MNI ASIA MARKETS ANALYSIS: Iran/Israel Hostility De-Escalates

HIGHLIGHTS

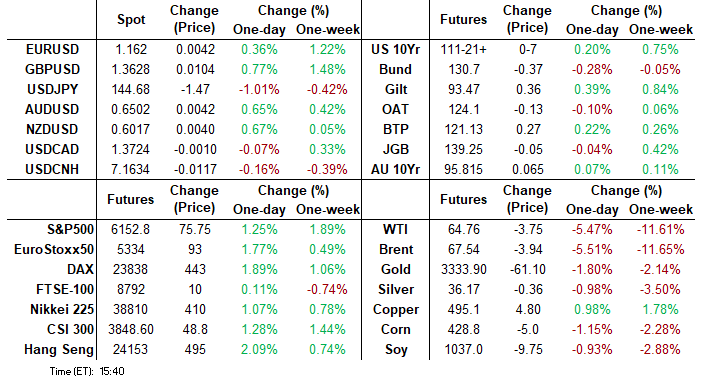

- Treasuries look to finish higher/near late Tuesday highs, partially tied to various Fed speakers leaving the door open to potential rate cuts (projected pricing shows Dec'25 around -60bp).

- Risk appetites improved as Israel/Iran hostilities de-escalate, SPX emini and Nasdaq index have risen to mid-February levels while if the Dow is near early March highs in late trade.

- US$ extended its reversal south that begun late Monday, with the dollar index within close proximity of cycle lows, Gold sold off (-50.90 at 3317.78), as did crude (WTI -4.0 at 64.51).

US TSYS

MNI US TSYS: Iran/Israel Ceasefire Holding, Fed Keeps Rate Cut Door Ajar

- US Treasuries look to finish at/near late Tuesday session highs - support twofold: risk sentiment improved as Israel/Iran hostilities appeared to de-escalate (ceasefire pledges watched closely after some morning confusion over timing).

- Secondary: Fed Chairman Powell's policy testimony to the House this morning - while maintaining patient stance regarding rate cuts, Chair Powell conceded he could see inflation not coming in "as strong as expected", however, "inflation is projected to have moved higher due to tariffs". Meanwhile, a "majority" feel it's appropriate to cut interest rates later this year.

- Projected rate cut pricing largely gaining vs. morning levels (*): Jul'25 at -4.7bp (-5.7bp), Sep'25 at -25.3bp (-24.2bp), Oct'25 at -41.2bp (-39.7bp), Dec'25 at -59.6bp (-56.6bp).

- On data, The Philly Fed non-manufacturing survey saw firms dial back particularly negative views on the regional economy to one closer to their own experiences. The Johnson Redbook retail sales index rose by 4.5% Y/Y in the week ending Jun 21, a slowdown from 5.2% the prior week and bringing month-to-date June sales gains to 4.8% Y/Y (vs a 5.7% gain targeted by retailers).

- Greenback weakness will likely have been bolstered by cleaner short-term positioning, weaker-than-expected US consumer confidence and Fed Chair Powell not ruling out the chance of an FOMC rate cut as soon as July.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.29% (+0.00), volume: $2.740T

- Broad General Collateral Rate (BGCR): 4.27% (+0.00), volume: $1.081T

- Tri-Party General Collateral Rate (TCR): 4.27% (+0.00), volume: $1.055T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $115B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $293B

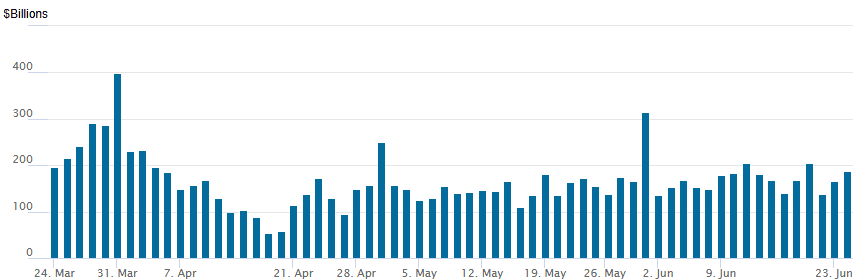

FED Reverse Repo Operation

RRP usage rises to $187.367B this afternoon from $165.319B yesterday, total number of counterparties at 34. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

