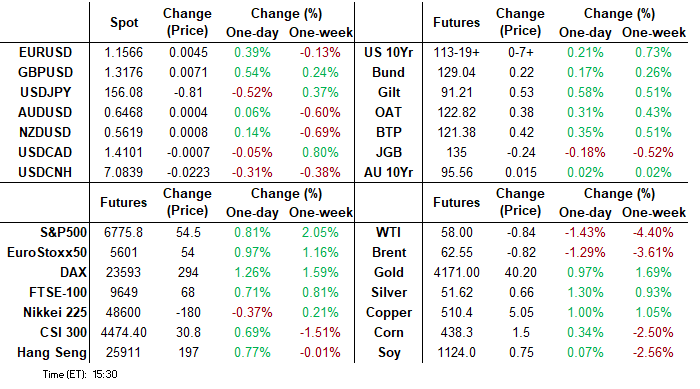

- Stocks are drifting near late session highs Tuesday, the DJIA outperforming moderate gains in SPX eminis and Nasdaq in late trade. Currently, the DJIA trades up 540.49 points (1.16%) at 46988.89, S&P E-Minis up 34.5 points (0.51%) at 6755.75, Nasdaq up 15.2 points (0.1%) at 22886.64.

- Initial risk-on support occurred after early ABC headlines reported that Ukraine has agreed with the United States on the terms of a potential peace deal. Stocks continued to gain after Fed Gov Miran reiterated that current monetary policy is holding the economy back, calling for large rate cuts in a Fox Business interview.

- A mix of Health Care, Consumer Discretionary and Communication Services sector shares led advances in the second half: Revvity +5.28%, Zoetis +4.71%, Align Technology +4.49%, Centene Corp+4.06%, Merck & Co +3.93% and GE HealthCare Technologies +3.69%.

- Chipotle Mexican Grill +6.41%, Lennar Corp +5.51%, DR Horton +5.39%, PulteGroup +5.18% and MGM Resorts Int +5.16%.

- Media and entertainment shares buoyed the Communication Services sector: Meta Platforms +3.07%, TKO Group Holdings +2.07%, Paramount Skydance +1.86%, Live Nation Entertainment +1.77% and Match Group +1.64%.

- On the flipside, Information Technology sector shares retreated after gaining the last few sessions: Advanced Micro Devices -7.39%, NVIDIA -4.41%, Super Micro Computer -3.27%, Oracle Corp -3.26% and Synopsys -1.02%.

- Energy stocks retreated with a decline in crude prices (WTI -0.84 at 58.00): EQT Corp -1.60%, APA Corp -1.56%, Coterra Energy -1.22%, EOG Resources -1.15% and Exxon Mobil -1.05%.

MNI ASIA MARKETS ANALYSIS: Hassett Frontrunner For Fed Chair

Nov-25 20:33By: Bill Sokolis

APAC+ 4

HIGHLIGHTS

- Initial risk-on support occurred after ABC headlines reported that Ukraine has agreed with the United States on the terms of a potential peace deal.

- Treasuries extending highs yet again as Fed Gov Miran sticks to dovish script on Fox Business - that current policy is holding economy back, calling for large rate cuts.

- Midday headlines positing Kevin Hassett being frontrunner in Trump's Fed Chairman search underpinned second half sentiment.

US TSYS

MNI US TSYS: Tsys Gaining on Dovish Fed Speak, Tepid UK/Russia Peace Deal Support

- Treasuries see-sawed higher Tuesday, near early session highs after a moderately volatile first half. TYZ5 +7.5 at 113-19.5 after the bell vs. 113-24 high; 10Y yld slipped below 4% to 3.9865% low briefly - lowest since late October.

- Treasuries extended highs, stocks rallied but quickly reversed after ABC headlines that Ukraine has agreed with the United States on the terms of a potential peace deal with Russia. The peace plan, which will be presented to Russia when Ukraine signs off, has been heavily modified from the 28-point peace plan that was leaked over the weekend. The alterations to the initial proposal, which leaned heavily towards Russian priorities, has led to scepticism that Russia will agree to the basic terms.

- Treasuries extending highs yet again as Fed Gov Miran sticks to dovish script on Fox Business - that current policy is holding economy back, calling for large rate cuts. Headlines reiterating that Kevin Hassett is deemed a frontrunner in search for the next Fed Chair role have prompted a dovish shift in the front-end of the curve, further weighing on the greenback.

- Heavy data day: The delayed retail sales report for September was softer than expected, with control group sales slipping -0.1% M/M for their first (nominal) decline since April;

- Core PPI inflation was softer than expected back in September even if it was partly offset by a revision even further back in July. It broadly chimes with underlying core goods CPI inflation, with a peak for post-tariff M/M inflation pressures having come earlier in the summer (June for our median estimate on the CPI side, July for core PPI). PPI final demand inflation was in line with expectations in September at 0.31% M/M after -0.14% M/M, although core inflation surprised softer.

