MNI ASIA MARKETS ANALYSIS: Focus on Wednesday CPI

HIGHLIGHTS

- Treasuries look to finish moderately higher Monday, recovering a fraction of Friday's pos-jobs data sell off.

- Pres Trump deploys appr 500 US Marines to LA to help stem anti-immigration protest violence.

- Modest week opener volumes (TYU5 under 1M after the bell) on light second tier data and the Fed in Blackout, focus is on Wednesday's CPI inflation data.

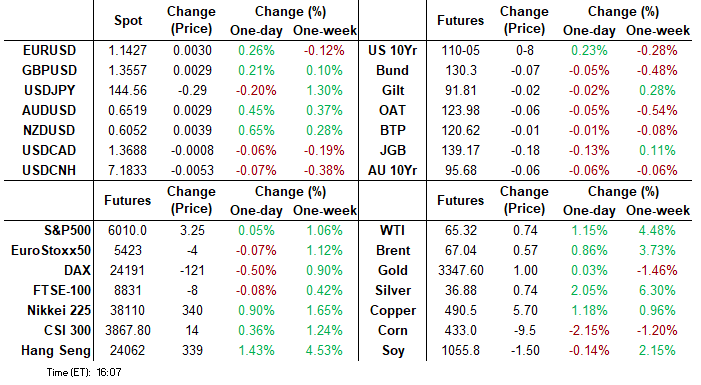

- USD index remains lower on the session, hovering in close proximity to pre-NFP levels, stocks mildly higher (SPX +1 at 6007.75) along with crude (WTI +.74 at 65.32) and Gold (+18.88 at 3329.29).

US TSYS

MNI US TSYS: Late Risk-Off Tone as Marine Battalion Deployed to LA

- Muted reaction after the bell, stocks pared gains after wires reported a battalion of Marines (appr 500) to be deployed to Los Angeles to quell immigration protest unrest.

- Treasuries blipped higher after NY Fed 1Y inflation expectations come out lower than expected. Tsys remain inside session range, curves steeper with Bonds lagging.

- 1-Year median inflation expectations fell to 3.2% from 3.6% prior, the biggest drop since February 2023 to the lowest level since February of this year. 3Y median ticked 0.2pp lower to 3.00% (fully reversing what now appears to be a temporary tariff-led increase in April).

- Tsy Sep'25 10Y futures currently trades 6 at 110-03 vs. 110-07.5 session high, technical resistance above at 110-20.5 (50-day EMA).

- Curves steeper: 2s10s +0.903 at 47.391, 5s30s +1.498 at 86.007

- Cross asset: Stocks mildly higher, paring gains (SPX eminis +2.25 at 6009.0), Gold higher at 3327.5.

- Bbg US$ index little weaker, inside range at 1209.21 (-2.53).

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.29% (+0.00), volume: $2.667T

- Broad General Collateral Rate (BGCR): 4.27% (+0.00), volume: $1.072T

- Tri-Party General Collateral Rate (TCR): 4.27% (+0.00), volume: $1.043T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $118B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $301B

FED Reverse Repo Operation

RRP usage rises to $179.315B this afternoon from $149.284B Friday, total number of counterparties at 37. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options remain mixed in the second half, volumes picking up in the wings. Underlying futures higher/off highs. Projected rate cut pricing retreats slightly vs. morning levels (*) as follows: Jun'25 steady at 0.0bp, Jul'25 at -3.6bp (-4.1bp), Sep'25 at -17.4bp (-17.9bp), Oct'25 at -29.6bp (-30.6bp), Dec'25 at -44.9bp (-45.9bp).

SOFR Options:

Late: 16,000 0QU5 96.75/97.00 call spds vs. 32,000 0QU5 97.25/97.68 call spds

Block, +6,250 0QV5 95.87/96.12/96.37 put trees, 4.5 ref 96.625 -- adds to:

