MNI ASIA MARKETS ANALYSIS: Goolsbee Leaves a Mark

HIGHLIGHTS

- Treasuries retreat from overnight highs - extending lows after hawkish comments from Chicago Fed Goolsbee in FT interview: "uncomfortable overly frontloading rate cuts" while "inflation is going the wrong way".

- Pre-auction short sets vs. $70B 5Y Tsy note auction and rate locks vs. ongoing heavy corporate issuance (Oracle $18B 7pt) weighed on rates.

- The greenback has been steadily appreciating, resulting in the USD index rising above last week’s post-Fed recovery highs.

- Main focus is on Thursday's heavy data drop: Personal Consumption, GDP, Durables/Cap Goods, and weekly claims.

US TSYS

MNI US TSYS: Chicago Fed Goolsbee Uncomfortable W/ Frontloading Rate Cuts

- Treasuries look to finish near late Wednesday session lows, extending the decline late after hawkish comments from Chicago Fed Goolsbee FT interview headlines aired: "UNCOMFORTABLE OVERLY FRONTLOADING RATE CUTS" while we "STILL HAVE MOSTLY STEADY, SOLID JOBS MARKET...AT THE SAME TIME, INFLATION IS GOING THE WRONG WAY".

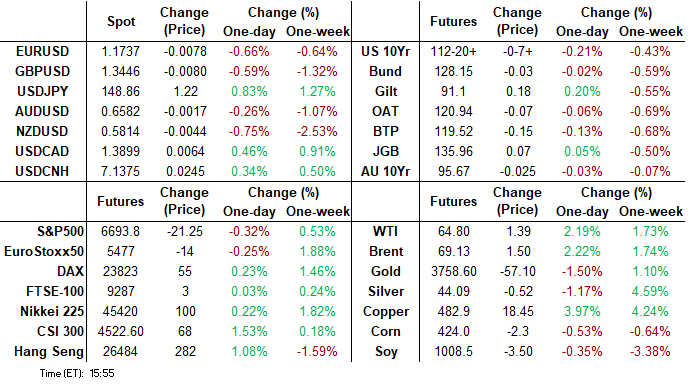

- Currently, the Dec'25 10Y trades -7 at 112-21 (yld 4.1447% +.0385) vs. 112-20 low - nearing technical support at 112-205/112-155 (Low Sep 22 / High Aug 5 and 14). Resistance above at 113-12/29 High Sep 18 / High Sep 11 and the bull trigger. Curves mildly steeper: 2s10s +2.868 at 54.666, 5s30s +.195 at 105.129.

- Tsys were under pressure from pre-auction short sets vs. $70B 5Y Tsy note auction and rate locks vs. ongoing heavy corporate issuance (Oracle $18B 7pt). The latest $70B 5Y note auction (91282CPA3) tailed slightly: 3.710% high yield vs. 3.709% WI; 2.34x bid-to-cover vs. 2.36x prior.

- The greenback has been steadily appreciating, resulting in the USD index rising above last week’s post-Fed recovery highs. The next level for the DXY resides at the 50-day EMA, intersecting today just below the 98.00 mark. Despite a fleeting surge above this average in late July, daily closes above have been rare since February this year.

- Main focus is on Thursday's heavy data drop: Personal Consumption, GDP, Durables/Cap Goods, and weekly claims.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.12% (-0.02), volume: $2.877T

- Broad General Collateral Rate (BGCR): 4.09% (-0.02), volume: $1.160T

- Tri-Party General Collateral Rate (TCR): 4.09% (-0.02), volume: $1.127T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.09% (+0.00), volume: $95B