Decent SOFR option volumes revolved around calls for the most part Tuesday, Treasury options muted. Underlying futures firmer, near top end of the session range as Israel/Iran hostilities appear to de-escalate. Projected rate cut pricing largely gaining vs. morning levels (*): Jul'25 at -4.7bp (-5.7bp), Sep'25 at -25.3bp (-24.2bp), Oct'25 at -41.2bp (-39.7bp), Dec'25 at -59.6bp (-56.6bp).

SOFR Options:

+15,000 SFRU5 95.68/95.75/95.81 2x1x1 put trees, 0.0-0.25

+2,000 SFRZ5 96.25 straddles, 44.5 ref 96.22

+5,000 SFRQ5 96.00/96.12/96.25/96.37 call condors, 1.5 ref 95.915

Block, 10,000 SFRN5 96.00/96.12 call spds 1.75 ref 96.845

+10,000 0QQ5/0QU5 96.50/96.75/97.00call fly strip, 10.5 ref 96.795

+10,000 0QZ5 96.75/97.00/97.50/97.75 call condors, 7.0 ref 96.845

+31,800 0QU5 97.25/97.50 call spds, 3.5

Block/screen, 4,000 SFRQ5 95.75/95.87/96.00 2x3x1 put flys, 1.5 ref 95.935

-6,000 SFRQ5 96.25/96.375 call spds, 1.0 vs 95.96/0.05%

-2,500 SFRN5 95.75/95.87/96.00 put fly, 5.0

+2,500 SFRQ5 96.1875/96.3125 call spd, 1.5

+8,000 SFRN5 96.25/96.375 call spd w/ SFRQ5 96.1875/96.3125 call spd strip, 1.75 total

+2,000 SFRZ5 95.75/96.00 put spd 1.0 over 96.25/96.50 call spd

-3,600 SFRN5 95.75/95.87/96.00 put fly, 5.0 ref 95.935

+10,000 SFRU5 95.875/95.9375 call spd vs SFRQ5 97.00 calls, 1.25

2,500 SFRN5 95.68/95.81 put spds, 0.75 ref 95.935

Treasury Options:

10,000 FVQ5 109/110 call spds ref 108-15.5

Over 26,000 TYQ5 112 calls, 32-40 (Decent volume yesterday: 84.2k pushed OI to 201,774)

+4,000 Mon wk 10Y 111.75 calls, 11 vs. 111-13.5/0.29%

+2,000 TYU5 108/109 put spds, 8 vs. 111-12.5/0.08%

-2,000 TYQ5 112.75 calls 19

MNI BONDS: EGBs-GILTS CASH CLOSE: German Long End Underperforms On Issuance Concerns

European FI traded mixed Tuesday, with Gilts gaining and easily outperforming Bunds, and periphery EGB spreads tightening.

- Germany's Q3 issuance plan was in line with expectations though the curve steepened on indications of possible 50Y issuance, helping pressure the broader FI space. But lower oil prices on the overnight US/Iran/Israel de-escalation helped subdue any short-end yield rise.

- Global core FI regained ground by middle of the European afternoon however, led by Treasuries as Fed Chair Powell was seen to be open to earlier rate cuts if data warranted, while US consumer confidence and labor market indications were weaker than expected.

- In European data, German IFO Business Climate/Expectations beat expectations. There were several central bank speakers, with BOE's Ramsden perceived dovishly, while ECB's Lane drawing headlines for seeing some caution on services disinflation (though nothing really new).

- The German curve bear steepened on the day, with the UK's leaning bull flatter (out to the 10-year segment).

- Periphery/semi-core EGB spreads tightened in a risk-on session, with BTPs outperforming.

- Wednesday sees a quieter central bank communications schedule, with BOE's Lombardelli the lone scheduled speaker, while in data we get French consumer confidence and Spanish GDP/PPI readings.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.3bps at 1.851%, 5-Yr is up 2.1bps at 2.131%, 10-Yr is up 3.6bps at 2.543%, and 30-Yr is up 6.5bps at 3.026%.

