MNI ASIA MARKETS ANALYSIS: Japan, S. Korea Tariffs Kick Off

HIGHLIGHTS

- Treasuries gapped higher early Monday after Tsy Sec Bessent alluded to several trade announcements expected over the next 24 hours with "plenty of countries wanting to make deals".

- Rates swiftly pulled back from highs amid a general lack of specifics from the Trump administration.

- Conversely, rates gapped lower, extended lows with equities after Pres Trump announced 25% tariffs on Japan and South Korea Goods.

- Additional announcements included: 25% tariffs on Malaysia and Kazakhstan, 30% on South Africa and 40% on Laos and Myanmar. US$ climbed on the news.

US TSYS

MNI US TSYS: Trump Announces Tariffs via Social Media

- Treasuries look to finish broadly lower - but off midday lows as Pres Trump announced tariffs via social media Monday (that spurred Brazil's Lula to say it is "Irresponsible to threaten tariffs on Social Media).

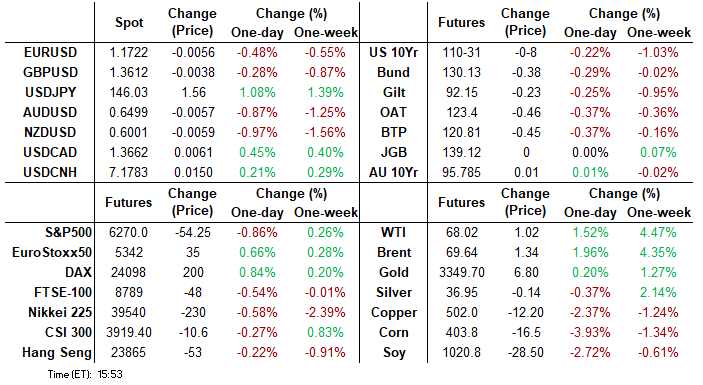

- Currently, Tsy Sep'25 10Y futures trades -7.5 at 110-31.5 (110-29 low / 111-12.5 high), sitting on key support at 110-31, the 50-day EMA, and the Jul 3 low. A clear break of this average would signal scope for a deeper correction and highlight a possible reversal.

- Tsy 10Y yield climbed to 4.3972% high late Monday, curves bear steepened w/ 2s10s +2.512 at 47.473, 5s30s +3.771 at 96.145.

- Tsys had gapped higher briefly early Monday after Tsy Sec Bessent alluded to several trade announcements expected over the next 24 hours with "plenty of countries wanting to make deals" -- but Tsys swiftly pulled back from highs amid a general lack of specifics from the Trump administration.

- Rates extended lows along with equities after Pres Trump announced 25% tariffs on Japan and South Korea Goods. Additional announcements included: 25% tariffs on Malaysia and Kazakhstan, 30% on South Africa and 40% on Laos and Myanmar.

- Price action is bolstered by the USD index respecting its test of long-term trendline support, fostering the subsequent extension to fresh recovery highs.

- No data Monday, limited on tap Tuesday: NFIB Small Business Optimism at 0600ET, Consumer Credit at 1500ET, Tsy bills and $58B 3Y Note auction (91282CNM9) at 1300ET. Main focus on Wednesday's FOMC minutes for the June meeting.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.35% (-0.04), volume: $2.846T

- Broad General Collateral Rate (BGCR): 4.32% (-0.05), volume: $1.140T

- Tri-Party General Collateral Rate (TCR): 4.32% (-0.05), volume: $1.109T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $129B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $277B

FED Reverse Repo Operation:

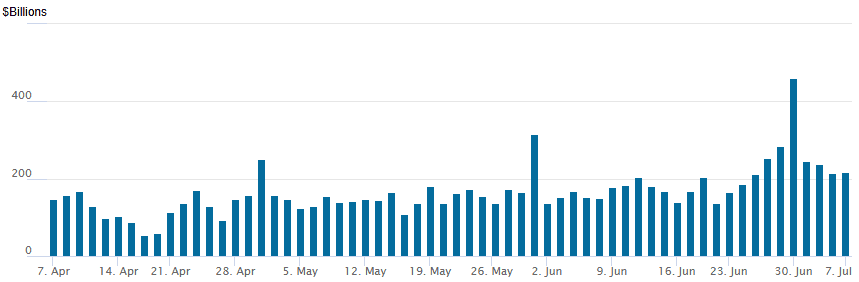

RRP usage inches up to $218.030B this afternoon from $214.665B last Thursday, total number of counterparties at 37. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to yesterday's (July 1) $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option flow remained mixed Monday, mostly bullish (call buying, put unwinds) with a couple exceptions like the large Sep'25 10Y put skew buyer. Underlying futures broadly weaker but off midday lows, curves steeper with the short end outperforming. Projected rate cut pricing has consolidated vs morning (*) levels: Jul'25 at -1.2bp, Sep'25 at -17bp (-18.9bp), Oct'25 at -32.2bp (-34.7bp), Dec'25 at -49.8bp (-53.0bp).

