MNI ASIA MARKETS ANALYSIS: Hasset for Fed Chair Resistance

HIGHLIGHTS

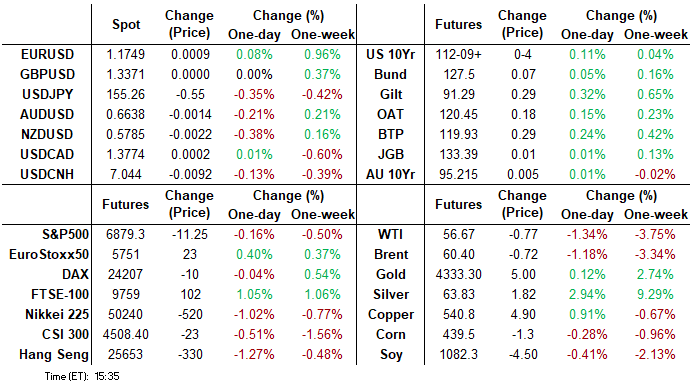

- Treasuries look to finish modestly higher Monday, near midday lows as rates drifted near early overnight support, the 2s10s curve however, steepened to 67.661 (+1.682) highest level since mid-Jan 2022.

- Generally quiet session as participants turn focus on Tuesday's heavy data schedule that includes headline NFP for November, weekly ADP, Retail Sales and S&P Global flash PMIs; absence of Fed speakers tomorrow.

- Fed Gov Miran follows up his third consecutive dissent in favor of a 50bp cut (vs the 25bp decided) at the December meeting with a speech detailing his views on inflation.

- There was a swift turnaround for risk sentiment following the US cash equity open, with weakness for the major US indices and crypto markets fuelling a brief bout of volatility.

US TSYS

MNI US TSYS: Focus on Tuesday's Headline Jobs Data for November, Fed Speakers Absent

- Treasuries look to finish mildly higher Monday, well off midmorning highs to near early evening levels on a Generally quiet session as participants turn focus on Tuesday's heavy data schedule that includes headline NFP for November, weekly ADP, Retail Sales and S&P Global flash PMIs; absence of Fed speakers tomorrow.

- TYH6 trades +4 at 112-09.5 (112-06 low / 112-16.5 high) on just over 1M contracts. Of note, the 2s10s curve however, steepened to 67.661 (+1.682) highest level since mid-Jan 2022.

- Technical resistance at 112-21 (20-day EMA) - a continuation lower would refocus attention on key short-term support at 111-29, the Dec 10 low. Clearance of this level would confirm a resumption of the bear leg and signal scope for an extension towards 111-19, a Fibonacci projection.

- From CNBC sources earlier on the Fed Chair race: "Kevin Hassett's candidacy for the Federal Reserve chair, once seen by the market as almost a sure thing, has received some pushback by high-level people who have the ear of President Donald Trump, according to sources familiar with the matter."

- Fed Gov Miran follows up his third consecutive dissent in favor of a 50bp cut (vs the 25bp decided) at the December meeting with a speech detailing his views on inflation (link). There are no surprises from the current-biggest dove on the FOMC on his rate outlook: he advocates "a quicker pace of easing policy".

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.67% (+0.01), volume: $3.261T

- Broad General Collateral Rate (BGCR): 3.65% (+0.03), volume: $1.324T

- Tri-Party General Collateral Rate (TCR): 3.65% (+0.03), volume: $1.303T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $102B

- Daily Overnight Bank Funding Rate: 3.64% (+0.00), volume: $174B

FED Reverse Repo Operation:

RRP usage rebounds to $2.601B, counterparties steady at 6 this afternoon, vs. Thursday's $0.838B (lowest level since mid-March 2021). Compares to prior low on November 18 low: $0.905B; this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option flow remained mixed, better put volume in SOFR options, Treasury options saw some large low-delta call buying in TYH6. Focus on tomorrow's heavy data docket: weekly ADP and headline employment data for November. Projected rate cut pricing mildly lower for Jan26, gaining slightly through Jun'26 vs. early morning levels (*): Jan'26 at -5.5bp (-6.6bp), Mar'26 at -13.8bp (-13.5bp), Apr'26 at -20.5bp (-20.1bp), Jun'26 at -34.2bp (-33.5bp).

