MNI ASIA MARKETS ANALYSIS: House Vote on Reopen Wednesday

HIGHLIGHTS

- Cash closed for Veterans Day holiday - business as usual for futures and equities: Health Care sector shares helping DJIA outperform.

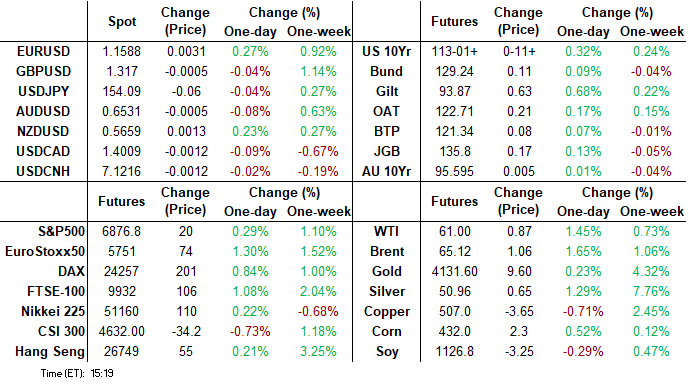

- Treasuries extended highs, 10s neared initial technical resistance after ADP's new weekly employment release showed a decline of -11,250 jobs.

- The Senate passed a stopgap bill last night to fund the US Govt through January 30. Vote goes to the House tomorrow - as early as 1600ET.

US TSYS

MNI US TSYS: Veterans Day Sideways Shuffle

- Treasuries hold firmer - narrow range since marking session high late morning. Currently, the Dec'25 10Y contract trades +10.5 at 113-00.5 vs. 113-01.5 high - just below resistance at 113-02, the Nov 5 and 7 high. Clearance of this level would highlight a potential bullish reversal.

- Otherwise, a short-term bear theme in Treasuries remains in place. Attention is on a reversal trigger at 112-06, the Sep 25 low, and the 100-DMA, at 112-08. A clear break of these price points would expose a trendline support at 112-02. The trendline is drawn from the May 22 low.

- USD also holding narrow range since marking session low in the first half, Bbg $ index BBDXY -1.38 at 1,217.33 vs. 1,216.52 low.

- The DJIA, however, continues to climb: +5011.60 at 47,880.23 (+1.09%), outpacing SPX eminis (+0.28%) while the Nasdaq holds mildly weaker (-0.1%).

- Look ahead: Wednesday data limited to MBA Mortgage Applications at 0700ET, Tsy auctions: $69B 17w bill and 42B 10Y Note (91282CPJ4). Focus on multiple Fed speakers through the session: Williams, Paulson, Waller, Bostic, Miran and Collins.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options shifted to low delta call buying - particularly in Jan'26 10Y calls after a slow start to the session. Underlying futures extended highs after the ADP showed a decline in jobs - futures holding narrow range since late morning, while projected rate cut hold firmer vs late Monday levels (*): Dec'25 at -16.8bp (-15.5bp), Jan'26 at -27.1bp (-25.1bp), Mar'26 at -38.3bp (-35.2bp), Apr'26 at -44.9bp (-41.3bp).

SOFR Options: (Note Nov options expire Friday)

Update, over +25,000 SFRF6 96.62/96.75/97.00 2x3x1 call flys, 2.25-2.75 vs. 96.435/0.09%

+10,000 SFRZ5 96.31 calls, 3.5 ref 96.245

+4,000 SFRF6 96.43/96.62/96.75 call flys, 3.5

+10,000 0QZ5 97.00/97.25 call spds, 5.25 ref 96.905

-5,250 0QZ5 96.93/97.06 call spds, 4.0

-3,000 SFRX5 96.50 calls, 1.5 ref 96.25

+4,000 SFRZ5 96.43/96.50, 0.5 vs. 96.28/0.05%

Block, +5,000 0QH6 96.25/96.50 put spds, 3.5 ref 96.895

1,300 SFRX5 96.18/96.25 box

Block, -10,000 SFRZ5 96.50/96.62 call spds, 0.25

Block/screen, 4,000 SFRG6 96.68/96.81/96.87/97.00 call condors, 0.75

4,000 SFRZ5 96.37/96.56 call spds vs. SFRF6 96.56/96.75 call spds, 2.5 net/Jan bought over

