MNI ASIA MARKETS ANALYSIS: Focus on SCOTUS Tariff Opinion Day

HIGHLIGHTS

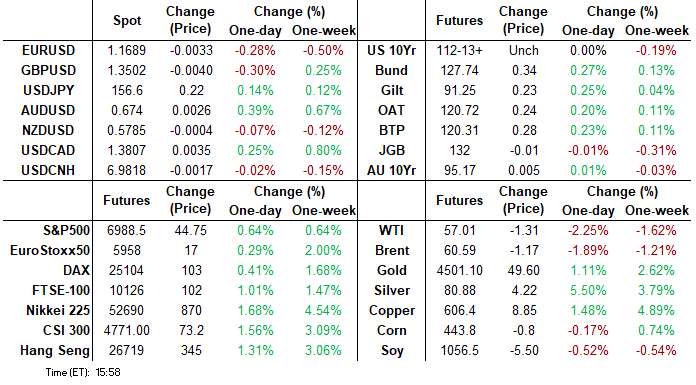

- Treasuries look to finish weaker Tuesday, near the middle of a relatively narrow session range, curves flatter after massive selling in the short end (over 690k FFF6 down to 96.36 -0.0075).

- Richmond Fed Barkin speech takes a measured approach, noting that after some "insurance" cuts, policy is close to neutral, with the dual mandate variables finely balanced.

- The USD index has drifted higher on Tuesday, as markets appear lacking in conviction ahead of the important US ISM services and NFP data releases later in the week.

- Supreme Court announces a ruling on the legality of the White House's IEEPA tariffs on Friday Jan 9 (per the Court's updated calendar here they have set Friday as an "Opinion Day"; the justices sit at 10am).

US TSYS

MNI US TSYS: Treasuries Pare Early Losses, Eye on Employ Data, SCOTUS on Tariffs Fri

- Treasuries are running mildly weaker after the bell, well off morning lows after massive selling in Jan'26 Fed Funds (-450k, total DV01near $19M) in the first half.

- In FX, this has translated to further USD strength, prompting a continued reversal of yesterday's weakness. We noted at the time the low levels of participation in the EURUSD, GBPUSD rallies and that's helping both pairs show back through 1.17 and 1.35 respectively. Others looks far more resilient, with AUDUSD remaining higher on the session.

- Currently, TYH6 trades 112-12 (-1.5) vs. 112-06 low / 112-14 high; Curves currently mixed: 2s10s at 70.386 -.256, 5s30s -.091 at 114.438.

- Treasuries are in consolidation mode and continue to trade above key support at 111-29, the Dec 10 low and bear trigger. The trend remains bearish and a break of 111-29 would confirm a resumption of the bear cycle. This would open 111-19 initially, a Fibonacci projection.

- Services PMI: 52.5 in Dec final (flash and cons 52.9) after 54.1 in Nov; Composite PMI: 52.7 in Dec final (flash 53.0) after 54.2 in Nov; the downward revision for services is in contract to the unrevised final manufacturing reading reported last week.

- It's possible that the Supreme Court announces a ruling on the legality of the White House's IEEPA tariffs on Friday Jan 9 (per the Court's updated calendar here they have set Friday as an "Opinion Day"; the justices sit at 10am), but it's not certain given that they do not announce in advance what opinions that they are providing.

- Looking ahead: ADP private employ & JOLTS data tomorrow, NFP Friday.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.70% (-0.05), volume: $3.441T

- Broad General Collateral Rate (BGCR): 3.66% (-0.04), volume: $1.348T

- Tri-Party General Collateral Rate (TCR): 3.66% (-0.04), volume: $1.313T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $92B

- Daily Overnight Bank Funding Rate: 3.64% (+0.00), volume: $178B

FED Reverse Repo Operation

RRP usage recedes to $2.582B with 10 counterparties this afternoon vs. $6.485B Monday. Compares to December 12 low of $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

Larger SOFR put flow focused on January that expire next week Friday - well before the first FOMC of 2026 on Jan 28. & Treasury options more mixed/two-way with some large low-delta 10Y call buying in Feb. Underlying futures mildly weaker - off lows, curves mixed (2s10s -.079 at 70.563; 5s30s +.185 at 114.532). Projected rate cut pricing cools slightly vs. late Monday levels (*): Jan'26 at -4.6bp, Mar'26 at -13.2bp (-13.9bp), Apr'26 at -18.6bp (-19.5bp), Jun'26 at -31.7bp (-34.3bp).

