MNI ASIA MARKETS ANALYSIS: Geopol Risks Simmer Ahead FOMC

HIGHLIGHTS

- Early Monday risk-on / risk-off unwind with Tsys and stocks opening higher on perceived optimism over Iran's interest in nuclear negotiations to stop Israel attacks.

- Said risk-on tone gradually abated by midday as reports of more bombing filtered through markets, Iran stating they are "ready to deal a major blow to Israel".

- Aside from geopol factors, Mon opener was rather quiet with muted data, focus on Wed's FOMC rate announcement, as well as weekly/continuing claims, house starts/build permits & 3 bill auctions ahead Thu's Juneteenth holiday.

US TSYS

MNI US TSYS: Early Risk-On Evaporates, Stocks Just Don't Know it Yet

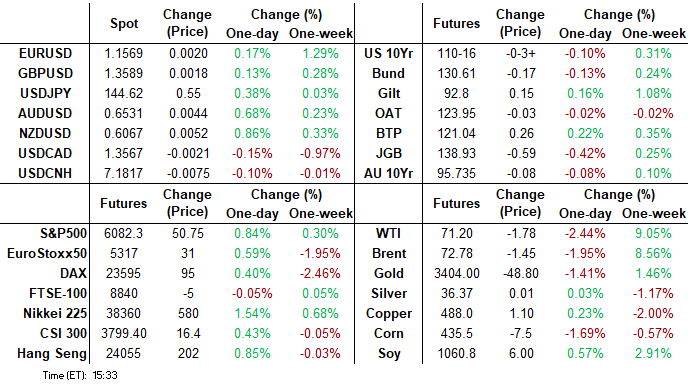

- Treasuries retreated from midday highs as early risk-on tone over easing geopol-tension hopes in turn retreated as Iran and Israel continued to trade missiles. Weaker Treasury futures are back near opening levels with the Sep'25 10Y contract at 110-15.5 (-4) vs. 110-26 overnight high - compares to early Friday high of 111-05 (111-13 overnight high).

- Earlier focus on key resistance and recent high at 111-14+, a Fibonacci retracement and the Jun 5 high. Clearance of this hurdle would be bullish and highlight a stronger reversal. Technical support below at 109-28 (Low Jun 6 / 11).

- Stocks firmer but off early highs, SPX eminis tapped highest levels since last Wednesday: 6055.25 (+76.0) with Financials and IT sectors leading gainers in early trade.

- Despite the breadth of moves, markets rather quiet ahead of Wednesday's FOMC annc. Projected rate cut pricing has cooled vs. morning levels (*) as follows: Jun'25 at 0.0bp, Jul'25 at -3.1bp (-4.1bp), Sep'25 at -17.4bp (-18.4bp), Oct'25 at -30.6bp (-34.9bp), Dec'25 at -46.4bp (-46.9bp).

- Busy Wednesday: addition to FOMC, markets see weekly/continuing claims, house starts/build permits & 3 bill auctions ahead Thursday's Juneteenth holiday. Cash Treasury and stock exchanges are closed Thursday, along with open outcry pits in Chicago but equity and debt futures will be open for an abbreviated trading session.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.28% (+0.00), volume: $2.644T

- Broad General Collateral Rate (BGCR): 4.27% (+0.00), volume: $1.089T

- Tri-Party General Collateral Rate (TCR): 4.27% (+0.00), volume: $1.062T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $110B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $296B

FED Reverse Repo Operation

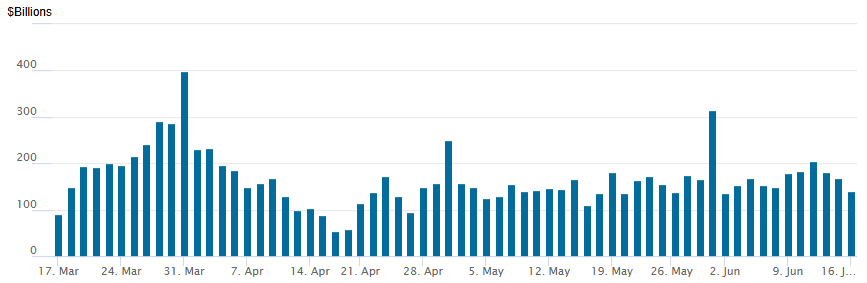

RRP usage retreats to $140.759B this afternoon from $168.645B Friday, total number of counterparties at 26. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

Option desks reported light SOFR & Tsy option flow Monday, mixed flow as underlying futures retreated from early session highs. Underlying futures trade weaker but off late overnight lows, projected rate cut pricing has cooled vs. morning levels (*) as follows: Jun'25 at 0.0bp, Jul'25 at -3.1bp (-4.1bp), Sep'25 at -17.4bp (-18.4bp), Oct'25 at -30.6bp (-34.9bp), Dec'25 at -46.4bp (-46.9bp).

