MNI ASIA MARKETS ANALYSIS: Focus on Wed FOMC, No Move Expected

HIGHLIGHTS

- Treasuries look to finish mostly lower Monday, off lows on late deal-tied unwinds and positioning ahead of Wednesday's FOMC policy annc.

- Limited volume with with multiple Spring holidays around the globe: Japan, China, HK, South Korea, as well as the UK, EU is open however.

- Focus on Wednesday's FOMC: expected to extend its series of rate holds to a third meeting in May, keeping the Fed funds target rate at 4.25-4.50% while maintaining its forward guidance in the Statement.

US TSYS

MNI US TSYS: Focus Remains on Midweek FOMC, ISM Service 2Y Highs

- Treasuries look to finish lower Monday, off late session lows as rates bounced in reaction to reversal in stocks that had been climbing steadily off early session lows.

- Generally quiet session on lighter volumes (TYM5 <1M) with multiple Spring holidays around the globe: Japan, China, HK, South Korea, as well as the UK, EU is open however.

- Focus on Wednesday's FOMC rate annc at 1400ET. The FOMC is expected to extend its series of rate holds to a third meeting in May, keeping the Fed funds target rate at 4.25-4.50% while maintaining its forward guidance in the Statement.

- Treasury futures gap lower after higher than expected ISM Services data - climbing to the highest levels since January 2023 (51.6 from 50.8 vs 50.2 est; Employment Index 49.0 Vs Mar 46.2; New Orders Index 52.3 Vs Mar 50.4; Prices Index 65.1 Vs Mar 60.9.

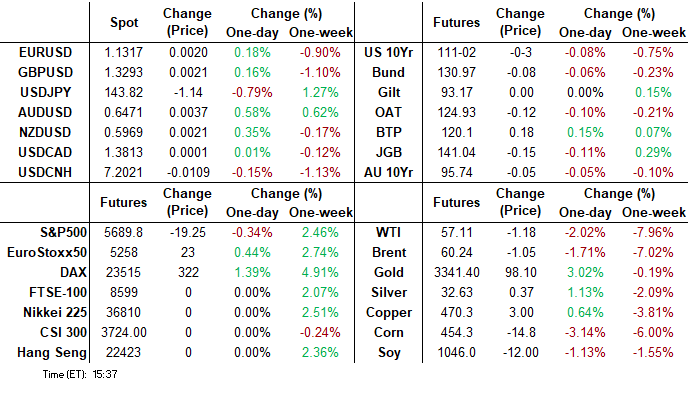

- Jun'25 10Y currently -3 at 111-00 vs. 110-28.5 low (10Y yld at 4.3394%), through technical support at 110-30.5 (50-day EMA). A clear breach of this average would strengthen a bearish threat and expose 110-16+, the Apr 22 low.

- Cross asset: Still weaker BBG US$ index bounces to 1221.48 (-3.03); stocks weaker after paring losses all day: S&P eminis -20.5 at 5688.5.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.36% (-0.03), volume: $2.694T

- Broad General Collateral Rate (BGCR): 4.33% (-0.02), volume: $1.073T

- Tri-Party General Collateral Rate (TCR): 4.33% (-0.02), volume: $1.036T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $111B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $279B

FED Reverse Repo Operation

RRP usage recedes to $124.690B this afternoon from $147.882B Friday. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B. The number of counterparties at 32.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options remained mixed lat eMonday, lighter volumes with multiple spring holiday closures in Asia and UK. Focus on Wednesday's FOMC policy annc, no rate change expected. Underlying futures weaker but off late session lows. Projected rate cut pricing vs. morning levels (*) as follows: May'25 steady at -0.5bp, Jun'25 at -7.3bp (-8.4bp), Jul'25 at -23.3bp (-25.5bp), Sep'25 -42.2bp (-46.9bp).