SOFR Options:

-4,000 SFRU5 95.75/96.12 put over risk reversals, 0.5

6,500 SFRZ5 96.31/96.37 call spds

+10,000 SFRZ5 97.18 calls, 3.25 ref 96.17

-4,000 3QZ5 95.75 puts, 5.5 vs. 96.465/0.16%

-1,000 SFRN5 95.87 straddles, 3.75

+8,000 SFRV5 96.25/96.50/96.75 call flys, 3.0

-1,000 SFRV5 96.18/96.43 strangles, 23.75

+2,500 SFRM5 96.75/97.25 call spds vs. 0QM 97.25 calls, 1.0 net

Block/screen 8,000 SFRV5 96.06/96.18/96.31/96.43 call condors, 3.25

1,850 SFRU5 95.87 put vs. 95.93/96.12 call spd ref 95.88

Block, 5,000 SFRV5 96.12/96.18/96.31/96.43 broken call condors, 0.0

+2,000 SFRH6 96.50/97.00 call spds, 13.5 ref 96.43

2,100 SFRN5 95.75/95.81/95.87 put trees, 1.5

3,336 SFRZ5 95.75/95.87/96.25/96.37 put condors, 6.5 ref 96.21/0.05%

Treasury Options:

-20,000 TYU5 113 calls vs. 109/110 put spds 1 net ref 111-00.5

Block, 10,000 TYU5 113.5 calls, 13 vs. 111-02/0.05%

5,000 TYU5 109.5 puts, 21 ref 110-31.5 to -30.5

1,000 FVQ5/FVU5 108.25 straddle spd

2,500 TYU5 113/113.5 call spds, 1 ref 111-01

6,500 TYQ5/wk2 TY 110.25 put spd, 11 net

2,000 TYV5 122.5 calls, ref 111-04.5

2,400 TUQ5 104.5 calls, 0.5 (exp 7/25)

2,000 TYU5 111.5 puts

-20,000 TYQ5 109.5 puts, 4 ref 111-07

+1,000 TYQ5 111.5/112/112.5 call flys, 4

+1,000 FVQ5 108/108.5 2x1 put spds, 3

MNI BONDS: EGBs-GILTS CASH CLOSE: Weakness Builds Into The Close

Bunds slightly underperformed Gilts Monday.

- Yields started the session by edging lower. Eurozone retail sales came in weak, though German industrial production was surprisingly solid versus last week's factory orders data.

- Core FI would weaken over the course of the rest of the European session, with oil prices and equities edging up, albeit amid light volumes. Yields closed at the session highs.

- Just after the cash close, however, we saw a bounce in Bund and Gilt futures after US President Trump announced the imposition of 25% tariffs on South Korean and Japanese imports.

- The German and UK cash curves both bear steepened on the day.

- Periphery / semi-core EGB spreads closed slightly wider, with BTPs underperforming.

- Tuesday's central bank speaker slate is quiet, with only an appearance by ECB's Nagel. In addition, we get German trade data.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.1bps at 1.837%, 5-Yr is up 3.6bps at 2.161%, 10-Yr is up 3.6bps at 2.643%, and 30-Yr is up 3.1bps at 3.118%.

- UK: The 2-Yr yield is up 1.2bps at 3.864%, 5-Yr is up 2bps at 4.011%, 10-Yr is up 3.2bps at 4.586%, and 30-Yr is up 4.8bps at 5.391%.

- Italian BTP spread up 1.2bps at 84.8bps / French OAT up 0.5bps at 67.8bps

MNI EGB OPTIONS: Varied Call Structure Buying Across Euribor And Sonia Monday

Monday's Europe rates/bond options flow included:

- RXU5 127.5/125.5ps, sold at 15 in 1.5k

- ERU5 98.25/98.37cs, bought for 0.75 and 1 in 4k

- ERZ5 98.25/98.12/97.87p ladder sold at 4 in 2.5k

- ERM6 98.0625/98.1875/98.625/98.75c condor vs 97.75p, bought the condor for 1.5 in 2k

- 2RH6 97.75/97.25ps 1x4, bought the 4 for 4.5 in 2.25k (sold the 1)

- SFIQ5 96.20/96.30/96.40c fly, bought for 1 and 1.5 in 15k total

- SFIV5 96.10/96.20/96.30c fly, bought for 1.5 in 6k

- SFIV5 vs SFIX5 96.70 calls. Pays 1.5 to buy the X5 in 5.7k

MNI FOREX: Greenback Extending Recovery Amid Tariff Developments

- Trepidation surrounding renewed tariff concerns has boosted US dollar sentiment on Monday, allowing the USD index to extend its most recent recovery. Price action is bolstered by the USD index respecting its test of long-term trendline support, fostering the subsequent extension to fresh recovery highs.