SOFR Options:

+8,000 SFRZ6 99.00/100.00/101.00 call flys, 1.5

-8,000 SFRZ6 96.50/96.87 3x1 put spds 1.0-0.75

10,000 SFRF6 96.25/96.37 call spds ref 96.465

-10,000 3QH6 96.25/96.50 put spds vs. 0QH6 96.50/96.75 put spds, conditional curve flattener, 4.5 cr

1,800 SRFH6 96.43/96.50/96.56 call spds

3,000 SFRH6 96.37 puts ref 96.475

5,000 SFRH6 96.43/96.56 call spds

+2,000 SFRH6 96.37/96.43 2x1 put spds, 1

over +5,000 SFRF6 96.25/96.31/96.43/96.50 call condors, 3.5

+12,000 SFRF6 96.37/96.43/96.50 put flys, 1.5 ref 96.48

+1,500 SFRF6 96.37/96.43/96.50 1x3x2 call flys, 1.0

+52,000 SFRF6 96.43 puts, 2.25-2.5 - total volume over 101.5k, part tied to put fly & condor

4,500 SFRF6 96.37/96.43/96.50 put flys ref 96.48

+5,000 SFRF6 96.25/96.31/96.37/96.43 put condors ref 96.48

+5,000 SFRF6 96.37/96.43 put spds, 2.25 vs. 96.47/0.20%

5,000 SFRF6 96.31/96.43/96.50 1x3x2 call flys, 4.75

+3,400 SFRG6 96.43/96/56/96.68 call flys, 2.75

1,500 SFRG6 96.43 puts ref 96.48

Treasury Options:

appr +80,000 TYG6 117.25 calls, cab-7

+35,000 TYG6 114 calls, 2

+12,000 FVG6 109 puts, 11.5 vs. 109-05.5

3,500 USG6 114/116 strangles, 54-55

2,450 FVG6/FVH6 110 call spds, 8.5 ref 109-07

+5,000 TYH6 114 calls, 12

-9,000 TYH6 111.5 puts, 22

+4,500 TYG6 111/111.5 put spds, 5 vs. 112-06.5/0.11%

1,500 wk2 TY 111.5/111.75/112 put trees (exp Fri)

2,170 TYH6 111.5 puts ref 112-10.5

+2,000 USG6 112/114 2x1 put spds, 15

-10,000 TYH6 113.5 calls, 17

MNI BONDS: EGBs-GILTS CASH CLOSE: Yields Fall Again As Data Come In On Dovish Side

European yields fell for a second consecutive session Tuesday, with some moderation in Eurozone inflation at end-2025.

- Softer-than-expected German state-level/national inflation helped Bunds rally over the course of the session, with Gilts largely following suit with no major UK-specific macro/headline drivers on the day.

- The short-end/belly led gains on a higher probability of ECB cuts priced by end-2026.

- Other data were also accommodating to European rates. French HICP was broadly in line but CPI was slightly weaker than expected. Final December PMIs were on the weak side too, with the Eurozone composite revised down 0.4 points to 51.5, and the UK's down 0.7 to 51.4.

- Periphery / semi-core EGB spreads were little changed. OAT spreads notably rose vs falls elsewhere, with French Finance Minister Lescure saying the fiscal deficit could come in higher than 5.4% of GDP this year.

- Looking ahead to Wednesday, with 2/3 of country reports in, we estimate some downside risks to the 2.0% Y/Y consensus for the Eurozone HICP reading (we get Dutch and Austrian readings before the EZ print, with Italy coming simultaneously with the Eurozone number).

