MNI ASIA MARKETS ANALYSIS: Iran Warns US Before Retaliation

HIGHLIGHTS

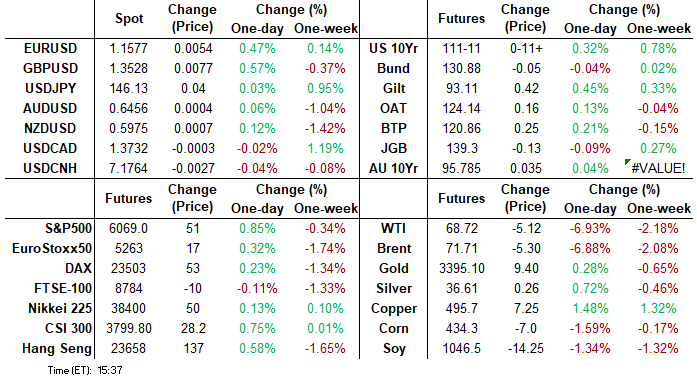

- Treasuries look to finish near midday highs Monday, early support (rates and stocks) amid muted response from Iran to the US bombing 3 nuclear facilities over the weekend.

- Curves bull steepened after Fed VC Bowman said in favor of July rate cut if inflation remains muted, Chicago Fed Goolsbee if tariff passthrough inflation subdued.

- Stocks extended gains even after Iran launched missiles at US base in Qatar, possible face saving measure as Iran warned US prior, most if not all missiles intercepted.

- Crude prices fell sharply (WTI most since April 2020) as Pres Trump urged US to ramp up production.

US TSYS

US TSYS: Tsys Bid With Stocks, Not the Reaction You Were Expecting

- Treasuries looked to finish higher Monday (TYU5 +11.5 at 111-11), curves bull steepening (2s10s +2.645 at 49.176) as rates & stocks rallied on initially muted response by Iran to US bombing over the weekend.

- Stocks extended gains even after Iran launched missiles at US base in Qatar, possible face saving measure as Iran warned US prior, most if not all missiles intercepted.

- Risk gained traction on dovish comments on potential rate cuts from Fed VC Bowman and Chicago Fed Goolsbee if inflation remains muted.

- Projected rate cut pricing gains traction vs. this morning's levels (*), Dec at the highest since May 12: Jul'25 at -5.9bp (-3.6bp), Sep'25 at -25.2bp (-19.5bp), Oct'25 at -32.6bp (-40.7bp), Dec'25 at -58.8bp (-49.9bp).

- Existing home sales unexpectedly ticked up in May to a 4.03M seasonally-adjusted annual pace, from 4.00M in April (and vs 3.95M survey).

- Flash S&P manufacturing PMI held steady at 52.0 for a second month (cons 51.0) after 50.2 in both March and April whilst services dipped to 53.1 (cons 53.0) after 53.7 in May.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.29% (+0.01), volume: $2.700T

- Broad General Collateral Rate (BGCR): 4.27% (+0.00), volume: $1.083T

- Tri-Party General Collateral Rate (TCR): 4.27% (+0.00), volume: $1.060T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $118B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $298B

FED Reverse Repo Operation

RRP usage rebounds to $165.319B this afternoon from $138.283B Friday, total number of counterparties at 34. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

Surge in two-way SOFR puts and upside Aug 10Y Tsy calls reported Monday as underlying futures rallied initially muted response by Iran to US bombing over the weekend and after dovish comments on potential rate cuts from Fed VC Bowman and Chicago Fed Goolsbee if inflation remains muted. Projected rate cut pricing gains traction vs. this morning's levels (*), Dec at the highest since May 12: Jul'25 at -5.9bp (-3.6bp), Sep'25 at -25.2bp (-19.5bp), Oct'25 at -32.6bp (-40.7bp), Dec'25 at -58.8bp (-49.9bp).

SOFR Options:

-10,000 SFRU5 97.50/98.00 call spds, 9.0

Block, 5,000 SFRQ5 96.00/96.12/96.25/96.37 call condors ref 95.955

-10,000 SFRU5 95.75/0QU5 96.25 put spds, 0.0 0QU sold over

-20,000 0QZ5 95.87/96.12/96.25/96.50 put condors, 4.0 vs. 96.865/0.05%

+16,000 SFRU5 95.62/95.75 put spds, 2.5 ref 95.96/0.14%

+7,000 0QN5 96.62/96.75 2x1 put spds 1.5 ref 96.795

-4,000 SFRQ5 95.62/95.75 put spds, 1.125 ref 96.23

-6,000 SFRV5 95.75/95.87/96.00 put flys, 1.75 ref 96.225

-7,000 SFRN5 95.75/95.81/95.87 put flys, 1.0 ref 95.95

-7,000 SFRZ5 put fly strip: 95.56/95.68/95.81, 95.75/95.87/96.00, 96.00/96.12/96.25, collects 4.5