- UK: The 2-Yr yield is down 1.7bps at 3.872%, 5-Yr is down 1.7bps at 3.991%, 10-Yr is down 1.9bps at 4.473%, and 30-Yr is down 0.4bps at 5.208%.

- Italian BTP spread down 5.5bps at 91.9bps / Greek bond spread down 3.5bps at 73.9bps

MNI OPTIONS: Euro Rate Call Structure Buying Resumes

Tuesday's Europe rates/bond options flow included:

- DUQ5 107.30/107.20/107.00 broken p ladder, bought for 1.75 in 4k

- ERQ5 98.12/98.1875cs vs 97.9375p bought the cs for 1.5 in 4k

- ERU5 98.125/98.25/98.375c fly, bought for 3.25 in 10k

- ERU5 98.12/98.1875/98.25c ladder, bought for 1 in 4k

- 0RU5 98.375/98.25/98.125p fly vs 97.875p, bought the fly for -0.5 in 8k

MNI FOREX: Greenback Extends Weekly Reversal Lower, USD Index Eyes Cycle Lows

- The dollar remained under renewed pressure Tuesday, as firmer risk sentiment permeated through global markets following the announcement of a truce between Israel and Iran. This allowed the greenback to extend its reversal south that begun late Monday, with the dollar index within close proximity of cycle lows.

- Greenback weakness will likely have been bolstered by cleaner short-term positioning, weaker-than-expected US consumer confidence and Fed Chair Powell not ruling out the chance of an FOMC rate cut as soon as July. In remarks to Congress on Tuesday, Powell said “many paths are possible” when asked about the possibility of a July rate cut, explaining that lower inflation and weaker labour data could portend an earlier cut to interest rates.

- USDJPY (-0.86%) briefly extended the reversal from yesterday’s peak to over 350 pips and the swift move back below its 20-day EMA is a bearish development. With positioning a lot cleaner now following yesterday’s spike higher to 148.03, the risks may be tilted to a more protracted move south, targeting 144.34 (Jun 18 low) initially, before 142.80 Low Jun 13.

- In similar vein, the Swiss Franc continued to perform resiliently, prompting USDCHF (-0.94%) to match the April lows at 0.8040. A break of this bear trigger would confirm a resumption of the medium-term technical downtrend and open the 0.8000 handle, and 0.7927, the 1.50 projection of the May 1 - Sep 6 2024 - Jan 13 price swing.

- AUD and NZD are also performing well, but remain shy of their most recent highs against the greenback, which are located at 0.6552 and 0.6088. Dollar dynamics have allowed the likes of EURUSD and GBPUSD to rise through the overnight highs to their best levels of the cycle, and the next immediate targets for the move are 1.1696 and 1.3681 respectively.

- Australian CPI highlights the Wednesday data calendar, before US new home sales figures. Fed Chair Powell will testify in front of the Senate.

MNI OPTIONS: Expiries for Jun24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E612mln)

- USD/JPY: Y145.00($582mln)

- USD/CAD: C$1.3775($665mln)

MNI US STOCKS: Late Equities Roundup: Eminis & Nasdaq Climb to New 4M Highs

- Despite early morning confusion over Israel/Iran ceasefire pledges, stocks continued to march higher late Tuesday as tensions appeared to de-escalate. Multiple Fed speakers, including Chairman Powell's policy testimony to the House, contributed to support as rate cut chances gained traction.

- SPX emini and Nasdaq index have risen to mid-February levels while if the Dow is near early March highs in late trade. Currently, the DJIA trades up 506.56 points (1.19%) at 43088.53, S&P E-Minis up 70 points (1.15%) at 6146.75, Nasdaq up 295.3 points (1.5%) at 19926.22.

- Information Technology, Financials and Communication Services sectors continued to outperform in the second half: IT leaders included Intel +6.54%, Advanced Micro Devices +6.51%, Enphase Energy +5.06% and Micron +4.47%.