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.7bps at 2.1%, 5-Yr is down 2.9bps at 2.424%, 10-Yr is down 2.8bps at 2.842%, and 30-Yr is down 2.7bps at 3.48%.

- UK: The 2-Yr yield is down 2.3bps at 3.697%, 5-Yr is down 2.3bps at 3.915%, 10-Yr is down 2.6bps at 4.48%, and 30-Yr is down 1.9bps at 5.227%.

- Italian BTP spread down 0.6bps at 69.3bps / French OAT up 0.5bps at 70.9bps

MNI OPTIONS: Large Put Structure Buying In Euribor, Sonia Feature Tuesday

Tuesday's Europe rates/bond options flow included:

- DUH6 106.80/107/107.20c fly, sold at 3.5 in 7k

- DUH6 106.70/106.90/107.00c fly 1x3x2, bought for 4.5 in 5k (5kx15kx10k)

- RXG6 126.50/126ps, bought for 8 in ~3.5k

- ERH6 98.125c vs 2RH6 97.8125c, trades 1.5 and 1.75 for the 2yr in 16.6k

- ERU6 97.62p sold at 2 in 11k

- ERU6 98.0625/97.9375/97.875p ladder, bought for 3.75 in 15k total

- ERU6 98.0625/98.1875 call spread vs 97.6875/97.5625 put spread, paper pays 1.75 to buy the call spread in 7.5k

- ERZ6 98.12/98.31/98.43/98.62c condor sold at 2 in 4k

- ERZ6 98.25/98.50cs, bought for 2.75 in 8k

- SFIU6 97.00/96.75ps 1x2, bought for half in 20k

- SFIZ6 96.90/97.00cs vs 96.35/96.25ps, bought the cs for 0.75 in 2k

MNI FOREX: EUR Pressured by Soft Inflation, AUD Extends Advance Ahead of CPI

- The USD index has drifted higher on Tuesday, as markets appear lacking in conviction ahead of the important US ISM services and NFP data releases later in the week. Elsewhere, Euro weakness has been evident through the session on the back of softer-than-expected French and German inflation data releases, while higher beta currencies continue to react favourably to the stronger equity/commodity backdrop.

- Following the initial Eurozone inflation releases earlier in the session, EURUSD has been grinding steadily lower from the 1.1743 highs, consolidating back below 1.17 ahead of the APAC crossover. For EURAUD, the cross has extended its break below support at 1.7462, continuing to trade at the lowest level since May, signalling scope for a more protracted selloff towards a key downside target at 1.7248, the May 2025 low.

- AUDUSD made fresh cycle highs at 0.6739 today, strengthening bullish conditions for the pair. Notable topside levels include 0.6795 and 0.6858 are the next chart points of note, projection levels of the Nov 21 - Dec 10 - 18 price swing. Notably, AUDNZD has risen to another cycle high during today’s session, as the cross now operates at the highest level since 2013. Australian CPI data is due on Wednesday.

- In EM, the South African Rand continues to standout, printing fresh cycle highs earlier in the session amid the ongoing constructive price action for metals. The trend condition in USDZAR remains firmly bearish, with sights on 16.2545 next, the 1.764 projection of the Sep 4 - Oct 9 - Nov 5 price swing.

- US ISM services will highlight Wednesday’s calendar, as markets also await Friday’s release of non-farm payrolls.

MNI FX OPTIONS: Expiries for Jan07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1725(E685mln), $1.1775(E1.4bln)

- USD/JPY: Y156.00($677mln), Y157.00($903mln)

- NZD/USD: $0.5650(N$1.1bln)

- USD/CAD: C$1.3800($1.3bln), C$1.3835($852mln)

MNI US STOCKS: Late Equities Roundup: DJIA Extends Record High Yet Again

- Stocks continued to plow higher Tuesday, the DJIA climbing to a new record high (49,504.12) after paring gains earlier when Treasury yields followed USD higher after Bloomberg reported the Supreme Court announced this Friday as their "opinion day" over ruling on Pres Trump's global tariffs.