SOFR Options:

Update, total 20,000 0QZ5 96.75/97.00/97.50/97.75 call condors, 6.0 ref 96.72/0.05%

Block, 5,000 SFRV5 95.75/95.93/96.50 broken call trees, 2.5 net ref 96.125

+4,000 0QV5 97.00/97.50/98.00 call flys, 5.5 vs. 96.695/0.10%

+5,000 0QN5 96.75 calls, 8.5 ref 96.62/0.38%

-1,500 2QZ5 96.50 straddles, 61.0-60.5

1,000 SFRU5 95.87/96.06 2x3 call spds, 1.25

3,000 SFRU5 95.37/95.62 put spds, 0.5 ref 95.88 to -.875

1,500 SFRN5 95.62/95.75/95.87 put flys, 4.5

Treasury Options:

Block, 10,000 FVN5 108 calls, 10 vs. 107-29.5/0.44%

-7,500 TYN5 110.25/112 1x2 risk reversals (-p) vs. 110-22.5/0.41%

1,200 TYQ5/TYU5 110.5 call spds, 16 ref 110-23

2,000 TYQ5 110/111 strangles, 1-19

2,000 TYN5 110.5/110.75/111/111.25 call condors

1,250 TYN5 109/109.5 put spds vs. 111.75/112.25 call spds ref 110-14.5

+1,000 TYU5 107/108 put spds 9 vs. 110-21/0.08%

MNI BONDS: EGBs-GILTS CASH CLOSE: Bull Steeper On Another Geopolitically Heavy Day

European yields fell across curves Monday in a bull steepening move.

- Yields rose early in the session, with safe havens shrugging off weekend escalation of Middle East tensions, taking more of a cue from associated higher oil prices.

- But the day's highs were hit relatively early and yields descended from there. Iran-Israel headlines dominated in a data-thin session, with bond gains notably on a WSJ report that Iran was seeking to end hostilities.

- Italian final HICP was revised lower. The Eurozone hourly labour cost index moderated in Q1, but less than initially estimated.

- Both the German and UK curves bull steepened, with Gilts outperforming.

- Periphery/semi-core EGB spreads tightened, with BTPs and OATs outperforming.

- Tuesday's calendar includes the ZEW Survey for June and Spanish labour market data, with speaking appearances by ECB's Villeroy and Centeno.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.5bps at 1.841%, 5-Yr is down 1.6bps at 2.12%, 10-Yr is down 0.8bps at 2.527%, and 30-Yr is down 0.1bps at 2.986%.

- UK: The 2-Yr yield is down 3.4bps at 3.906%, 5-Yr is down 2.4bps at 4.04%, 10-Yr is down 1.7bps at 4.533%, and 30-Yr is down 0.6bps at 5.254%.

- Italian BTP spread down 2.1bps at 92.8bps / French OAT down 2bps at 70.2bps

MNI OPTIONS: Monday Sees Buying Call Structures Versus Puts In Rates

Monday's Europe rates/bond options flow included:

- RXN5 127.5p, bought for 1 in 6k

- ERU5 98.12/98.25cs, bought for 4.5 in 10k.

- ERZ5 98.31/98.37cs vs 97.93p, bought the cs for -0.25 (receive) in 2k

- ERH6 98.5625/98.1875ps 1x2, sold at 11.25 down to 10.50 in 21.6k

- ERH6 98.06/98.18/98.50/98.62c condor vs 97.87p, bought the condor for half in 4k

- 0NU5 96.90/97.40cs 1x1.25 vs 96.10p, bought the cs for 0.5625 in 10k

MNI FOREX: AUD and NZD Outperforming Amid Firmer Risk Sentiment

- The US dollar is underperforming on Monday, as more benign price action across the energy and equity markets is conveying a more stable risk backdrop. WTI and Brent crude futures are roughly 7% off the earlier highs, while the e-mini S&P 500 tracks around 1% in the green to start the week.