- The Conference Board consumer survey for November saw a sharper decline in consumer confidence whilst expectations remained below a recessionary threshold for a tenth consecutive month. Consumer confidence was notably weaker than expected in November at 88.7 (cons 93.3) after a slightly upward revised 95.5 (initial 94.6) in October, hitting its lowest since April and before that early 2021.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.96% (+0.03), volume: $3.232T

- Broad General Collateral Rate (BGCR): 3.93% (+0.03), volume: $1.288T

- Tri-Party General Collateral Rate (TCR): 3.93% (+0.03), volume: $1.260T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.88% (+0.00), volume: $73B

- Daily Overnight Bank Funding Rate: 3.88% (+0.00), volume: $159B

FED Reverse Repo Operation

RRP usage at $2.314B with 8 counterparties this afternoon from $1.077B Monday. Compares to last Tuesday's $0.905B - lowest level since mid-March 2021; this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options rotated around upside calls Tuesday (note Sep'26 call spread with par calls) and put unwinds. Underlying futures firmer on dovish Fed speak from Gov Miran, while odds of Kevin Hassett being next Fed Chair gained. Projected rate cut pricing steady at recent highs for Dec (app 80.4% priced in) gaining slightly out the curve: current levels vs. early morning (*): Dec'25 steady at -20.1bp, Jan'26 at -28.4bp (-27.4bp), Mar'26 at -36.8bp (-35.5bp), Apr'26 at -44.9bp (-44.4bp).

SOFR Options:

-13,000 SFRZ5 96.18/96.25/96.37 2x3x1 call flys, 6.0 vs. 96.265/0.10%

-20,000 SFRZ5 96.18/96.25/96.31 iron flys, 4.5 ref 96.2625

+4,000 SFRF6 96.31/96.37/96.43/96.50 put condors 1.0 over 96.56/96.62 call spds

Block, 5,000 SFRZ5 96.18 calls, 1.75

-5,000 SFRZ5 96.25/96.56 call spds, 4.0

+5,000 SFRG6 96.37 calls vs. 0QG6 97.12 call spds, 2.25 Feb over

+5,000 SFRM6 96.12/96.25/96.31/96.43 put condors, 2.5

6,250 SFRZ5 96.12/96.18/96.25/96.31 call condors ref 96.26 to -.2625

over 9,300 SFRZ5 96.25 calls ref 96.255

2,000 0QZ5 97.50/97.68/97.87 2x1x1 call trees ref 96.965

2,000 2QZ5 96.93/97.06 call spds ref 96.92

5,000 SFRZ5 96.31/96.37 call spds ref 96.25

4,000 SFRZ5 96.37 calls, cab

3,700 SFRZ5 96.12/96.25 put spds ref 96.2475

3,000 SFRH6 96.18/96.31/96.43 put flys ref 96.445

3,500 SFRU6 99.00/100.0 call spds ref 96.875

1,000 SFRZ5 96.00/96.06/96.12/96.18 put condors ref 96.2425

Treasury Options:

8,100 FVF6 110 calls 25 ref 109-31

5,625 FVF6/FVH6 110 call spds, 22.5 net ref 109-30

10,000 USH6 115 puts, 102 ref 117-25

-4,500 TYF6 112.5/114.5 strangles, 31

3,250 TYF6 114.5/115 4x3 call spds ref 113-13.5

3,500 TYF6 113.5/114/114.5 call trees

4,250 111/112 2x1 put spds ref 113-16

1,500 TYH6 112/115.5 call spds ref 113-13

5,000 TYF6 113 straddles, 122 ref 113-12.5

1,500 TYF6 116/117.5 call spds ref 113-12.5

over 3,100 TYF6 113.5 calls, 39 ref 113-10.5

2,500 FVF6 109 puts, 8 ref 109-24.25

MNI FOREX: Hassett Headlines Bolster Softer USD Backdrop, UK Budget Awaited

- Tuesday’s FX session was characterised by waning optimism for the dollar, prompting the USD index to recede further from last week’s cycle highs, now tracking comfortably back below the 100.00 mark. Headlines reiterating that Kevin Hassett is deemed a frontrunner in search for the next Fed Chair role have prompted a dovish shift in the front-end of the curve, further weighing on the greenback.

- Additionally, tepid optimism relating to the Russia/Ukraine peace deal have helped boost major equity indices, while also providing notable support to the Euro. As such, EURUSD has risen to 1.1580, narrowing the gap to a key short-term resistance at 1.1656, the Nov 13 high and reversal trigger.

- It is GBP that has stood out as the best performing currency in G10. We noted earlier that potential positioning dynamics could help exacerbate a potential GBP squeeze, and this may have been playing out ahead of tomorrow’s UK budget.

- GBPUSD is currently up 0.72% on the session, rallying as high as 1.3201. Today’s move has notably breached a short-term resistance for cable, rising above the 20-day EMA, at 1.3161, signalling scope for a stronger corrective cycle. More meaningful resistance is at the 50-day, intersecting at 1.3265.

- Lower core yields have allowed USDJPY to further erode a portion of the significant recent upswing, with the pair dipping back below 156.00 today. While the USDJPY bullish trend appears well established, the pair had entered overbought territory, and this short-term pullback is considered technically corrective at this juncture. Support to watch is the prior breakout level around 155.00, which closely coincides with 154.76, the 20-day EMA.