- Currently, the DJIA trades up 508.28 points (1.04%) at 49484.2, S&P E-Mini Futures up 44.5 points (0.64%) at 6988.25, Nasdaq up 144.7 points (0.6%) at 23540.05.

- Technology and Health Care sector shares continued to lead advances in late trade, AI-related valuation concerns in abeyance as chip makers surged: Sandisk Corp +24.78%, Western Digital +16.64%, Seagate Technology +13.84%, Microchip Technology +11.60%, Micron +8.45%, NXP Semiconductors +8.45%, Texas Instruments +7.95%, Lam Research +6.25% and Analog Devices +5.24%.

- Pharmaceutical makers continued to buoy the Health Care sector: Moderna +9.73%, Incyte +5.14%, Align Technology +4.43%, Stryker +4.40% and Quest Diagnostics +4.23%.

- Energy and Communication Services sectors led declines in the first half, oil and gas shares trimming prior session gains tied to the US abduction of Venezuela's Maduro over the weekend: Kinder Morgan -4.50%, Chevron -4.38%, Williams Cos -4.14%, ONEOK -3.91%, Halliburton -3.41%, Coterra Energy -3.21% and Exxon Mobil -2.94%.

- Meanwhile, Paramount Skydance -3.70%, Comcast -3.23%, AT&T Inc -2.25%, Alphabet -1.12% and T-Mobile US -1.07% weighed on the Communication Services sector.

MNI EQUITY TECHS: E-MINI S&P: (H6) Support Remains Intact

- RES 4: 7080.92 0.764 proj Nov 21 - Dec 11 - 18 price swing

- RES 3: 7021.79 0.618 proj Nov 21 - Dec 11 - 18 price swing

- RES 2: 7014.00 High Oct 30 and the bull trigger

- RES 1: 6994.00 High Dec 26

- PRICE: 6988.50 @ 1556 ET Jan 6

- SUP 1: 6865.03 50-day EMA

- SUP 2: 6771.50 Low Dec 18 and a key support

- SUP 3: 6684.50 Low Nov 24

- SUP 4: 6583.00 Low Nov 21 and a reversal trigger

A recent pullback in S&P E-Minis appears corrective. A key near-term support has been defined at 6771.50, the Dec 18 low. Clearance of this level is required to signal scope for a deeper retracement and would also highlight a possible short-term reversal. For bulls, sights are on key resistance at 7014.00, the Oct 30 high. A break of this hurdle would confirm a resumption of the primary uptrend.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 07/01/2026 | 0700/0800 | ** | Retail Sales | |

| 07/01/2026 | 0745/0845 | ** | Consumer Sentiment | |

| 07/01/2026 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 07/01/2026 | 0855/0955 | ** | Unemployment | |

| 07/01/2026 | 0900/1000 | *** | Bavaria CPI | |

| 07/01/2026 | 0900/1000 | *** | Baden Wuerttemberg CPI | |

| 07/01/2026 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 07/01/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 07/01/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 07/01/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 07/01/2026 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 07/01/2026 | 1000/1100 | *** | EZ HICP Flash (2dp) | |

| 07/01/2026 | 1000/1100 | *** | Italy Flash Inflation | |

| 07/01/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 07/01/2026 | 1315/0815 | *** | ADP Employment Report | |

| 07/01/2026 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 07/01/2026 | 1500/1000 | ** | Factory New Orders | |

| 07/01/2026 | 1500/1000 | ** | Factory New Orders | |

| 07/01/2026 | 1500/1000 | *** | JOLTS jobs opening level | |

| 07/01/2026 | 1500/1000 | *** | JOLTS quits Rate | |

| 07/01/2026 | 1500/1000 | * | Ivey PMI | |

| 07/01/2026 | 1500/1000 | ** | Durable Goods New Orders | |

| 07/01/2026 | 1500/1000 | ** | Durable Goods New Orders | |

| 07/01/2026 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 07/01/2026 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 07/01/2026 | 2110/1610 | Fed Vice Chair Michelle Bowman | ||

| 08/01/2026 | 2330/0830 | ** | average wages (p) | |

| 08/01/2026 | 0030/1130 | ** | Trade Balance |