MNI ASIA MARKETS ANALYSIS: Kevin Hassett In-A-Box

HIGHLIGHTS

- Treasuries look to finish at/near late Tuesday highs with Pres Trump continuing to tease Hassett as Fed Chair pick after stating earlier in the day he would "probably" announce his pick in early 2026.

- Context on the Trump-Hassett headlines: [Listing off people in the room] "I guess a potential Fed chair is here too. I don’t know, are we allowed to say that, potential? He’s a respected person that I can tell you. Thank you Kevin."

- Risk sentiment has stabilised, with the major equity indices in the US tilting in the green, roughly 6% gains for bitcoin and general crypto advances have added to the overall optimistic backdrop.

- Wednesday Data Calendar: Monthly ADP, Import/Export Prices, IP/Cap-U and ISM Services.

US TSYS

MNI US TSYS: Scaling Off Late Session Highs, Trump Teases Chair Pick Again

- Treasuries are see-saw off late session highs as Pres Trump continues to tease the potential Fed chair replacement, inferring Kevin Hassett again (Hassett odds were back to 80% on Polymarket vs 70% earlier today):

- Context on the Trump-Hassett headlines: [Listing off people in the room] "I guess a potential Fed chair is here too. I don’t know, are we allowed to say that, potential? He’s a respected person that I can tell you. Thank you Kevin."

- Treasuries had scale back support following earlier headlines that Pres Trump would wait until early 2026 to "probably" announce Chairman Powell's replacement. Chair Powell's 4Y term ends mid-May 2026.

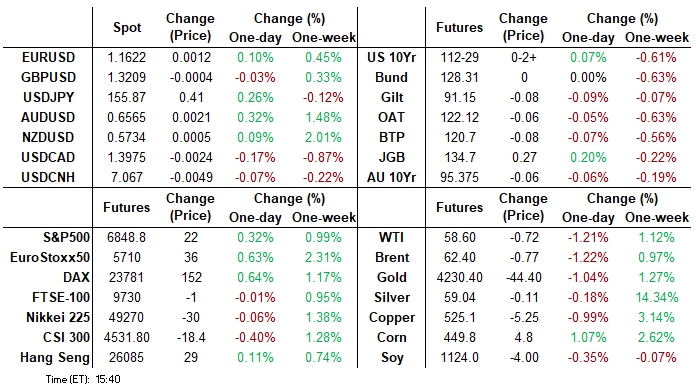

- Currently, TYH6 trades +2 at 112-29 vs. 112-30.5 high. Monday’s move down resulted in a breach of both the 20-day EMA, but more importantly the 50-day EMA at 112-27. A clear breach of this average would undermine a recent bull theme and signal scope for a deeper retracement. A reversal higher is required to refocus attention on the key resistance and bull trigger at 113-29+, the Oct 17 high.

- The Atlanta Fed earlier today released its wage growth tracker for September, with a longer delay than would usually be the case after the delayed BLS payrolls report on Nov 20. It held steady at 4.1% Y/Y for a third consecutive month, as always reflecting the three-month average of median hourly wage growth.

- Wednesday Data Calendar: Monthly ADP, Import/Export Prices, IP/Cap-U and ISM Services.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.12% (+0.00), volume: $3.454T

- Broad General Collateral Rate (BGCR): 4.07% (-0.01), volume: $1.299T

- Tri-Party General Collateral Rate (TCR): 4.07% (-0.01), volume: $1.270T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.89% (+0.01), volume: $85B