- The RBNZ decision highlights the APAC calendar on Wednesday before all focus turns to the UK budget. It is worth noting that there did appear to be some dollar demand heading into 4pm London, and as a reminder, Barclays’ rebalancing model points to strong Dollar buying against all the majors at month-end in November.

MNI FX OPTIONS: Expiries for Nov26 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1480-00(E2.4bln), $1.1525(E1.0bln), $1.1565(E685mln), $1.1595-00(E1.7bln), $1.1650(E721mln)

- USD/JPY: Y153.00($1.2bln), Y154.00($2.1bln), Y155.00($1.9bln), Y156.00($977mln), Y157.00($941mln)

- AUD/USD: $0.6450(A$1.1bln), $0.6535(A$1.7bln)

- NZD/USD: $0.5670-75(N$1.2bln)

- USD/CAD: C$1.3990-00($1.1bln), C$1.4085-00($1.5bln), C$1.4170($525mln)

- USD/CNY: Cny7.00($1.3bln)

MNI US STOCKS: Late Equities Roundup: Health Care, Discretionary Communications Lead

MNI EQUITY TECHS: E-MINI S&P: (Z5) Short-Term Corrective Cycle Intact

- RES 4: 6953.75 High Oct 30 and bull trigger

- RES 3: 6900.50 High Nov 12

- RES 2: 6791.25 High Nov 20

- RES 1: 6774.50

- PRICE: 6760.50 @ 1445 ET Nov 25

- SUP 1: 6525.00 Low Nov 21

- SUP 2: 6500.00 Round number support

- SUP 3: 6476.62 23.6% retracement of the Apr 7 - Oct 30 uptrend

- SUP 4: 6427.00 Low Sep 2

Weakness last week in S&P E-Minis continues to highlight a bearish threat. The breach of 6655.70, the Nov 7 low cancels recent bullish signals and highlights scope for an extension of the corrective cycle. Sights are on 6540.25 (pierced), the Oct 10 low and a key support. A clear break of it would open 6476.62, a Fibonacci retracement point. Initial firm resistance to watch is 6734.26, the 20-day EMA. A clear break of it would alter the picture.

MNI COMMODITIES: Crude Falls Amid Russia-Ukraine Peace Hopes, Gold Steady

- Crude markets fell under significant pressure after reports that Ukraine had agreed to most terms of a peace plan put together by the US after discussions this weekend. Zelenskiy and Trump are set to hammer out final ‘sensitive’ points. Russia is yet to comment on the latest developments but scepticism that Moscow would agree to the changes remains.

- WTI Jan 26 is down by 1.8% at $57.8/bbl.

- Markets are watching for signs of a successful peace deal for any potential sanctions relief on Russian energy that may follow.

- OPEC+ are meeting on Nov 30 to discuss output policy for next year, having indicated a halt to production hikes in Q1 at the last meeting.

- The move down in WTI futures strengthens a bearish theme, with scope seen for a move towards key support and the bear trigger at $55.99, the Oct 20 low.

- Meanwhile, spot gold is little changed today, with price ticking down by 0.1% to $4,132/oz.

- For gold, the recovery since Oct 28 suggest that the earlier correction is over. The first short-term bull trigger has been defined at $4,245.23, the Nov 13 high. On the downside, key support is at the 50-day EMA, at $3,966.65.

- Elsewhere, copper has rebounded by 0.9% to $510/lb, amid news that Chile’s Codelco is pushing for a massive hike in its annual premium for refined metal supplies to China. Next resistance is at $550.00, the Jul 9 and 28 low.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 26/11/2025 | 0700/1500 | ** | MNI China Money Market Index (MMI) | |

| 26/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 26/11/2025 | 1200/0700 | ** | Brazil Preliminary CPI | |

| 26/11/2025 | 1230/1230 | Chancellor Reeves to deliver UK Budget | ||

| 26/11/2025 | 1330/0830 | ** | Advance Trade, Advance Business Inventories | |

| 26/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 26/11/2025 | 1330/0830 | ** | Durable Goods New Orders | |

| 26/11/2025 | 1330/0830 | ** | Durable Goods New Orders | |

| 26/11/2025 | 1442/0942 | *** | MNI Chicago PMI | |

| 26/11/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 26/11/2025 | 1530/1530 | DMO to publish consultation agenda | ||

| 26/11/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 26/11/2025 | 1605/1705 | ECB Lane Fireside Chat on Macro Outlook | ||

| 26/11/2025 | 1630/1130 | ** | US Treasury Auction Result for 7 Year Note | |

| 26/11/2025 | 1700/1200 | ** | Natural Gas Stocks | |

| 26/11/2025 | 1700/1800 | ECB Lagarde Acceptance Speech | ||

| 26/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 26/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 26/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 26/11/2025 | 1900/1400 | Fed Beige Book | ||

| 27/11/2025 | 0030/1130 | * | Private New Capex and Expected Expenditure |