- As such, the likes of AUD and NZD have been key beneficiaries within G10, largely mirroring the price action for the major equity benchmarks. AUDUSD has been testing an important resistance point at 0.6550, the Nov 25 high, and a close at current levels would be he highest in 7 months, potentially signalling scope for a stronger recovery to the US election related highs at 0.6688.

- The EUR has also recovered, briefly rising to a session high of 1.1615. The rally has moderated as we approach the APAC crossover as spot deals close to 1.1580 at typing. Sights remain on 1.1696 next, a Fibonacci projection, as the technical uptrend remains firmly in place. Relative underperformance for the safe havens has elevated EURJPY to the highest level since July last year. A positive close today for the cross would be 8 consecutive winning sessions, with sights now on a couple of daily highs at the 168.00 mark.

- USDJPY stands a touch higher Monday, but still managed to establish a 110 pip range on the session, keeping attention on the pair high as we approach tomorrow’s BOJ decision and press conference. 145.46 and 142.12 appear the key short-term parameters for the pair.

- Elsewhere on Tuesday, German ZEW figures are scheduled, before US retail sales and import price data are due.

MNI OPTIONS: Expiries for Jun17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1625(E1.3bln)

MNI US STOCKS: Late Equities Roundup: Walking Back Early Risk-On Tone

- Stocks rebounded from last Friday's sell-off, reacting positively early Monday to headlines that Iran is hoping intermediaries will pressure Israel to a ceasefire in return for "flexibility in nuclear negotiations" with the US.

- The early risk appetite abated as the two continued to bombard each other, Iran stating they are "ready to deal a major blow to Israel". Of note, crude prices remained weaker after late last week's spike higher (WTI -1.34 at 71.64).

- Currently, the DJIA trades up 283.05 points (0.67%) at 42480.07 (42707.73 high), S&P E-Minis up 53 points (0.88%) at 6084.5 (6055.25 high), Nasdaq up 264.1 points (1.4%) at 19670.82 (19733.31 high).

- Information Technology and Communication Services sectors continued to outperform in the second half, Advanced Micro Devices +9.20%, Teradyne +5.46%, ON Semiconductor +5.15%, Monolithic Power Systems +5.11% and Super Micro Computer +4.98% buoyed the IT sector.

- Leading gainers in the Communication Services sector included Warner Bros Discovery +5.63%, Take-Two Interactive Software +3.45%, TKO Group Holdings +3.41% and Meta Platforms +2.91%.

- Energy and Utilities sectors underperformed on the back of weaker crude prices: Diamondback Energy -3.03%, APA -2.43%, ONEOK -2.20%, Occidental Petroleum -2.11% and Targa Resources -2.08%. Meanwhile, Consolidated Edison -2.82%, NextEra Energy -2.26%, DTE Energy -2.03% and CMS Energy -1.69%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Support Remains Intact

- RES 4: 6200.00 1.500 proj of the Apr 7 - 10 - 21 price swing

- RES 3: 6172.50 High Feb 24

- RES 2: 6134.00 High Feb 26

- RES 1: 6128.75 High Jun 11

- PRICE: 6090.00 @ 1500 T Jun 16

- SUP 1: 5979.00/5882.88 Low Jun 13 / 50-day EMA

- SUP 2:5811.50 Low May 23

- SUP 3: 5645.75 Low May 7

- SUP 4: 5500.00 Low Apr 30

The trend condition in S&P E-Minis remains bullish and the contract traded to a fresh cycle high last Wednesday, reinforcing current bullish conditions. For now, the most recent pullback is considered corrective. The contract has pierced support at 5990.75, the 20-day EMA. A clear breach of this average would expose the 50-day EMA, at 5882.88. Key short-term resistance has been defined at 6128.75, the Jun 11 high.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 17/06/2025 | 0600/0800 | ** | Unemployment | |

| 17/06/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 17/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 17/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 17/06/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/06/2025 | 1230/0830 | *** | Retail Sales | |

| 17/06/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 17/06/2025 | 1230/0830 | *** | Retail Sales | |

| 17/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 17/06/2025 | 1315/0915 | *** | Industrial Production | |

| 17/06/2025 | 1400/1000 | * | Business Inventories | |

| 17/06/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 17/06/2025 | 1400/1000 | * | Business Inventories | |

| 17/06/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 5 Year Note | |

| 18/06/2025 | 2350/0850 | * | Machinery orders |