- Daily Overnight Bank Funding Rate: 4.09% (+0.00), volume: $188B

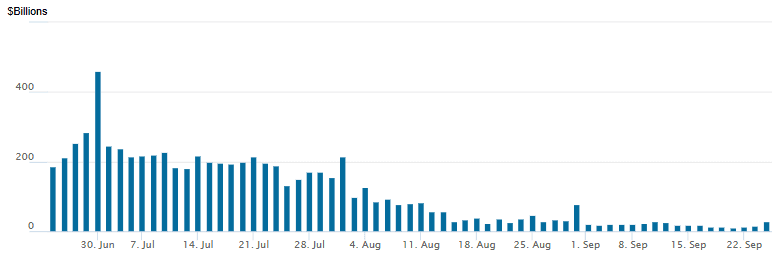

FED Reverse Repo Operation

RRP usage bounces to $29.172B with 22 counterparties this afternoon from $14.402B Tuesday. Compares to $11.363B on Friday, September 16 - lowest level since early April 2021. The year's high usage stands at $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR/Treasury options segued from mixed/calls to better low delta puts trade in the second half as underlying futures extended session lows after Chicago Fed Goolsdbee's hawkish statements in FT interview. Additional caution ahead Thursday's heavy data drop: Personal Consumption, GDP, Durables/Cap Goods, and weekly claims. Projected rate cut pricing drifts off early morning levels (*): Oct'25 at -23.1bp (-23.2bp), Dec'25 at -42.9bp (-44bp), Jan'26 at -54.2bp (-55bp), Mar'26 at -65.6bp (-66.5bp).

SOFR Options:

+6,000 SFRV5 96.50 calls, 0.75 vs. 96.33/0.08%

+10,000 SFRX5 96.87/97.12 call spds, .25 ref 96.32

Block, 5,000 SFRX5 96.37/96.50 call spds, 2.75 ref 96.33

+3,000 SFRZ5 96.37/96.50/96.62 call flys, 2.75

-10,000 SFRZ5 96.68/96.75 call spds, cab

+5,000 0QX5 95.87 puts, cab ref 96.965

+4,000 SFRF6 96.62/96.75 call spds 1.75 over 96.12/96.25 put spds

+5,000 SFRH6 97.25 calls, 3 ref 96.535

2,250 SFRH6 96.12/96.18 put spds vs 96.62/96.75 call spds

8,750 0QZ5 96.68/96.87 2x1 put spds ref 96.975

6,000 0QX5 96.87/97.12 strangles ref 96.98

3,000 SFRZ5 96.62 puts ref 96.975

Treasury Options:

15,000 TYV5 113 puts, 23 ref 112-20.5

+15,000 TYX5 111/112 put spds 1 over 114 calls

9,000 TUX5 104.25/104.38/104.5/104.62 put condors

-14,000 TYX5 112/113.5 strangles, 42 ref 112-22

3,000 USZ5 113 puts, 48 ref 116-15

2,500 TYZ5 111/112 put spds 16 ref 112-24.5

-1,500 TYV5 112.75 puts, 6 ref 112-30/0.35%

1,250 TYV5 112.25/112.5/112.75 put trees, 5 ref 112-24

over 15,000 TYZ5 114 calls, 31 last (another 116k traded Tue, OI +64.9k to 229.3k)

2,500 TYV5 112.5 puts, 3 (total volume over 6.6k)

2,000 TYV5 113/TYX5 111.5 put spds ref 112-28

over 7,200 wk1 TY 112.25 puts, ref 112-28 (exp 10/3)

3,000 TYZ5 113.5/114 call spds ref 112-29

-2,000 TYX5 114/TYZ5 114.5 call spds ref 112-30 (Dec over)

MNI BONDS: EGBs-GILTS CASH CLOSE: Modest Gains Peter Out

European yields closed largely unchanged Wednesday.

- The space saw a light bid in early trade, with cash bonds catching up to US Treasury gains after the European close Tuesday.

- Bunds were helped by German IFO sentiment that came in lower than expected across all of the headline indices (telling a different story to Tuesday's solid Services PMI), as well as ongoing concerns over Russia-Ukraine.

- However, gains petered out. The broader space was weighed down by supply, including short-term BTPs, 7Y Germany, and soft demand in a 5Y UK auction, while US corporate issuance (a $15B sale announced by Oracle) was also seen as a global factor.

- Additionally, OAT spreads widened after French unions called for demonstrations on October 2 after meeting with PM Lecornu, drawing a similar reaction across semi-core/peripheries.

- Gilts slightly outperformed Bunds, with very mild bull flattening in both the UK and German curves. Periphery/semi-core EGB spreads closed modestly wider.