-10,000 SFRH6 94.62/95.62 put spds, 2.25 ref 96.39

-5,000 SFRU5 95.81/96.00 call spds 2.75 over 95.62/95.75 put spds

+6,000 SFRZ5 96.25/96.37/96.50/96.62 call condors, 1.25 ref 96.155

2,250 SFRZ5 96.50/96.75/97.00/97.25 call condors ref 96.155

Block, 2,500 SFRQ5 95.87/96.12/96.37 call trees, 2.5 ref 95.885

1,750 0QQ5 96.87/97.37 call spds

2,000 SFRU5 96.00/96.25/96.50 call flys ref 95.88

2,400 0QQ5 96.37 puts ref 96.69

Block, 2,500 0QZ5 97.00/97.31 call spds, 8.5 vs. 96.765/0.10%

Treasury Options:

Update - over +77,300 TYQ5 112 calls, 28-27 vs 110-29.5/0.26%, appr vol 6.59%

over 62,900 TYQ5 112.5 calls, 28 last

over 76,200 TYQ5 113 calls, 21 last

4,000 TYQ5 110.5/111.5 put spds,

3,300 FVQ5 109/109.75 2x3 call spds ref 108-20.5

4,950 FVQ5 109.75 calls, 11.5

6,000 TYU5 111 puts, ref 111-17.5

+32,000 TYQ5 113 calls, 21 ref 111-15.5/0.20, appr 6.68% vol (exp 7/25)

17,000 TYQ5 109.5/112.5 strangles

1,750 wk4 TY 110.25/111.5 call spds, ref 110-29.5, exp 6/27

+20,000 TYQ5 112.5 calls, 20 vs. 110-29.5/0.19%, appr 6.71% vol

-2,000 TYQ5 111 calls, 48 vs. 110-28/0.47%

MNI BONDS: EGBs-GILTS CASH CLOSE: Yields Pull Back From Early Session Highs

Gilts outperformed EGBs amid an intraday rally Monday.

- Yields jumped in the re-open from the weekend, following the US's bombing of Iranian nuclear sites.

- Global core FI rallied in late morning/early afternoon trade though, with oil prices fading, and dovish comments by a Federal Reserve official (Bowman).

- Eurozone flash June services PMI was in line with expectations, with Germany notably beating consensus; manufacturing was slightly below expected with France notably missing.

- UK manufacturing / services PMI respectively beat/met expectations.

- The German curve leaned bull steeper, with the UK's bull flatter. EGB periphery/semi-core spreads closed slightly tighter.

- Tuesday's data slate includes German IFO and UK CBI trends, while we hear from the majority of the BOE MPC (including Bailey and Pill), as well as multiple ECB speakers.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.2bps at 1.838%, 5-Yr is down 0.8bps at 2.11%, 10-Yr is down 1bps at 2.507%, and 30-Yr is down 1.1bps at 2.961%.

- UK: The 2-Yr yield is down 3bps at 3.889%, 5-Yr is down 3.5bps at 4.008%, 10-Yr is down 4.5bps at 4.492%, and 30-Yr is down 5.8bps at 5.212%.

- Italian BTP spread down 0.7bps at 97.4bps / Spanish down 0.8bps at 69.1bps

MNI EGB OPTIONS: Rates Trade Opens Week On Mixed Note

Monday's rates/bond options flow included:

- DUU5 107.40/107.70cs, bought for 7 and 7.5 in 7.5k

- RXQ5 129.50p, bought for 36.5 and 37 in 3.5k

- ERZ5 98.12/98.25/98.37c fly, bought for 2.75 in 6k

- ERZ5 97.1875p, bought for 0.25 in 4k

- 0RV598.1875/98.3125/98.375c fly, bought for 3 in 5k

- SFIZ5 96.50/96.75/96.85broken c fly, bought for 3.25 in 3k

MNI FOREX: US Dollar Extending Intra-Day Reversal Lower

- The intra-day reversal lower for the greenback is extending, as the USD index now trades through last Friday’s lows, roughly 1% below the earlier session highs. Lower oil prices and resilient equity benchmarks are assisting the renewed USD weakness, despite the plethora of headlines crossing surrounding Iran’s launch of missile attacks towards a US air base in Qatar.

- The likes of GBPUSD (+0.50%) and EURUSD (+0.36%) are leading the charge within the G10 complex. For EURUSD, the bullish trend remains firmly in place and scope remains seen for a climb towards 1.1696, a Fibonacci projection. Recovering global sentiment has tilted the likes of AUD and NZD back to unchanged on the day after being the standout laggards earlier on Monday.

- Euro resilience has also been notable against the crosses with the likes of EURAUD and EURNZD holding onto 0.5% gains on the session.

- JPY volatility has not disappointed, although the Japanese currency has followed the broader dollar trend rather than being impacted by safe haven flows. Initially, USDJPY rose as high as 148.03, which may have been exacerbated by positioning dynamics. However, since then, the pair tracks around 180 pips lower, and is edging towards the overnight lows at the 146.00 handle. Below here, support to watch lies at 145.08, the 50-day EMA.