- Daily Overnight Bank Funding Rate: 3.89% (+0.01), volume: $151B

FED Reverse Repo Operation

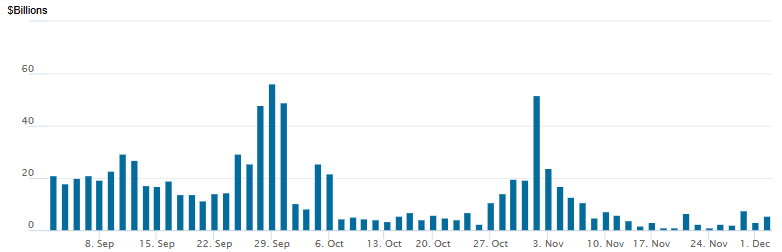

RRP usage rises to $5.620B with 11 counterparties this afternoon from $3.240B Monday. Compares to last Tuesday November 18: $0.905B - lowest level since mid-March 2021; this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options revolved around low delta structures Tuesday with a notable return of par (and above) call options hedging rate cuts to 0.0 by late 2026. Underlying futures spent all session grinding off early session lows as Trump continued to tease his choice for Fed Chair (Hassett) after suggesting an early 2026 annc earlier in session. Curves adding to Monday's bear steepening. Projected rate cut pricing rises vs. late Monday (*): Dec'25 at -24.6bp (-24.7bp), Jan'26 at -31.8bp (-30.6bp), Mar'26 at -39.8bp (-37.8bp), Apr'26 at -46.3bp (-44.1bp).

SOFR Options:

-10,000 SFRZ5 96.18/96.25 call spds 5.25 ref 96.265

Block/screen, +13,000 SFRH6 96.37 straddles 13.75-14.0 over 96.62 calls

+10,000 0QG6 97.12 calls, 8.5 vs. 96.93 to -.935/0.30%

2,000 SFRG6 96.31/96.43 put spds ref 96.445

+5,000 SFRF6 96.50/96.68/96.81 call flys 2.75 ref 96.44

+5,000 SFRH6 96.62/96.81 call spds, 2.5 ref 96.44

-20,000 0QF6 97.00/97.25 call spds, 6.0 ref 96.94

+5,000 SFRF6 96.62 calls, 2.25 ref 96.435

2,000 SFRZ5 96.18/96.25/96.31 put flys, 2.75

Block, 5,000 SFRG6 96.37/96.43 call spds, 2.5

+10,000 SFRG6 96.37/96.43 call spds, 2.5 ref 96.43

+2,500 SFRH6 96.31/96.56 strangles, 9.0

Update, +7,000 SFRH6 96.37 straddles vs. 96.62 calls, 13.75 net ref 96.43

2,500 SFRH6 96.75/97.00 call spds, 1.75 ref 96.435

2,000 2QM6 95.87/96.37 put spds vs. 95.75/96.25 put spds, 6.25 net bear steepener

2,000 0QH6 96.50/96.75 3x2 put spds ref 96.92

5,700 SFRG6 96.31/96.37/96.43/96.50 put condors

5,000 SFRF6 96.50 calls, 2k spd vs. 96.56 calls

over 9,800 SFRZ5 96.25 calls, 3.5 last

Block/screen 11,690 SFRF6 96.43/96.56/96.68 call flys

6,500 SFRM6 96.31 puts ref 96.66

3,400 SFRU6 99.00/100 call spds

1,200 SFRZ6 99.00/100.0/101 call flys ref 96.91

Treasury Options:

10,000 FVF6 107.5/108 2x1 put spds

10,000 wk2 TY 112.25 puts, 8

appr 10,000 TYZH6 114 calls ref 112-24.5 to -25

over 3,000 TYH6 112 puts, 43 last

2,000 FVH6 109.75calls, 14.5 last

1,350 USH6 100 puts ref 116-07

1,500 TYG6 111/112 put spds ref 112-27

MNI FOREX: USDJPY Extends Bounce Amid Stabilising Risk Sentiment

- With little meaningful data on the global economic calendar Tuesday, risk sentiment has stabilised, with the major equity indices in the US tilting in the green. Furthermore, roughly 6% gains for bitcoin and general crypto advances have added to the overall optimistic backdrop. These dynamics have done little to move the needle for the USD index, which has spent the session consolidating the strong reversal off the lows yesterday.

- Price action across G10 FX has been muted, keeping volumes light across the board (EUR futures had posted ~65% of the volumes you'd expect to see towards the European close), contrasting with Monday's busier price action. After printing within 4 pips of key 1.1656 resistance yesterday, EURUSD has pulled back towards the 1.16 handle, of which we have been oscillating around on Tuesday.