- BOE's Greene speaks after the cash close. Thursday's data includes French consumer confidence, Eurozone money supply and UK CBI sales, while we also get the SNB decision and the ECB's Economic Bulletin.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is unchanged at 2.022%, 5-Yr is down 0.1bps at 2.327%, 10-Yr is down 0.1bps at 2.748%, and 30-Yr is down 0.5bps at 3.338%.

- UK: The 2-Yr yield is down 0.1bps at 3.953%, 5-Yr is down 0.6bps at 4.098%, 10-Yr is down 1.1bps at 4.669%, and 30-Yr is down 1bps at 5.487%.

- Italian BTP spread up 2.3bps at 81.7bps / French OAT up 0.5bps at 82.2bps

MNI OPTIONS: Notable Put Structures Across Euribor And German Bonds

Wednesday's Europe rates/bond options flow included:

- DUV5 107.20/107.10/106.90p ladder, sold at -9.25 (receive) in 7.6k

- RXX5 127/126 put spread sees paper pay 13 on 4K vs. 4K RXV5 128 puts at 7.

- ERH6/0RH6 98.125/98.00ps spread, bought the front for half in 5k

- ERF6 98.125/98.25 call spread, bought for 2 in 6.8k

- ERH6 98.25/98.37 call spread paper paid 1 on 2K

- ERM6 98.25/98.37cs, bought for 2.25 in 10k

- SFIG6 96.20/96.10/96.00p fly, bought for 2 and 2.25 in 25k

- 0RZ5 97.9375/97.75ps 1x2 with 2RZ5 97.75/97.625 ps 1x2, sold the strip at 2.25 in 2.5k.

MNI FOREX: USD Index Extends to Fresh Recovery Highs, NZD Extends Lower

- Across the session, the greenback has been steadily appreciating, resulting in the USD index rising above last week’s post-Fed recovery highs. The next level for the DXY resides at the 50-day EMA, intersecting today just below the 98.00 mark. Despite a fleeting surge above this average in late July, daily closes above have been rare since February this year. A more lasting break could signal scope for a stronger dollar correction to the topside.

- Bar the outperforming Aussie following higher-than-expected CPI data, losses across the G10 have been broad based, with both the Japanese yen and New Zealand dollar underperforming.

- USDJPY (+0.75%) picked up some momentum above 148.38 resistance earlier today, and spot has narrowed the gap to 149.14, the Sep 3 high. Meanwhile, GBPUSD has pierced S-T trendline support, strengthening a bearish threat.

- One chart level that particularly stands out is NZDUSD (-0.80%), as the pair approaches the key 0.5800 pivot support, which coincides with the 50% retracement of the year’s range. Price action has been exacerbated by the break of a short-term trendline and should we break the figure, 0.5728 and 0.5636 would be the most obvious targets for a deeper selloff. Today's dynamic have propelled AUDNZD to another fresh cycle high of 1.1341, extending the cross' impressive rally in recent months.

- USDCHF is up around half a percent as we approach tomorrow’s SNB decision. Analysts expect a hold at 0.00% as most likely, with a cut into negative territory appearing improbable.

- In terms of data, the third read of US GDP will cross, as well as weekly jobless claims. Durable goods and existing home sales data are also scheduled.

MNI US STOCKS: Late Equities Roundup: Paring Longs Ahead Thursday's Heavy Data

- Stocks held at/near Wednesday session lows in late trade, profit taking evident ahead of Thursday's heavy economic data and continued Fed speaker schedule. Currently, the DJIA trades down 163.42 points (-0.35%) at 46128.6, S&P E-Minis down 24.25 points (-0.36%) at 6690.75, Nasdaq down 78.3 points (-0.3%) at 22494.57.

- Materials, Technology and Communication Services sector shares underperformed in the second half. Materials weighed by Freeport-McMoRan -16.08% after down-revising their third-quarter projections, DuPont de Nemours -2.65%, Smurfit WestRock -1.39%.

- Tech stocks drew additional profit taking in the second half: Synopsys -4.71%, Jabil -3.97%, Oracle and Adobe both declined -2.86%, while Electronic Arts -3.30%, Take-Two Interactive Software -2.67% and TKO Group Holdings -2.62% weighed on the Communication Services sector.