+10,000 0QV5 95.87/96.12/96.37 put trees, 4.0 ref 96.625

+4,000 0QV5 95.75/96.12/96.37 broken put trees, 3.5

+6,000 0QM5 96.50/96.62 call spds, 3.0 vs. 96.46/0.25%

+20,000 SFRN5 97.37 calls, 0.5 ref 95.86

+4,000 SFRZ5 95.56/95.68/95.81 put flys, 2.5 ref 96.105

+10,000 0QU5 95.62/95.87 put spds, 1.5 ref 96.555

+8,000 SFRN5 95.87/96.00/96.12 call flys, 1.25-1.5

+2,500 SFRZ5 96.18/96.50/96.81 call flys, 3.5 vs. 96.12/0.20%

-4,000 SFRH6 95.62 put 0.5 over 96.25/96.62/97.00 call fly

+2,500 0QN5 97.62/98.25 call strip, .75

-7,500 0QZ5 97.25/97.50 call spds 0.5 over 96.37/96.62/96.87 call flys

-10,000 SFRH6 95.68 puts, 6.5 ref 96.29

-10,000 0QQ5 96.87 calls, 4.0 vs. 96.565/0.26%

Block, 4,800 SFRU5 95.75/95.87 put spds 8.0 ref 95.87

9,000 SFRU5 95.81/95.93 call spds ref 95.865

2,500 0QV5 96.00/96.25 put spds ref 96.61

2,000 SFRZ5 96.25/96.50 call spds

5,000 SFRZ5 96.25/96.37/96.50/96.62 call condors ref 96.11

1,000 SFRU5 95.68/95.87/96.00 broken put flys ref 95.865

1,000 0QM5 96.37/96.50/96.75/97.00 broken call condors ref 96.475

+5,000 0QM5 96.43/96.56/96.68 1x3x2 call flys 1.5 vs. 96.425/0.05%

Treasury Options:

+10,000 TYN5 108.5 puts, 3 vs. 110-04.5/0.05%

1,250 TUQ5 103.75/104 2x3 call spds vs. 2,500 TUQ5 103.12 puts ref 103-15.88

3,000 TYN5 109 puts, 8 ref 110-04

4,500 Wed wkly TY 109.25/109.75 put spds ref 110-02.5 (exp 6/11)

+3,000 FVQ5 107.75/108.75 1x2 call spds 4.5 ref 107-21

Block, -10,000 FVN5 107 puts, 6 ref 107-19.5

MNI BONDS: EGBs-GILTS CASH CLOSE: Yields Dip Ahead Of UK Labour Market Data

European yields fell modestly Monday, with bellies outperforming on core curves.

- Bunds and Gilts were solid early, the former continuing a partial recovery from the post-ECB lows.

- The rally lost steam though. There was a modicum of risk appetite on reports suggesting the US and China could reach an agreement on key issues central to their trade dispute (including on export restrictions/rare earths), while higher oil prices weighed in early afternoon trade.

- Core FI would get a bit of a lift from a notable downtick in US consumer inflation expectations (NY Fed), helping cement modest gains.

- The German and UK curves leaned slightly steeper overall, with 5Ys slightly outperforming.

- Periphery/semi-core EGB spreads were little changed, with BTPs slightly outperforming.

- Tuesday's highlight is the UK labour market report - MNI's preview is here. The most important number remains the private AWE ex-bonus, which consensus expects to fall to 5.3% in the 3-months to April from 5.56%Y/Y in the 3-months to March. The UK spending review comes Weds.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.6bps at 1.864%, 5-Yr is down 1.9bps at 2.156%, 10-Yr is down 0.9bps at 2.567%, and 30-Yr is up 0.3bps at 3.012%.

- UK: The 2-Yr yield is down 1bps at 4.003%, 5-Yr is down 1.7bps at 4.138%, 10-Yr is down 1.2bps at 4.632%, and 30-Yr is down 1.1bps at 5.328%.

- Italian BTP spread down 0.6bps at 92bps / French OAT unchanged at 67.2bps

MNI OPTIONS: Sizeable Put Condor Purchases In Euribor Monday

Monday's Europe rates/bond options flow included:

- ERU5 98.18/12/06/00 put condor bought for 0.75 to 1 in 20.5k all day

- ERZ5 98.06/97.93 1x2 put spread bought for 1.75 in 6k

- ERZ5 98.25/98.1875/98.00/97.75 put condor, bought for 1.5 in 5k

MNI FOREX: Greenback Moderately Weaker, Antipodean FX Outperforms

- Although off its worst levels, the USD index remains lower on the session, hovering in close proximity to pre-NFP levels. Overall, this keeps the prevailing theme of a weaker greenback intact, and the DXY within range of the early June pullback low at 98.351 - a key level of support.

- Ahead of U.S.-China talks in London today, President Trump authorized Treasury Secretary Scott Bessent's team to negotiate away recent restrictions on the sale of a wide variety of technology and other products to China, according to people familiar with the matter. This is keeping risk sentiment buoyant to start the week.

- This cautious optimism is prompting AUD and NZD to outperform on Monday. NZDUSD has broken back above an important zone of resistance between 0.6025/40. Spot continues to threaten a daily close above the US election related highs, signalling scope for a more protracted recovery towards 0.6168, the 76.4% retracement of the Sep '24 - Apr '25 selloff. Initial resistance is seen at 0.6080, last week's high print.

- For AUDUSD, last Thursday’s close above 0.6500 was the highest in 6 months, and Monday’s resumption of strength keeps trend signals bullish. The pair’s recent climb signals scope for an initial climb to 0.6550, a Fibonacci retracement and the Nov 25 high.