SOFR Options:

+15,000 SFRM5 95.68/95.75/95.81/95.87 put condors, 2.0 ref 95.78

+8,000 0QM5 98.00 calls, 1.0 vs. 96.805/0.05%

-2,500 SFRK5 95.62/95.68/95.75 2x3x1 put flys w/ SFRM5 95.62/95.75 put spds, 10.5 total

+15,000 SFRU5 98.00 calls

-10,000 SFRU5 96.43/96.62 call spds, 3.25

+4,000 SFRU5 95.75/95.87 2x1 put spds, 0.5 ref 96.14

2,000 SFRH6 97.18/98.25 call spds vs. 0QH6 97.25/98.25 call spds, 2.5 net/0QH6 over

+2,500 SFRH6 97.50/98.00 call spds, 7.5 ref 96.67

+5,000 SFRN5 95.75/95.87 put spds 2.0 vs. 96.195/0.05%

+4,000 0QM5/0QU5 97.00/97.50/98.00 call fly spd, 0.5 net

+4,000 SFRZ5 95.93 puts, 9.5 ref 96.475

2,000 SFRK5 95.93/96.00 call spds ref 95.80

over 3,500 SFRK5 96.06 calls, 0.5 ref 95.81

Treasury Options:

7,500 TYM5 111.5 calls, 36 ref 111-01

Block, 8,500 TYM5 112.5 calls, 14 ref 111-01

+3,000 TYM5 111 straddles, 123 6.89% vol

4,000 TYM5 108 puts, 2 ref 111-01.5

over 12,200 TYM5 113 calls, 10 ref 111-02

-17,000 FVN5 110.5/111.5 call spds 5.5 ref 108-14.75

1,500 TYM5 111.75 straddles,

over 7,000 TYN5 110.5 puts ref 111-08

2,000 TYM5 111/112 2x1 put spds

over 7,500 TYM5 112 calls, 25 last

1,600 FVM5 107/107.5 put spds ref 108-14.25

2,000 TYM5 110.5/111.25 put spds, 22 ref 111-06.5

over 3,200 TYM5 111.25 calls, 46 ref 111-08

1,000 TYM5 111/112/113/114 call condors

1,600 FVM5 107.25 puts ref 108-15.25

MNI FOREX: Tale of Two Halves as Greenback Recovers Following US Data

- Initially on Monday, the US dollar traded weaker against all others in G10, as traders were happy to erode a portion of the post-NFP advance and resume the underlying trend of greenback selling. However, firmer-than-expected ISM services data assisted a solid rebound, with dollar indices now only trading in moderately negative territory as we approach the APAC crossover.

- US ISM Services Index data rose to the highest level since January 2023, and the higher-than-expected prices paid component (65.1 vs. 61.4 est.) has provided further impetus for the greenback recovery.

- This has helped the likes of EUR and GBP to edge back towards unchanged on the session, the clear underperformers in G10. For EURUSD, this translates to the pair reversing around 65 pips from session highs to trade back at 1.13. Initial key support to watch is the 20-day EMA, at 1.1264.

- A similar move for GBPUSD has seen spot narrow the gap to overnight lows of 1.3257. A bearish tweezer top formation on the daily candle chart last Monday/Tuesday highlights a short-term top. Support to watch lies at 1.3225, the 20-day EMA. A break of this level would signal scope for a deeper retracement.

- AUD remains among the best performers after an extended period of consolidation, AUDUSD is gaining following the surprisingly strong showing for Anthony Albanese in the weekend's general elections. The price action puts the rate above the 200-dma and a close above would be the first since November last year.

- Despite the dollar rebound, USDJPY remains 0.6% lower on the session at 144.10, with technical resistance levels remaining intact for now. Moving average studies remain in a bear-mode position highlighting a dominant downtrend. Lower-than-forecast inflation data in Switzerland did little to knock the ongoing optimism for the Swiss Franc. Key USDCHF resistance remain intact at 0.8333, the 2023 low and breakdown point.