- The Japanese yen is the weakest currency across the G10 amid the firmer risk backdrop, allowing USDJPY to consolidate its near 1% recovery from yesterday’s lows. The price action this week has created some false breaks on the chart, keeping bullish Cross/JPY conditions intact, for now. We pointed out that the adjustment of rate hike pricing between Jan and Dec meetings should have little lasting impact on yen sentiment, with broader risk conditions, domestic fiscal developments and China-Japan tensions more likely to drive the narrative.

- AUD's moderate strength is worth noting, and means AUDUSD has printed seven consecutive sessions of higher highs, narrowing the gap with 0.6580 in the process - the next notable resistance. One primary driver of AUD strength is the continued pullback in front-end vols. G10 FX vol has been sold firmly off the November peak, but 1m implied AUD vols are now the lowest of the year and the second lowest level since the onset of COVID in 2020.

- It’s a busier docket on Wednesday, with RBA Governor Bullock speaking before Australian Q3 GDP. Swiss CPI will then precede US ADP employment and ISM Services PMI data.

MNI OPTIONS: Expiries for Dec03 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E611mln), $1.1625(E697mln)

- EUR/GBP: Gbp0.8885(E505mln)

- NZD/USD: $0.5730(N$622mln)

MNI US STOCKS: Late Equities Roundup: IT, Industrials, Financials Lead Advances

- Stocks are trading firmer Tuesday, inside session ranges after scaling off midmorning highs. Currently, the DJIA trades up 181.94 points (0.38%) at 47474.58, S&P E-Mini Futures up 13.5 points (0.2%) at 6840.25, Nasdaq up 152 points (0.7%) at 23429.77.

- Trading desks offered several reasons for the improved sentiment including a rebound in Bitcoin prices, a rebound in JGBs following a strong 10Y auction overnight and general short covering/position squaring ahead of Wednesday's S&P Global US Services PMI and ISM Services Index data.

- Information Technology, Industrials and Financials sector shares continued to lead advances in late trade:

- Intel Corp +8.01%, NXP Semiconductors +7.26%, Teradyne +6.26%, Microchip Technology +5.20%, Texas Instruments +4.63%, Applied Materials +4.29% and HP +4.28%.

- Boeing +9.37%, GE Vernova +5.35%, United Airlines Holdings +3.87%, Generac Holdings +3.20% and JB Hunt Transport Services +2.96%.

- E-currency rebound buoyed: Coinbase Global +3.83%, Robinhood Markets +3.72%, Global Payments +3.66% and Capital One Financial +1.45%.

- Conversely, Energy and Materials sector shares continued to lead declines in the second half, partially tied to weaker crude price action (WTI -.72 at 58.60): Targa Resources -2.27%, EQT Corp -2.16%, Williams Cos Inc -1.79%, Expand Energy -1.78% and Marathon Petroleum -1.77%.

- Meanwhile, the following weighed on the Materials sector: Packaging Corp of America -5.48%, Smurfit WestRock -3.79%, International Paper -3.65%, Mosaic -3.27% and Newmont Corp -2.33%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Bullish Outlook

- RES 4: 6953.75 High Oct 30 and bull trigger

- RES 3: 6900.50 High Nov 12

- RES 2: 6852.56 76.4% retracement of the Oct 30 - Nov 21 bear leg

- RES 1: 6864.50 High Dec 1

- PRICE: 6832.50 @ 1350 ET Dec 2

- SUP 1: 6674.50/6525.00 Low Nov 25 / 21

- SUP 2: 6500.00 Round number support

- SUP 3: 6476.62 23.6% retracement of the Apr 7 - Oct 30 uptrend

- SUP 4: 6427.00 Low Sep 2

S&P E-Minis are holding on to their recent gains following the recovery from the Nov 21 low. The climb has resulted in a breach of the 20- and 50- day EMAs. This highlights a bullish development and the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would signal scope for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low.