SOFR Options:

Block/screen, +40,000 SFRJ6 96.25 puts, 0.75

+5,000 SFRF6 96.37/96.50 strangles, 6.0 ref 96.47

-2,500 SFRF6 96.50 straddles 10.0 over 96.62 calls ref 96.47

2,300 SFRF6 96.37/96.43 2x1 put spds vs. 96.475

-10,000 SFRF6 96.50 calls, 4.75

+5,00 SFRH6 97.00 calls, 1.75

5,500 SFRH6 96.37/96.50/96.68/96.81 call condors

2,000 SFRF6/SFRG6 96.37/96.43/96.50 put tree spd

2,500 SFRG6/SFRH6 96.31 put spds

12,000 SFRH6 96.37/96.50 call spds ref 96.475 vs.

6,000 SFRH6 96.62/96.68/96.75/96.81 call condors

+11,100 SFRH6 96.31/96.37/96.43/96.50 put condors, 1.5 ref 96.47

+3,500 SFRF5 96.31 puts, 0.5

+5,000 0QF6 97.12/97.37 call spds, 2.0 ref 96.845

Treasury Options

-10,000 TYG6 111 puts, 15 ref 112-09

9,500 TYG6 111/112 put spds, 20 ref 112-08.5

4,000 TYH6 111/113.5 strangles, 59 ref 112-10.5

2,400 TYH6 112 puts ref 112-14.5

7,500 wk3 FV/FVF6 109 put spd

+50,000 TYH6 113.5 calls, 32 vs. 112-11.5/0.31% -- add

-8,000 TYH6 113 calls, 45 vs. 112-14.5

+77,000 TYH6 113.5 calls, 31 ref 112-13

2,000 USG6 108/112 put spds ref 115-03

10,000 TYF6/TYG6 112 put spds, 16 ref 112-10.5

+2,000 TYF6 112.75/113.5 call spds, 11 ref 112-14/0.22%

+6,500 TYF6 112.25/113/114 1x3x1 broken call flys, 1 ref 112-11

1,400 USH6 115 puts ref 115-03

over 2,500 TYG6 114 calls, 11 ref 112-11

+2,000 TYF6/TYG6 115 call spds vs 112-13.5, 5

+14,000 Tuesday wkly 10Y 111.75/112 put spds, 4 (exp tomorrow)

over 5,200 TYF6 112.5 calls, 19

-5,000 TYF6 111.75/113.5 strangles, 16 ref 112-09

3,000 TYF6 111.75 puts ref 112-07

MNI BONDS: EGBs-GILTS CASH CLOSE: Opening Week Flatter With Event/Data Risk Looming

European curves flattened Monday, with the ECB and BOE decisions looming later in a busy week.

- Gilt and Bund futures traded in ranges seen late last week, as part of a broader global move ahead of significant central bank and data events (US and UK labour market and inflation data).

- After a morning rise, core FI had been set to post stronger gains on the day but pulled back sharply in the last couple of hours ahead of the cash close. There wasn't a clear headline/macro catalyst for either move, overall the moves had a positive correlation with risk assets (a late pullback in stocks was associated with weaker bonds).

- In other developments, the French Senate passed the 2026 budget as expected, while the EU unveiled its H1 2026 funding plan, which includes E90B of bonds.

- The UK curve twist flattened with outperformance at the long end vs Germany, whose curve bull flattened. Periphery/semi-core EGB spreads tightened modestly.

- Tuesday's data docket is heavy, with UK labour market data followed by flash December PMIs. MNI's preview of this week's key UK data is here - The labour market and CPI data could pose potential roadblocks but we remain of the view that if data is broadly in line with the BOE's expectation, a cut is likely coming. Elsewhere Tuesday, attention will be on the US employment report for October and November.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.4bps at 2.15%, 5-Yr is up 0.1bps at 2.469%, 10-Yr is down 0.4bps at 2.853%, and 30-Yr is down 0.9bps at 3.472%.

- UK: The 2-Yr yield is up 0.7bps at 3.754%, 5-Yr is down 0.8bps at 3.947%, 10-Yr is down 2.1bps at 4.496%, and 30-Yr is down 2.9bps at 5.239%.