+4,000 SFRZ6 96.12/96.50/96.75 broken put flys, 2.5

-2,000 SFRX5 96.18/96.31 strangles, 0.5

9,350 SFRX 96.18 puts, .25-0.50 total volume over 17,500

over 8,300 SFRX5 96.25 puts

-6,500 SFRZ5 96.43/96.68 call spds, 0.25-0.50

Treasury Options:

2,000 USZ5 120/122 call spds 4

6,100 TYZ5 117.5/120 1x2 call spds ref 113-00

Update over +117,000 TYF6 114 calls, 29 vs. 112-30.5 to -31.5/0.30% (open interest 51,680)

1,000 TUZ5 104.5/104.62 1x2 call spds

2,000 FVZ5 109.75/110/110.5/110.75 call flys ref 109-14

1,250 TYZ5/TYF6 115 call calendar spds

2,000 TYZ5 111.5/112 put spds, 1

-3,500 TYZ5 112.75 calls, 24 vs. 112-23.5/0.47%

+2,500 Wednesday weekly TY 112.5 puts, 1 vs. 112-26/0.28%

+2,500 Wednesday weekly TY 112.75 calls, 21 vs. 112-24/0.45%

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Easily Outperform On Soft Labour Data

Gilts easily outperformed peers Tuesday.

- UK labour market data broadly came in on the soft side, driving an early bull steepening rally. A December BOE cut is now around 80% priced from <70% prior, helping the UK short-end strengthen (2Y yields hit a post-Aug 2024 low).

- Treasuries led a global rally in early afternoon on weekly ADP private sector payrolls data that showed a notable contraction in the 4-week period to Oct 25.

- In other data, German ZEW underperformed in both expectations and current conditions.

- BOE MPC hawk Greene reiterated her previously aired areas of focus, having no impact on the short end & gilts.

- On the day, the German curve lightly bull flattened, while the UK's held its early bull steepening.

- Periphery/semi-core EGB spreads were little changed vs Bunds.

- Wednesday's calendar includes Italian industrial production and final German CPI. We also get commentary from ECB's Schnabel and de Guindos, as well as BOE's Pill.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.4bps at 2.001%, 5-Yr is down 0.9bps at 2.259%, 10-Yr is down 1bps at 2.658%, and 30-Yr is down 0.6bps at 3.254%.

- UK: The 2-Yr yield is down 8.3bps at 3.724%, 5-Yr is down 7.8bps at 3.857%, 10-Yr is down 7.4bps at 4.387%, and 30-Yr is down 6.7bps at 5.172%.

- Italian BTP spread up 0.1bps at 74.5bps / French OAT down 0.4bps at 76.4bps

MNI EGB OPTIONS: Slew Of Sonia Upside Continues After Labour Data

Tuesday's Europe rates/bond options flow included:

- SFIX5 96.20/96.25/96.30/96.35c condor, sold at 4.25 in 3.5k

- SFIG6 96.60/96.70/96.75/96.85 thin body call condor paper paid 1.5 on 9K

- SFIH6 96.60/96.75/96.90 call fly x 2 vs. 96.30/96.00 put spread paper paid 0.75 on 7.5K

- SFIM6 96.85/97.00/97.15c fly x2 vs 96.30/96.00ps, bought the fly for -0.25 in 7.5k x 3.75k

- SFIM6 96.80/96.90cs, bought for 2.25 in 3.5k

- SFIM6 96.80/96.90/97.00/97.10c condor, bought for 1.25 in 5k

- SFIZ6 96.75/97.00/97.25 call fly paper paid 3.75 on 5.25K

- SFIZ6 96.90/97.30/97.45 broken Call fly vs 96.45/96.30ps, bought the fly for 3.25 in 2k

- 0NU6 96.70/96.80 call spread and 97.10/97.20 call spread paper paid 6.25 on 7.5K

MNI FOREX: USD Index Extends Recent Weakness Following Data, CHF Outperforms

- A softer-than-expected ADP jobs release from the US caught the market a little off guard on Tuesday, weighing on the greenback and allowing the USD index to plumb new pullback lows below 99.40.

- ADP noted that “not only is the pace of employment growth shifting lower, it’s doing so in a jagged path across occupations, industries, and geographies. Going forward, instead of being a stable constant, the break-even rate more likely will be constantly moving”.

- Most notable initially was the move for USDJPY, which extended its selloff from the overnight highs to around 80 pips. Downside momentum picked up on a break of the overnight lows, below 154.00 to 153.67 lows before stabilising. We have pointed out that USDJPY continues encounter some resistance above the 154.00 handle, potentially registering an eighth daily high between 154.14-154.49, bolstering the short-term significance of this resistance cluster. First important support to watch lies at 152.70, the 20-day EMA.

- CHF outperforms following late yesterday's optimism on a potential Swiss trade deal with the US. While such a deal would be unlikely to sway SNB rates this year or the next, it should see a moderate upwards revision of 2026 GDP forecasts for the country, which is providing a boost to the Franc. EURCHF sees downside pressure as a function of that at 0.9273, while USDCHF (-0.67%) has tracked back below 0.8000.

- EURUSD broke above Friday’s high to trade back above 1.1600. The 50-day EMA intersects at 1.1627, and a breach would alter the short-term bearish theme.

- It’s worth noting that GBPUSD fully reversed the UK labour market data inspired selloff, however, sterling weakness remains evident through the cross, with EURGBP maintaining its position back above 0.88 for now.

MNI OPTIONS: Expiries for Nov12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500-05(E1.1bln), $1.1550(E790mln), $1.1585-90(E565mln), $1.1645-50(E855mln), $1.1688-90(E1.3bln)

- USD/JPY: Y154.00($500mln)

- GBP/USD: $1.3100(Gbp1.9bln), $1.3150(Gbp674mln), $1.3225-30(Gbp1.3bln)

- AUD/USD: $0.6500(A$1.4bln), $0.6530-50(A$1.4bln)

- NZD/USD: $0.5600(N$538mln)

MNI US STOCKS: Late Equities Roundup: DJIA Outperforming, Health Care Bounce

- Stocks remain mixed late Tuesday, the DJIA outperforming the tech-heavy Nasdaq as AI valuation concerns hampered chip makers again. Muted activity on the Veterans Day holiday, sentiment stable ahead of Wednesday's House vote to re-open/fund the government through Jan 30.

- Currently, the DJIA trades up 509.56 points (1.08%) at 47876.72, S&P E-Minis up 16.25 points (0.24%) at 6873.5, Nasdaq down 39.4 points (-0.2%) at 23488.65.

- Reversing Monday's support - technology stocks continued to lead declines in late trade: Hewlett Packard Enterprise -3.85%, Lam Research -3.72%, Teradyne -3.59%, Micron Technology -3.13%, Cadence Design Systems -2.89%, Applied Materials -2.51%, Synopsys -2.39% and NVIDIA -2.33%.

- Consumer Discretionary and Utilities sector shares followed: Vistra Corp -3.86%Constellation Energy -2.82% and NRG Energy -2.29%; Tapestry -2.47%, Tesla -1.94% and Chipotle Mexican Grill -1.79%.