- The Financials sector was supported by services stocks: Coinbase Global +12.05%, Apollo Global Management +4.78% and KKR & Co +4.73%, while media and entertainment shares supported the Communication Services sector: Warner Bros Discovery +2.11%, Charter Communications +2.13%, Netflix +1.97% and Match Group +1.78%

- On the flipside, weaker crude prices (WTI -4.2 at 64.31 - partially due to the de-escalation in the Middle East) weighed on oil and gas stocks: Occidental Petroleum -3.91%, Exxon Mobil -3.15%, ConocoPhillips -2.80%, Chevron -2.41% and Hess -2.29%.

- Broadline retailers weighed on the Consumer Staples sector: Dollar General -1.52%, Estee Lauder -2.80% and Dollar Tree -2.11%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Uptrend Remains Intact

- RES 4: 6249.00 - High Feb 21

- RES 3: 6200.00 1.50 proj of the Apr 7 - 10 - 21 price swing

- RES 2: 6172.50 High Feb 24

- RES 1: 6151.00 Intraday high

- PRICE: 6150.50 @ 1500 ET Jun 24

- SUP 1: 5959.00/5913.50 Low Jun 23 / 50-day EMA

- SUP 2: 5811.50 Low May 23

- SUP 3: 5645.75 Low May 7

- SUP 4: 5500.00 Low Apr 30

The trend condition in S&P E-Minis is unchanged, it remains bullish and this week’s strong start reinforces current conditions. Short-term resistance and a bull trigger at 6128.75, the Jun 11 high, has been pierced. A clear break of this level would confirm a resumption of the uptrend that started Apr 7. This would open the 6200.00 handle, a Fibonacci projection. Key support remains at the 50-day EMA - at 5913.50. A clear break of it would signal a reversal.

MNI COMMODITIES: Crude Falls Sharply, Gold Pulls Back As Geopolitical Tensions Ease

- WTI has recouped some losses during US hours but remains down sharply on the day as the Israel-Iran conflict has de-escalated.

- WTI Aug 25 is down by 5.8% at $64.5/bbl.

- The geopolitical risk premium is unwinding as the risk to Iranian oil infrastructure or disruption to shipping in the Strait of Hormuz has eased.

- Market uncertainty is still high with trade disputes and OPEC output normalisation impacting demand and supply.

- For now, the sell-off is considered corrective and the pullback has allowed a recent overbought condition to unwind.

- Support to watch is at the 50-day EMA, at $64.52, which has been pierced. A clear break of it would signal scope for a deeper retracement towards $58.87, the May 30 low.

- On the upside, initial resistance to watch is $71.39, the 50.0% retracement of the Jun 23 - 24 high-low range.

- Meanwhile, spot gold has fallen by 1.5% to $3,317/oz, taking the yellow metal through the 50-dma support for the first time since mid-May.

- The move came on the back of the tentative ceasefire struck between Iran and Israel and it has seen gold narrow the gap with the June lows of $3,293.64, which form first support.

- Despite this, a bullish theme in gold remains intact and the latest pullback is considered corrective. Resistance at $3,435.6, the May 7 high, has recently been pierced.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 25/06/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 25/06/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 25/06/2025 | 0700/0900 | ** | PPI | |

| 25/06/2025 | 0700/0900 | *** | GDP (f) | |

| 25/06/2025 | 0845/0945 | BOE Lombardelli At BOE MonPol Conference | ||

| 25/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 25/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 25/06/2025 | 0900/1000 | BOE Pill On Panel At BOE MonPol Conference | ||

| 25/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 25/06/2025 | 1230/1330 | BOE Lombardelli Chairs Riksbank's Breman Speech At BOE MonPol Conf | ||

| 25/06/2025 | 1400/1000 | *** | New Home Sales | |

| 25/06/2025 | 1400/1000 | *** | New Home Sales | |

| 25/06/2025 | 1400/1000 | Fed Chair Jay Powell | ||

| 25/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 25/06/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 25/06/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 25/06/2025 | 1800/1400 | Federal Reserve Board Meeting |