MNI COMMODITIES: WTI Futures Trade Back to Unchanged on Week

- Crude futures experienced a volatile session, but have trended lower on the session. This has brought front-month WTI back to unchanged on the week, around the $58.60 mark. A further resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low.

- There was a momentary spike for oil prices amid headlines from Russian President Putin who stated that European demands are not acceptable for Russia, and that Russia will increase strikes on facilities and Ukrainian vessels and take measures against tankers of countries which help Ukraine.

- However, prices have since resumed a moderate bearish pathway amid hopes that negotiations with the US, led by Special Envoy Steve Witkoff, may prompt some progress regarding peace talks.

- A U.S. military build up off Venezuela and its deadly attacks on small boats is also keeping tension high, supporting a risk premium even as supply from OPEC+ and elsewhere is higher than demand, pressuring oil lower as global inventories climb. President Donald Trump suggested the Pentagon will soon start targeting drug cartels with strikes on land in Venezuela, however, oil prices have not bee impacted by the latest headlines.

- Separately, the decline in Russian oil flows to India may only be for a brief period as Moscow plans to boost supplies Kremlin spokesperson Dmitry Peskov told Indian journalists on Tuesday.

MNI PRECIOUS METALS: Gold-Silver Ratio Prints Four-Year Lows

- Expectations firming for a likely Fed cut next week have helped precious metals to reaffirm their bullish overall themes. The strong bounce for both gold and silver from their respective lows in October suggests the bear phase between Oct 20 and 28 appears to have been a correction.

- Initial USD weakness early Monday allowed spot gold to extend gains, reaching as high as $4,264/oz, a fresh recovery high. However, intra-day momentum then stalled amid the broader recovery for the US dollar, and this dynamic has continued to weigh on gold Tuesday. Price traded as low as $4,163.95/oz and despite recovering towards $4,200, spot remains down 0.89% on the session. 20- and 50-day exponential moving averages provide the notable supports, intersecting at $4,116 and $4,001 respectively.

- Meanwhile, spot silver is looking set to extend its impressive winning streak in recent days. Although today’s highs fell short of fresh record highs, a winning session today would be seven consecutive daily advances. BNP noted yesterday that investors will be watching how expensive silver is getting relative to gold. The gold-silver ratio has notably broken below the 2024 lows today, placing the ratio at the lowest levels in over four years.

- It’s mainly projection levels that are used to generate targets for the silver move at this point, and the next notable level is $59.563, a Fibonacci projection.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 03/12/2025 | 0700/0200 | * | Turkey CPI | |

| 03/12/2025 | 0730/0830 | *** | CPI | |

| 03/12/2025 | 0815/0915 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0815/0915 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0845/0945 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0845/0945 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0850/0950 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0850/0950 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0855/0955 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0855/0955 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0900/1000 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0900/1000 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0930/0930 | ** | S&P Global Services PMI (Final) | |

| 03/12/2025 | 0930/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 03/12/2025 | 1000/1100 | ** | EZ PPI | |

| 03/12/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 03/12/2025 | 1030/1130 | ECB Lane Keynote at Banca d'Italia Workshop on Exchange Rates | ||

| 03/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 03/12/2025 | 1315/0815 | *** | ADP Employment Report | |

| 03/12/2025 | 1330/0830 | ** | Import/Export Price Index | |

| 03/12/2025 | 1330/1430 | ECB Lagarde Statement at ECON Hearing | ||

| 03/12/2025 | 1415/0915 | *** | Industrial Production | |

| 03/12/2025 | 1445/0945 | *** | S&P Global Services Index (final) | |

| 03/12/2025 | 1445/0945 | *** | S&P Global US Final Composite PMI | |

| 03/12/2025 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 03/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 03/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 03/12/2025 | 1530/1630 | ECB Lagarde Statement at ECON Hearing (as ESRB Chair) | ||

| 03/12/2025 | 1700/1700 | BOE Mann in Panel on Reserve Currencies | ||

| 04/12/2025 | 0030/1130 | ** | Trade Balance |