- On the positive side, Energy and Consumer Discretionary sector shares continued to lead gainers, oil and gas stocks buoyed the former as crude prices climbed higher (WTI +1.43 at 64.84): EQT Corp +4.18%, Phillips 66 +3.45%, APA Corp +2.86% and Expand Energy Corp +2.79%.

- Discretionary sector shares supported by Tesla +3.66%, Lululemon Athletica +3.13%, eBay +2.59% and Ross Stores +2.43%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Bull Cycle Intact

- RES 4: 6812.29 2.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 3: 6800.00 Round number resistance

- RES 2: 6787.63 1.382 proj of the Aug 1 - 15 - 20 price swing

- RES 1: 6756.75 High Sep 22

- PRICE: 6688.50 @ 1415 ET Sep 24

- SUP 1: 6625.74 20-day EMA

- SUP 2: 6577.25 Low Sep 10

- SUP 3: 6506.07 50-day EMA

- SUP 4: 6417.25 Low Aug 12

A bull cycle in S&P E-Minis remains intact and the contract traded to a fresh cycle high on Monday. Price has recently breached the 6700.00 handle and this signals scope for an extension towards 6787.63, a Fibonacci projection point. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend and positive market sentiment. Initial support to watch lies at 6625.74, the 20-day EMA.

MNI COMMODITIES: Crude Extends Gains, Gold Pulls Back, Copper Jumps

- Crude has seen further support today from an EU plan to tariff imports of Russian oil, additional disruption to Russian energy infrastructure, and a tariff agreement between the US and EU.

- WTI Nov 25 is up by 2.5% at $65.0/bbl.

- Despite this move, the trend condition in WTI futures remains bearish and short-term gains are considered corrective. Initial resistance to watch is $65.43, the Sep 2 high, with key short-term resistance defined at $68.43, the Jul 30 high.

- A stronger resumption of weakness would open $57.50, the May 30 low.

- Meanwhile, gold has pulled back today from yesterday's all-time high, as the steady appreciation of the US dollar to fresh recovery highs has weighed on the yellow metal.

- Spot gold is down by 0.9% at $3,729/oz.

- Gold is still in a clear bull cycle and shallow short-term pullbacks remain corrective. The next objective is the $3,800.0 handle. Initial firm support lies at $3,621.4, the 20-day EMA.

- Elsewhere, copper has rallied by 3.9% today to $482/lb, after Freeport declared force majeure at a key mine in Indonesia.

- Freeport said that suspension of its Grasberg Block Cave mine, the second largest source of the metal, following a deadly mud rush will reduce near-term copper and gold output.

- Today’s rally has seen copper pierce initial resistance at $475.14, the 50-day EMA, a clear break of which would open $550.00, the Jul 9 and Jul 28 lows.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 25/09/2025 | 0600/0800 | ** | PPI | |

| 25/09/2025 | 0600/0800 | * | GFK Consumer Climate | |

| 25/09/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 25/09/2025 | 0730/0930 | *** | SNB Interest Rate Decision | |

| 25/09/2025 | 0800/1000 | ** | M3 | |

| 25/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 25/09/2025 | 1000/1100 | ** | CBI Distributive Trades | |

| 25/09/2025 | 1220/0820 | Chicago Fed's Austan Goolsbee | ||

| 25/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 25/09/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 25/09/2025 | 1230/0830 | * | Payroll employment | |

| 25/09/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 25/09/2025 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 25/09/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 25/09/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 25/09/2025 | 1300/0900 | New York Fed's John Williams | ||

| 25/09/2025 | 1300/0900 | KC Fed's Jeff Schmid | ||

| 25/09/2025 | 1400/1000 | Fed Vice Chair Michelle Bowman | ||

| 25/09/2025 | 1400/1000 | *** | NAR existing home sales | |

| 25/09/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 25/09/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 25/09/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 25/09/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 25/09/2025 | 1700/1300 | Fed Governor Michael Barr | ||

| 25/09/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 25/09/2025 | 1740/1340 | Dallas Fed's Lorie Logan | ||

| 25/09/2025 | 1900/1500 | *** | Mexico Interest Rate | |

| 25/09/2025 | 1930/1530 | San Francisco Fed's Mary Daly | ||

| 26/09/2025 | 2330/0830 | ** | Tokyo CPI |