- On the positive side, a mix of Energy and Health Care sector shares led advances in the second half: Paramount Skydance +9.31%, Viatris +6.54%, Moderna +4.81%, Dexcom +4.76%, Devon Energy +4.22%, Bio-Techne Corp +3.96% and Merck & Co +3.87%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Bullish Recovery

- RES 4: 7000.00 Psychological round number

- RES 3: 6993.12 3.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6974.04 3.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 1: 6877.25/6953.75 Intraday high / High Oct 30 and bull trigger

- PRICE: 6875.00 @ 1433 ET Nov 11

- SUP 1: 6655.70 Low Nov 7 and key short-term support

- SUP 2: 6571.25 Low Oct 17

- SUP 3: 6540.25 Low Oct 10 and a key support

- SUP 4: 6476.62 23.6% retracement of the Apr 7 - Oct 30 bull cycle

The trend condition in S&P E-Minis remains bullish and the bear leg since the Oct 30 high appears corrective. The contract has managed to find support below the 50-day EMA, currently at 6716.03 and a key support. Last Friday’s activity also highlights a potential reversal signal - a bullish doji candle. This defines key support at 6655.50, the Oct 7 low. A continuation higher would signal the end of a correction and open 6953.75, Oct 30 high and bull trigger.

MNI COMMODITIES: WTI Rallies, Spot Gold Steady As Correction Appears Over

- Crude prices are higher today, amid strength in oil product markets, with WTI on track for its highest close since Nov 3.

- WTI Dec 25 is up by 1.5% at $61.0/bbl.

- In the US, the House will return tomorrow to vote on the continuing resolution that could reopen the government by Friday. The bill to provide US government funding until Jan 30 passed the Senate with the support of a number of Democrats.

- For WTI futures, an upward corrective cycle remains intact for now. Price has traded through the 50-day EMA, at $60.85, signalling scope for a stronger recovery.

- Initial resistance is at $62.59, the Oct 24 high. A clear move through it would expose key resistance at $65.77, the Sep 26 high. The bear trigger is $55.96, the Oct 20 low.

- Despite the broader pressure on the USD, meanwhile, following the release of weak US ADP jobs data, spot gold has unwound earlier gains to be broadly unchanged on the day at $4,119/oz.

- There may be some short-term positioning dynamics in play here, given the 3.5% rally from last Thursday’s lows.

- From a technical perspective, the downleg for gold since Oct 20 appears to have been a correction, which has allowed an overbought condition to unwind.

- Recent gains suggest that correction is now over, with price above a key support at the 50-day EMA at $3,898.9. Initial resistance is seen at $4,161.4, the Oct 22 high, a clearance of which would refocus attention on $4,381.5, the Oct 20 high and bull trigger.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 12/11/2025 | 0700/0800 | *** | Germany CPI (f) | |

| 12/11/2025 | 0700/0800 | *** | Germany CPI (f) | |

| 12/11/2025 | 0900/1000 | * | Industrial Production | |

| 12/11/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 12/11/2025 | 1045/1145 | ECB Schnabel Speech at BNP Paribas | ||

| 12/11/2025 | 1140/1240 | ECB de Guindos at FIBI International Banking Conference | ||

| 12/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 12/11/2025 | 1205/1205 | BOE Pill in Panel at International Monetary Research Conference | ||

| 12/11/2025 | - | *** | Money Supply | |

| 12/11/2025 | - | *** | New Loans | |

| 12/11/2025 | - | *** | Social Financing | |

| 12/11/2025 | - | ECB Lagarde, Cipollone at Eurogroup Meeting in Brussels | ||

| 12/11/2025 | - | BOE MPG Meeting | ||

| 12/11/2025 | 1330/0830 | * | Building Permits | |

| 12/11/2025 | 1420/0920 | New York Fed's John Williams | ||

| 12/11/2025 | 1500/1000 | Philly Fed's Anna Paulson | ||

| 12/11/2025 | 1505/1005 | Kansas City Fed's Jeff Schmid | ||

| 12/11/2025 | 1520/1020 | Fed Governor Chris Waller | ||

| 12/11/2025 | 1730/1230 | Fed Governor Stephen Miran | ||

| 12/11/2025 | 1800/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 12/11/2025 | 1830/1330 | Bank of Canada meeting minutes | ||

| 12/11/2025 | 2050/1550 | New York Fed's Roberto Perli | ||

| 12/11/2025 | 2100/1600 | Boston Fed's Susan Collins | ||

| 13/11/2025 | 0030/1130 | *** | Labor Force Survey |