MNI FX OPTIONS: Expiries for May06 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1275(E508mln), $1.1325(E717mln), $1.1400(E632mln), $1.1500-10(E2.2bln)

- GBP/USD: $1.2980-90(Gbp545mln)

- USD/JPY: Y142.00($1.1bln), Y144.50-55($638mln), Y146.00($1.9bln)

- EUR/GBP: Gbp0.8500-05(E535mln)

- AUD/USD: $0.6300(A$813mln), $0.6500(A$702mln)

- USD/CAD: C$1.3815-30($874mln)

- USD/CNY: Cny7.3000($1.5bln)

MNI US STOCKS: Late Equities Roundup: DJIA Continues To Outpace SPX & Nasdaq

- Stocks continue to inch higher late Monday, moderate gains in the DJIA outpacing weaker SPX eminis and Nasdaq indexes at the moment. Currently, the DJIA trades up 65.13 points (0.16%) at 41381.93, S&P E-Minis down 11 points (-0.19%) at 5698, Nasdaq down 42.7 points (-0.2%) at 17935.12.

- Industrials and Consumer Services sectors led gainers in the second half, mostly travel related shares supported the former: Delta Air Lines +3.44%, Cummins +2.38%, United Airlines +2.38% and Uber Technologies +2.21%.

- Interactive media and entertainment supported the Consumer Services sector: Charter Communications +3.17%, Take-Two Interactive +2.64%, Electronic Arts +2.56% and Live Nation Entertainment +2.09%.

- Conversely, oil and gas stocks continued to weigh on the Energy sector as crude remains weaker (WTI -1.16 at 57.13): APA -3.92%, Occidental Petroleum -3.52%, ConocoPhillips -2.99%, ONEOK Inc -2.50% and Exxon Mobil -2.38%.

- Consumer Discretionary sector weighed by Starbucks -2.80%, Chipotle Mexican Grill -2.33%, Mohawk Industries -2.03%, Tesla -1.54% and NIKE -1.42%.

- Latest earnings after the close include: Neurocrine Biosciences, Ford Motor, Mattel Inc, Clorox, Diamondback Energy, Coterra Energy, Vertex Pharmaceuticals, Celanese, Williams Cos, Realty Income, Hims & Hers Health and Palantir Technologies .

MNI EQUITY TECHS: E-MINI S&P: (M5) Clears The 50-Day EMA

- RES 4: 5865.42 200-dma

- RES 3: 5837.25 High Mar 25 and a bull trigger

- RES 2: 5773.25 High Apr 2

- RES 1: 5724.75 High May 2

- PRICE: 5664.75 @ 14:22 BST May 5

- SUP 1: 5511.99 20-day EMA

- SUP 2: 5355.25/5127.25 Low Apr 24 / 21 and a key support

- SUP 3: 4996.43 76.4% retracement of the Apr 7 - 10 bounce

- SUP 4: 4832.00 Low Apr 7 and the bear trigger

The latest recovery in the e-mini S&P reinforces current bullish conditions.The contract has traded through the 50-day EMA, at 5620.87. A continuation of the bull phase would expose 5837.25 next, the Mar 25 high and a bull trigger. It is still possible that the entire rally since Apr 7 is a correction. A reversal lower would signal the end of this corrective phase and expose initially, support at 5127.25, the Apr 21 low.

COMMODITIES

WTI Crude Oil (front-month) down $1.14 (-1.96%) at $57.13

Gold is up $84.71 (2.61%) at $3323.19

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 06/05/2025 | 0545/0745 | ** | Unemployment | |

| 06/05/2025 | 0645/0845 | * | Industrial Production | |

| 06/05/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 06/05/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 06/05/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 06/05/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 06/05/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 06/05/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 06/05/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 06/05/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 06/05/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 06/05/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 06/05/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 06/05/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 06/05/2025 | 0900/1100 | ** | PPI | |

| 06/05/2025 | - | FOMC Meeting | ||

| 06/05/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 06/05/2025 | 1230/0830 | ** | Trade Balance | |

| 06/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 06/05/2025 | 1400/1000 | * | Ivey PMI | |

| 06/05/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 07/05/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 07/05/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI |