower after a weak US personal spending data release, but would spend the rest of the session trading in volatile fashion amid limited volumes.

- In other data, EC economic sentiment was weaker than expected in June, and though French consumer spending beat expectations in May, underlying momentum remains weak.

- Yields closed higher, with the German curve bear flattening and the UK's lightly bear steepening. 2Y - 5Y Gilts outperformed German counterparts, but it was vice versa further down the curve with Bund and Buxl outperforming 10-30Y Gilts.

- Periphery/semi-core EGB spreads tightened modestly.

- For the week, both the UK and German steepened, with Gilts easily outperforming: Germany 2Y +1.0bp/10Y +7.5bp, UK 2Y -8.0bp/10Y -3.3bp.

- Next week sees the remaining flash Eurozone June CPIs (MNI preview here), along with several speakers at the ECB's Sintra Forum.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3.5bps at 1.86%, 5-Yr is up 2.9bps at 2.163%, 10-Yr is up 2.3bps at 2.592%, and 30-Yr is unchanged at 3.07%.

- UK: The 2-Yr yield is up 1.2bps at 3.839%, 5-Yr is up 1.9bps at 3.968%, 10-Yr is up 3.2bps at 4.504%, and 30-Yr is up 1.9bps at 5.272%.

- Italian BTP spread down 0.3bps at 88.1bps / French OAT down 0.2bps at 67.9bps

MNI EGB OPTIONS: More Call Buying In Euribor, Downside In Bund To End The Week

Friday's Europe rates/bond options flow included:

- RXQ5 129p, bought for 27 in 4k

- RXQ5 128.5p, sold at 20.5 down to 20 in 4.8k

- ERQ5 98.125/98.1875/98.25c fly, was bought for 1.25 in 3k

- ERU5 98.1875/98.25cs 1x2, bought for 0.75 in 5k

MNI FOREX: USD Index Near February 2022 Lows, Bounce After Trump Ends Canada Trade Talk

- US$ bounced off near Feb '22 lows after President Trump unexpectedly announcing the end to Canadian trade negotiations via social media, BBDXY +1.87 at 1195.88).

- Softer than expected personal income data from the US offset a marginal uptick for Core PCE prints in May. The mixed data did little to enthuse an already subdued currency market on Friday, with the dollar index just 0.1% firmer on the session.

- Softer-than-expected Japanese data may be moderately boosting cross/JPY to finish the week. Tokyo’s core inflation slowed to 3.1% y/y in June from 3.6% in May. The core-core CPI, which excludes both fresh food and energy and is a key indicator of underlying inflation, also eased to 3.1% y/y in June from 3.3% in May. The likes of EURJPY and CHFJPY have been beneficiaries of this dynamic on Friday.

- Progress for CHFJPY specifically have been notable this week, and today’s advance looks set to extend the pair’s winning streak to seven consecutive sessions. CHFJPY has now rallied over 4% from the June lows to fresh record highs above 181.40.

- Today’s price action bridged the gap to the first notable projection level (from the Apr 25 - May 13 - May 23 price swing) at 181.35. Above here, the next objective is seen at 182.32.

- In emerging markets, the Colombian peso was a notable laggard on Friday following two rating downgrades from Moody’s and S&P.

- Overall this week, the dollar has resumed its downtrend, with the USD index set to close at its lowest weekly level since February 2022. Price action has propelled the likes of EURUSD above 1.17 and GBPUSD above 1.37, while USDCHF continued to plumb fresh 10-year lows and print below 0.8000.

- It is worth highlighting that next week’s US employment report will headline the economic calendar, notably scheduled on Thursday, owing to the July 4th holiday. China PMIs and German inflation data kicks thing off on Monday.

MNI FX OPTIONS: Expiries for Jun30 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1650(E2.4bln), $1.1675(E504mln), $1.1700(E1.7bln), $1.1750(E919mln), $1.1775(E731mln), $1.1800(E1.3bln)

- USD/JPY: Y143.65-85($1.8bln), Y144.85-00($789mln), Y145.35-50($1.3bln), Y146.00($589mln), Y148.40($1.3bln)

- GBP/USD: $1.3600(Gbp541mln)

- AUD/USD: $0.6425(A$836mln)

- USD/CAD: C$1.3600-10($595mln), C$1.3690-05($1.1bln)

MNI US STOCKS: Late Equities Roundup: Off Highs, Trump Ends Canada Trade Talks

- Stocks are paring gains in late Friday trade, reacting negatively to President Trump unexpectedly announcing the end to Canadian trade negotiations via social media.

- Trump announced the termination after Canada put a "Digital Services Tax on our American Technology Companies, which is a direct and blatant attack on our Country. They are obviously copying the European Union, which has done the same thing, and is currently under discussion with us."

- Potentially softer trade policy was telegraphed by Treasury Sec Bessent earlier in the session (could have deals wrapped up by Labor Day) while the Nasdaq climbed new all-time highs amid little fanfare (20,306.28), the SPX eminis still off early December 2024 highs by approximately 60.0 at the moment, the Dow off some 1,335 points for the same period.

- Currently, the DJIA trades up 270.84 points (0.62%) at 43658.18, S&P E-Minis up 8.75 points (0.14%) at 6203.75, Nasdaq up 12.3 points (0.1%) at 20180.49.

- Leading gainers included NIKE - climbing 15.45% amid a production shift away from China, data center REIT Equinix +5.04%, while defense stocks remained supported by Boeing +4.8%, Howmet Aerospace +3.6%. Laggers included Enphase Energy -7.47%, Coinbase Global -5.96%, Palantir Technologies -3.54%, Newmont -4.31% as Gold took a hit Friday (-52.50 at 3275.42) and First Solar -2.51%.

- Reminder, still a couple weeks away - the next earning cycle kicks off with several banks reporting in a couple weeks.

MNI EQUITY TECHS: E-MINI S&P: (U5) Bull Cycle Extends

- RES 4: 6281.12 1.618 proj of the Apr 7 - 10 - 21 price swing

- RES 3: 6277.50 High Feb 19 and a bull trigger

- RES 2: 6249.00 High Feb 21

- RES 1: 6220.75 Intraday high

- PRICE: 6187.00 @ 1455 ET Jun 27

- SUP 1: 6053.30/5952.18 20- and 50-day EMA values

- SUP 2: 5811.50 Low May 23

- SUP 3: 5645.75 Low May 7

- SUP 4: 5500.00 Low Apr 30

The trend condition in S&P E-Minis is unchanged, it remains bullish and this week’s fresh cycle highs reinforces current conditions. Short-term resistance and a bull trigger at 6128.75, the Jun 11 high, has been breached. The clear break confirms a resumption of the uptrend that started Apr 7. The 6200.00 handle has been cleared too, this opens 6249.00, Feb 21 high. Key support is at the 50-day EMA - at 5952.18. A clear break of it would signal a reversal.

COMMODITIES

MNI AMERICAS OIL: WTI crude is slightly higher today, holding within yesterday’s range, and remains set for a net weekly decline. Another possible OPEC+ hike added pressure, though Trump’s comments that he no longer intends to drop sanctions on Iran were supportive.

- The US has discussed the lifting of sanctions on Iran as a possible incentive to begin talks, CNN reports, as an Iranian law comes into place to suspend cooperation with the UN Nuclear watchdog. Iran’s Foreign Minister said no agreement had been reach for the resumption of talks with the US, IRNA said.

- China’s imports of Iranian crude surged in June despite the conflict, vessel tracking shows.

- WTI Aug futures were up 0.3% at $65.52

- WTI Sep futures were up 0.3% at $64.01

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 30/06/2025 | 0600/0800 | ** | Retail Sales | |

| 30/06/2025 | 0600/0800 | ** | Import/Export Prices | |

| 30/06/2025 | 0600/0800 | ** | Retail Sales | |

| 30/06/2025 | 0600/0700 | *** | GDP Second Estimate | |

| 30/06/2025 | 0600/0700 | * | Quarterly current account balance | |

| 30/06/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 30/06/2025 | 0800/1000 | ** | M3 | |

| 30/06/2025 | 0800/1000 | *** | Bavaria CPI | |

| 30/06/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 30/06/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 30/06/2025 | 0830/0930 | ** | BOE Lending to Individuals | |

| 30/06/2025 | 0830/0930 | ** | BOE M4 | |

| 30/06/2025 | 0830/1030 | ECB de Guindos At IADG Conference | ||

| 30/06/2025 | 0900/1100 | *** | HICP (p) | |

| 30/06/2025 | 1200/1400 | *** | HICP (p) | |

| 30/06/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 30/06/2025 | 1400/1000 | Atlanta Fed's Raphael Bostic - MNI Connect | ||

| 30/06/2025 | 1430/1030 | ** | Dallas Fed manufacturing survey | |

| 30/06/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 30/06/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 30/06/2025 | 1600/1200 | *** | USDA Acreage - NASS | |

| 30/06/2025 | 1600/1200 | ** | USDA GrainStock - NASS | |

| 30/06/2025 | 1700/1300 | Chicago Fed's Austan Goolsbee | ||

| 30/06/2025 | 1900/2100 | ECB Lagarde Opening Remarks At Sintra Forum | ||

| 01/07/2025 | 2300/0900 | ** | S&P Global Manufacturing PMI (f) | |

| 01/07/2025 | 2301/0001 | * | BRC Monthly Shop Price Index | |

| 01/07/2025 | 2350/0850 | *** | Tankan | |

| 01/07/2025 | 0030/0930 | ** | S&P Global Final Japan Manufacturing PMI | |

| 01/07/2025 | 0145/0945 | ** | S&P Global Final China Manufacturing PMI |