- Italian BTP spread down 1.1bps at 68bps / French OAT down 1.5bps at 70.9bps

MNI OPTIONS: Downside Lean In Bonds, Upside In Rates With BOE / ECB Eyed

Monday's Europe rates/bond options flow included:

- DUF6 106.70 puts seeing paper pay 5 on 4K

- DUG6 106.70/106.80/106.90/107.00 call condor paper paid 3 on 5K

- OEF6 117/116.75/116.50/116p condor, trades for -10 in 3.19k

- RXF6 127/126.50ps, bought for 8 in 1k

- ERZ6 98.25/98.375 call spread, bought for 1.75 in 10k

- ERZ6 97.93/97.68/97.43 put fly paper paid 4.5 on 3K

- 2RH6 97.75/97.62ps vs 0RH6 97.93/97.81ps, bought the 2yr for 1.5 in 10k

- SFIG6 96.60/96.70 call spread, bought for 1 in 8k

- SFIG6 96.45/96.50/96.55/96.60c condor, bought for 1 in 2k.

- 0NZ6 97.00/50 call spread vs. 96.00/95.50 put spread paper paid -0.25 on 10K for the call spread

MNI FOREX: AUDJPY and NZDJPY Consolidate Declines as Risk Turns Lower

- The dollar index has traded within a contained range to start the week, as markets look ahead to the long-awaited US employment release on Tuesday. Elsewhere, there was a swift turnaround for risk sentiment following the US cash equity open, with weakness for the major US indices and crypto markets fuelling a brief bout of volatility. AUD and NZD came under pressure here, while the JPY remains among the best performers in G10.

- For USDJPY, initial softness was as a result of the monthly Tankan survey / wage report in Japan, which reinforces the expectations for a BOJ hike on Friday. Lows of the day were recorded at 154.84, before spot subsequently bounced to the 155.40 region ahead of the APAC crossover.

- Below here, the December 05 low at 154.35 and the 50-day EMA at 153.95 represent an important support area as we navigate both the US data releases and BOJ meeting this week.

- NZD had a volatile session but remains at the bottom of the G10 leaderboard today. Newly appointed RBNZ Governor Breman indicated that market conditions have tightened “beyond what is implied by our central projection” for the official cash rate, prompting a dovish repricing. NZDUSD is down 0.36% on Monday, while NZDJPY currently sits 0.7% in the red.

- It’s perhaps not unsurprising that markets see AUD, JPY and NZD as most exposed headed into tomorrow's NFP print, with those currencies posting the largest overnight vol premium headed into Tuesday's November print. This put AUD overnight vols clear of 14 points at today's open for a new December high and the third highest level of the quarter to imply a +/- 40 pip swing in the price into the Tuesday NY cut.

- UK labour market data precedes Eurozone flash PMIs on Tuesday, before the focus turns to the return of US labour market data.

MNI FX OPTIONS: Expiries for Dec16 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1750-55(E1.8bln)

- USD/JPY: Y156.00($1.1bln)

- GBP/USD: $1.3500(Gbp3.8bln)

- NZD/USD: $0.5845-50(N$540mln)

- USD/CAD: C$1.3750($885mln)

MNI US STOCKS: Late Equities Roundup: Holding Lower Range Ahead Tuesday Data Drop

- Stocks hold moderately weaker levels late Monday, relatively narrow ranges after reversing early session gains, risk sentiment limited ahead of tomorrow's heavy economic data schedule that includes Non-Farm Payrolls for November.

- Currently, the DJIA trades down 87.82 points (-0.18%) at 48370.53, S&P E-Mini Futures down 13 points (-0.19%) at 6877.5, Nasdaq down 120.3 points (-0.5%) at 23074.74.

- Little change from the first half as a mix of Information Technology, Financial and Materials sector shares led declines in the second half: ServiceNow Inc -11.57% as they near $7B Armis acquisition, CoStar Group -7.21%, Coinbase Global -5.41%, Broadcom -5.25%, Workday -3.91%, Mosaic Co -3.82%, Devon Energy -3.62%, Builders FirstSource -3.62% and Uber Technologies -3.20%.

- On the positive side, Consumer Discretionary, Health Care and Utilities sector shares continued to lead advances:

- Tesla +3.89%, Royal Caribbean Cruises +3.77%, Carnival Corp +3.40%, Expedia Group +3.26%, Marriott International Inc +3.09%, Norwegian Cruise Line +3.09% and Booking Holdings +3.00%.

- Bristol-Myers Squibb +3.75%, Eli Lilly +2.99%, Baxter International +2.95%, Intuitive Surgical +2.51%, Pfizer +2.46% and Moderna +2.14%.