- Elsewhere, the likes of JPY, EUR and GBP have all risen between 0.2-0.3% to start the week. USDJPY displayed its usual volatility in posting a near 100 pip range and has settled just below 144.50 as we approach the APAC crossover. EURUSD is consolidating back above 1.14 as markets continue to digest the latest ECB decision and await further US data, most notably – the May inflation release on Wednesday.

- Uk labour market data kicks off Tuesday’s calendar, while markets will remain sensitive to global trade developments.

MNI OPTIONS: Expiries for Jun10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1300-20(E1.5bln), $1.1370-75(E920mln), $1.1400-25(E2.1bln)

- USD/JPY: Y143.90-00($1.1bln), Y144.85-00($805mln)

- AUD/USD: $0.6420(A$771mln), $0.6460(A$529mln)

- USD/CAD: C$1.3695($869mln)

MNI US STOCKS: Late Equities Roundup: Extending Modest Gains

- Stocks are holding modest gains late Monday, near session highs with the Dow joining S&Ps and Nasdaq on a relatively quiet start to the week as investors set their sites on this Wednesday's CPI inflation data for direction.

- Currently, the Dow trades up 99.15 points (0.23%) at 42862.01, S&P E-Minis up 18.25 points (0.3%) at 6025, Nasdaq up 92.8 points (0.5%) at 19622.68.

- Materials, energy and tech-related stocks continued to lead gainers in late trade: Enphase Energy +7.48%, Albemarle +4.93%, ON Semiconductor +4.86%, QUALCOMM +4.53%, Microchip Technology +4.52%, Advanced Micro Devices +4.49% and Evergy +4.12%.

- Meanwhile, health care and insurers continued to underperform after Goldman Sachs healthcare conference where industry leaders reported average hospital stays remain longer than pre-Covid levels.

- Laggers included Universal Health Services -6.10%, Intuitive Surgical -5.43%, Aon -4.06%, Allstate -3.79%, HCA Healthcare -3.21%, Arthur J Gallagher -3.19% and Progressive Corp-3.19%.

MNI EQUITY TECHS: E-MINI S&P: (M5) Fresh Cycle High

- RES 4: 6124.00 High Feb 24

- RES 3: 6080.75 High Feb 26

- RES 2: 6057.00 High Mar 3

- RES 1: 6025.00 High June 6

- PRICE: 6015.50 @ 14:24 BST Jun 9

- SUP 1: 5883.97/5789.71 20- and 50-day EMA values

- SUP 2: 5756.50 Low May 23

- SUP 3: 5596.00 Low May 7

- SUP 4: 5455.50 Low Apr 30

The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract traded to a fresh cycle high last week. The recent break of 5993.50, the May 20 high and a bull trigger, highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. A continuation would open 6057.00 next, the Mar 3 high. Key support lies at 5789.71, the 50-day EMA.

MNI COMMODITIES: Crude Rises, Metals Gain As US-China Talks Begin

- Crude prices are higher today, as risk sentiment has remained supported by US-China trade talks in London.

- Ahead of the talks, President Trump authorised Treasury Secretary Bessent's team to negotiate away recent restrictions on the sale of a wide variety of technology and other products to China, according to people familiar with the matter.

- WTI Jul 25 is up by 1.2% at $65.4/bbl.

- WTI futures traded higher last week, resulting in a clear break of resistance around the 50-day EMA. The climb signals scope for an extension towards $65.82, the Apr 4 high, followed by $71.10, the Apr 2 high and key resistance.

- It is still possible that the recovery since early May is a correction, and support to watch lies at $59.74, the May 30 low.

- Meanwhile, spot gold has risen by 0.7% to $3,334/oz, amid a moderately weak US dollar.

- A bullish theme in gold remains intact and a continuation of gains would refocus attention on $3,435.6, the May 7 high.

- Elsewhere, copper has also rebounded by 1.4% to $492/lb, as the red metal remains supported by a drop in inventories and disruptions to supply.

- Copper futures breached resistance at $498.25, the Apr 23 high last week, undermining the recent bearish theme and signalling scope for an extension higher near-term. This has opened $509.85, a Fibonacci retracement.

- On the downside, a pivot support is seen at $474.84, the 50-day EMA

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 10/06/2025 | 0600/0800 | *** | CPI Norway | |

| 10/06/2025 | 0600/0700 | *** | Labour Market Survey | |

| 10/06/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 10/06/2025 | 0800/1000 | * | Industrial Production | |

| 10/06/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 10/06/2025 | - | *** | Money Supply | |

| 10/06/2025 | - | *** | New Loans | |

| 10/06/2025 | - | *** | Social Financing | |

| 10/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 10/06/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 10/06/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result |