- The main beneficiary on Monday has been the Swiss Franc, as USDCHF falls 0.67% and edges back towards 0.8100, while CHFJPY has appreciated 0.76%. Earlier in the session spot printed up to 180.88, record highs for the cross.

- Focus on the data calendar tomorrow will be on German IFO, Canada CPI and US consumer confidence. Fed Chair Powell will also deliver his congressional testimony.

MNI OPTIONS: Expiries for Jun23 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E612mln)

- USD/JPY: Y145.00($582mln

- USD/CAD: C$1.3775($665mln)

MNI US STOCKS: SPX Eminis Marking Session Highs

- Despite Iran's retaliatory missile launches at US military base in Qatar, the targeted nature of the attack, which was telegraphed beforehand and "does not pose a threat to Qatar" Iranian officials said.

- This apparently lending to the latest support in stocks. Currently, the DJIA trades up 257.52 points (0.61%) at 42463.49, S&P E-Minis up 42.25 points (0.7%) at 6060.25, Nasdaq up 150.7 points (0.8%) at 19597.04.

- Consumer Discretionary and Utility sectors continue to lead gainers while Health Care and Financial sector shares continue to lag.

MNI EQUITY TECHS: E-MINI S&P: (U5) Shallow Correction

- RES 4: 6200.00 1.500 proj of the Apr 7 - 10 - 21 price swing

- RES 3: 6172.50 High Feb 24

- RES 2: 6134.00 High Feb 26

- RES 1: 6128.75 High Jun 11 and the bull trigger

- PRICE: 6017.75 @ 14:35 BST Jun 23

- SUP 1: 5906.79 50-day EMA

- SUP 2: 5811.50 Low May 23

- SUP 3: 5645.75 Low May 7

- SUP 4: 5500.00 Low Apr 30

The trend condition in S&P E-Minis is unchanged, it remains bullish. For now, the most recent shallow pullback is considered corrective. The contract has pierced support at 6007.80, the 20-day EMA. A clear breach of this average would suggest potential for a deeper retracement and expose the 50-day EMA, at 5906.79. Key short-term resistance and the bull trigger has been defined at 6128.75, the Jun 11 high.

MNI AMERICAS OIL: WTI crude plummeted after Iran responded to US strikes

WTI crude plummeted after Iran responded to US strikes over the weekend with rockets launched toward a US airbase in Qatar, which Qatar said had been intercepted. Thus far, there has been no disruption to oil flows despite some supertankers turning around near the Strait of Hormuz. Concerns are that a further escalation in the conflict could significantly impact oil infrastructure and exports from the region though there have been none as yet.

- WTI Aug futures were down 7.0% at $68.51

- WTI Sep futures were down 6.4% at $67.30

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 24/06/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 24/06/2025 | 0800/0900 | BOE Bailey At Gold Standard Conference | ||

| 24/06/2025 | 0845/1045 | 2025 Budget Press Conference | ||

| 24/06/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 24/06/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 24/06/2025 | 0930/1030 | BOE Green On CB Balance Sheet Mgmt | ||

| 24/06/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 24/06/2025 | 1115/1315 | ECB de Guindos At XLII APIE seminar | ||

| 24/06/2025 | 1230/0830 | *** | CPI | |

| 24/06/2025 | 1230/0830 | * | Current Account Balance | |

| 24/06/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 24/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 24/06/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/06/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 24/06/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 24/06/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 24/06/2025 | 1300/1500 | ECB Lagarde Accepts De Sanctis Award "Europa" | ||

| 24/06/2025 | 1315/0915 | Cleveland Fed's Beth Hammack | ||

| 24/06/2025 | 1335/1435 | BOE Ramsden At Barclays-CEPR MonPol Forum | ||

| 24/06/2025 | 1355/1555 | ECB Lane Keynote At Barclays-CEPR MonPol Forum | ||

| 24/06/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 24/06/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 24/06/2025 | 1400/1000 | Fed Chair Jay Powell | ||

| 24/06/2025 | 1400/1500 | BOE Bailey At Lords Econ Affairs Committee | ||

| 24/06/2025 | 1540/1640 | BOE Pill At Gold Standard Conference | ||

| 24/06/2025 | 1550/1650 | BOE Breeden At UK Finance Digital Innovation Summit | ||

| 24/06/2025 | 1630/1230 | New York Fed's John Williams | ||

| 24/06/2025 | 1700/1300 | * | US Treasury Auction Result for 2 Year Note | |

| 24/06/2025 | 1805/1405 | Boston Fed's Susan Collins | ||

| 24/06/2025 | 2000/1600 | Fed Governor Michael Barr | ||

| 25/06/2025 | 2301/0001 | * | Brightmine pay deals for whole economy | |

| 24/06/2025 | 0015/2015 | Kansas City Fed's Jeff Schmid | ||

| 25/06/2025 | 0130/1130 | *** | CPI Inflation Monthly |