- The bear steepening move for the treasury curve and late weakness for equities are providing the dominant drivers for FX in late trade, while last week’s stellar US payrolls data may also be underpinning the renewed greenback optimism.

- Initial dynamics weighed significantly on the likes of AUD and NZD Monday, although as the session has progressed the Japanese yen and some EM currencies have been notable laggards. The latest posts via truth social on the intended 25% tariffs on Japan and South Korea have exacerbated the weakness for the JPY and KRW.

- For USDJPY, session gains currently stand at 1.13% as we approach the APAC crossover. Spot ramped higher following the breach of the 50-day EMA, at 144.91, and the clean break has prompted a significant narrowing of the gap to 146.19, the Jun 24 high.

- The late extension of dollar strength also prompted EURUSD to slip back below 1.17, a post-payrolls low, tracking towards key short-term support to watch lies at 1.1630, the 20-day EMA.

- Separately, Trump's ire toward BRICS countries has tilted EM FX to underperform to start the week. Higher beta ZAR and BRL have notably depreciated after the President warned there would be "no exceptions" to a policy of 10% additional trade tariffs on nations that adhere to the BRICS' anti-American policies. CLP and COP are also extending losses to over 1.5% on the session.

- Tuesday’s focus turns to the RBA decision, where consensus sees the board delivering a 25bp rate cut to 3.60%.

MNI FX OPTIONS: Expiries for Jul08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E1.1bln), $1.1700(E1.3bln), $1.1770-80(E623mln), $1.1810(E710mln)

- USD/JPY: Y142.60-75($1.1bln), Y146.60($551mln)

- AUD/USD: $0.6435(A$646mln), $0.6545-50(A$563mln)

MNI US STOCKS: Extending Lows Yet Again on More Tariff Tweets

- Stocks extend late session lows after latest tariff announcements via Pres Trump's social media platform: 25% on goods from Malaysia and Kazakhstan, 30% on South Africa, and 40% on Laos.

- Currently, the DJIA trades down 664.11 points (-1.48%) at 44163.91, S&P E-Minis down 76.5 points (-1.21%) at 6247.5, Nasdaq down 265.4 points (-1.3%) at 20335.29.

- Energy, Consumer Discretionary, Materials, Financials and Health Care sectors underperforming.

- Main laggers in the second half include: Tesla -7.01%, First Solar -4.39%, Dow Inc -4.22%, Lululemon Athletica -4.21%, EOG Resources -3.74%, Halliburton -3.62%, Old Dominion Freight Line -3.58% and Albemarle Corp -3.53%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Bulls Remain In The Driver’s Seat

- RES 4: 6402.44 1.382 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6381.00 1.764 proj of the Apr 7 - 10 - 21 price swing

- RES 2: 6356.12 1.236 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6333.25 High Jul 3

- PRICE: 6264.00 @ 1450ET Jul 7

- SUP 1: 6235.50 Low Jul 2

- SUP 2: 6138.46/6000.73 20- and 50-day EMA values

- SUP 3: 5811.50 Low May 23

- SUP 4: 5645.75 Low May 7

The trend condition in S&P E-Minis is unchanged, it remains bullish. Resistance at 6128.75, the Jun 11 high, has recently been breached. The break confirmed a resumption of the uptrend that started Apr 7. This has been followed by a breach of key resistance and a bull trigger at 6277.50, the Feb 21 high. Sights are on 6356.12, a Fibonacci projection. Key support is at the 50-day EMA, at 6000.73.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 08/07/2025 | 0500/1400 | Economy Watchers Survey | ||

| 08/07/2025 | 0600/0800 | ** | Trade Balance | |

| 08/07/2025 | 0645/0845 | * | Foreign Trade | |

| 08/07/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 08/07/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 08/07/2025 | - | ECB de Guindos At ECOFIN Meeting | ||

| 08/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 08/07/2025 | 1400/1000 | * | Ivey PMI | |

| 08/07/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/07/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 08/07/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 08/07/2025 | 1900/1500 | * | Consumer Credit | |

| 09/07/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 09/07/2025 | 0130/0930 | *** | CPI | |

| 09/07/2025 | 0130/0930 | *** | Producer Price Index | |

| 09/07/2025 | 0200/1400 | *** | RBNZ official cash rate decision |