- Constellation Energy +1.75%, Public Service Enterprise Group +1.67%, American Electric Power +1.32%, Southern Co +1.22%, Entergy Corp +1.19% and Ameren Corp +1.15%.

MNI EQUITY TECHS: E-MINI S&P: (H6) Bullish Conditions

- RES 4: 7100.00 Round number support

- RES 3: 7044.82 2.0% Upper Bollinger Band

- RES 2: 7014.00 High Oct 30 and the bull trigger

- RES 1: 6988.00 High Dec 12

- PRICE: 6905.75 @ 07:26 GMT Dec 15

- SUP 1: 6864.00 Low Dec 12

- SUP 2: 6828.90 50-day EMA

- SUP 3: 6733.00 Low Nov 25

- SUP 4: 6583.00 Low Nov 21 and a key support

A bull cycle in S&P E-Minis remains intact and a fresh short-term cycle high last week strengthens the bull theme. Sights are on 7014.00, the Oct 30 high and bull trigger. Clearance of this hurdle would confirm a resumption of the primary uptrend. This would open the 7044.82 area, a Bollinger band resistance. Initial firm support to watch lies at 6828.90, the 50-day EMA. Key support and a reversal trigger is at 6583.00, the Nov 21 low.

COMMODITIES

MNI AMERICAS OIL: Americas End of Day Oil Summary: WTI Sinks

WTI has fallen to its lowest close since Oct. 2021 as the market monitors small signs of progress in Ukraine peace talks and expectations of a growing surplus.

- WTI JAN 26 down 1.1% at 56.8$/bbl

- Reuters reports comments from an unnamed US official following the conclusion of two days of talks with the Ukrainian delegation in Berlin. Says that documents relating to security guarantees for Ukraine "have made a lot of progress," describing them as "Article 5-like guarantees.”

- Venezuelan oil exports have fallen sharply since the US seizure of a tanker last week according to Reuters sources.

- Venezuela’s PDVSA is still struggling to restore key administrative systems following what it described as a cyberattack over the weekend, Bloomberg reported.

- Chevron has lowered the price of Venezuelan crude offered to US refiners following the seizure of a tanker by US forces: Bloomberg.

- The amount of crude oil held around the world on tankers that have been stationary for at least 7 days rose 5.1% w/w to 120.23m bbl as of Dec. 12: Vortexa

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 16/12/2025 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 16/12/2025 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 16/12/2025 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 16/12/2025 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 16/12/2025 | 0815/0915 | ** | S&P Global Services PMI (p) | |

| 16/12/2025 | 0815/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 16/12/2025 | 0830/0930 | ** | S&P Global Services PMI (p) | |

| 16/12/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | S&P Global Services PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | S&P Global Composite PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | Italy Final HICP | |

| 16/12/2025 | 0930/0930 | *** | S&P Global Manufacturing PMI flash | |

| 16/12/2025 | 0930/0930 | *** | S&P Global Services PMI flash | |

| 16/12/2025 | 0930/0930 | *** | S&P Global Composite PMI flash | |

| 16/12/2025 | 1000/1100 | * | Trade Balance | |

| 16/12/2025 | 1000/1100 | *** | ZEW Current Expectations Index | |

| 16/12/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 16/12/2025 | 1000/1100 | Foreign Trade | ||

| 16/12/2025 | 1330/0830 | *** | Employment Report | |

| 16/12/2025 | 1330/0830 | *** | Employment Report | |

| 16/12/2025 | 1330/0830 | *** | Employment Report | |

| 16/12/2025 | 1330/0830 | *** | Employment Report | |

| 16/12/2025 | 1330/0830 | *** | Retail Sales | |

| 16/12/2025 | 1330/0830 | *** | Retail Sales | |

| 16/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 16/12/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 16/12/2025 | 1445/0945 | *** | S&P Global Services Index (flash) | |

| 16/12/2025 | 1500/1000 | * | Business Inventories | |

| 16/12/2025 | 1500/1000 | * | Business Inventories | |

| 16/12/2025 | 1730/1230 | BOC Gov Macklem speech in Montreal | ||

| 17/12/2025 | 2350/0850 | * | Machinery orders | |

| 17/12/2025 | 0001/0001 | * | Brightmine pay deals for whole economy |