MNI ASIA MARKETS ANALYSIS: Focus on Fundamentals-Stocks Bounce

HIGHLIGHTS

- Treasuries see-sawed off early session highs, curves twist steeper with bonds leading the decline in the second half.

- Likely Govt shutdown to proceed at midnight tonight, some procedural votes set for Wednesday but those are likely to fail, and the Senate is not in session Thursday, hence the earliest the impasse is likely to be resolved is Friday.

- In the event of a shutdown, the BLS will suspend data distribution: Thu's weekly jobless and Fri's non-farm payrolls.

- Stocks actually stage late session recovery - as focus turns toward fundamentals instead of political turmoil.

US TSYS

US TSYS: Curves Twist Steeper Heading into Likely Gov Shutdown at Midnight

- US Govt likely to shutdown at midnight tonight - the first time since late Dec 2018 when the government shutterd for 35 consecutive days. Senate majority whip Barrasso: "SENATE TO VOTE THIS WEEKEND ON REOPENING GOVERNMENT", Bbg.

- The BLS plans to postpone key economic releases in the event of a shutdown: "BLS will suspend all operations. Economic data that are scheduled to be released during the lapse will not be released. All active data collection activities for BLS surveys will cease. The BLS website will not be updated with new content or restored in the event of a technical failure during a lapse." LINK

- That said, most of Wednesday's scheduled data should be released as most are generated by non-govt firms, Construction Spending the lone exception tomorrow as the U.S. Census Bureau the source. Updates to follow if/when an announcement of a closing is made.

- Treasuries trading mixed after the bell, curves twist steeper (2s10s +2.591 at 54.207) as Bonds led the decline in the second half, Tsy Dec'25 10Y contract (TYZ5) currently trades at 112-15.5 (-1) on decent cumulative volumes of 1.68M. 10Y yield at 4.1483% (+.0096).

- A short-term bear cycle in Treasury futures remains in play. Last Thursday’s sell-off resulted in a print below the 50-day EMA, currently at 112-10+. A clear break of this average would undermine a bull theme and signal scope for a deeper retracement. This would open 111-13+, the Aug 18 low and the next key support. On the upside, initial firm resistance to watch is 113-00, the Sep 24 high.

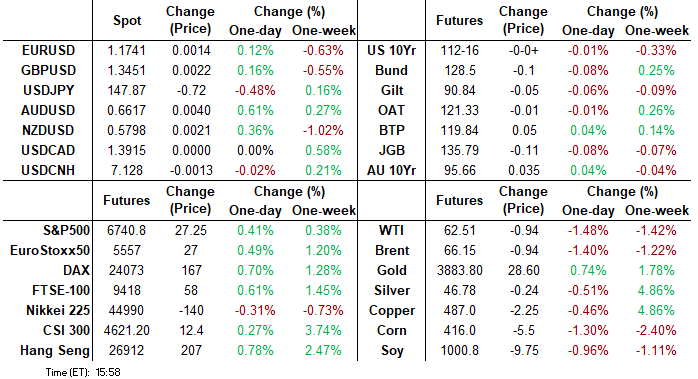

- Projected rate cut pricing gaining vs. late Monday levels (*): Oct'25 at -24.2bp (-22.7bp), Dec'25 at -44.2bp (-41.3bp), Jan'26 at -53.7bp (-50.7bp), Mar'26 at -64.7bp (-60.9bp).

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.13% (-0.03), volume: $2.893T

- Broad General Collateral Rate (BGCR): 4.12% (-0.02), volume: $1.146T

- Tri-Party General Collateral Rate (TCR): 4.12% (-0.02), volume: $1.110T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.09% (+0.00), volume: $89B

- Daily Overnight Bank Funding Rate: 4.09% (+0.00), volume: $174B

FED Reverse Repo Operation

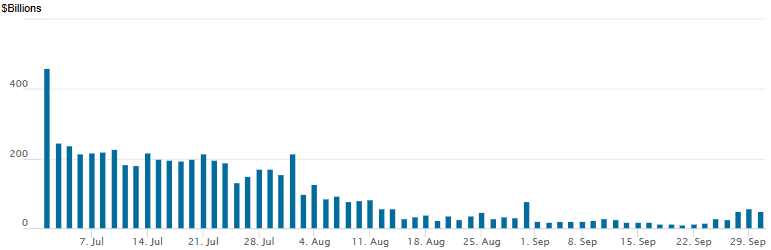

RRP usage slips to $49.071B into month end with 28 counterparties this afternoon from $56.220B Monday. Compares to $11.363B on Friday, September 16 - lowest level since early April 2021. The year's high usage stands at $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR/Treasury options revolved around low delta calls Tuesday, in addition to some chunky vol selling in the second half. Underlying futures have pared gains in the second half, curves twist steeper with short end rates outperforming. US Gov shutdown likely at midnight tonight. Projected rate cut pricing gaining vs. late Monday levels (*): Oct'25 at -24.2bp (-22.7bp), Dec'25 at -44.2bp (-41.3bp), Jan'26 at -53.7bp (-50.7bp), Mar'26 at -64.7bp (-60.9bp).

SOFR Options:

+15,000 SFRZ5 96.75 calls, 1.75 ref 96.31

-12,000 SFRX5 96.12/96.62 strangles, 1.75-2.0

-3,000 SFRV5 96.31 straddles, 6.25-6.0

-12,900 0QV5 96.93 calls 4.5 ref 96.905

26,000 SFRX5 96.50/96.56 call spds

2,000 2QZ5 97.18/97.43 call spds ref 96.805

2,500 SFRX5 95.93/96.00/96.06 put flys ref 96.295

5,000 0QZX5 96.37/97.62 strangles

+5,000 SFRF6 96.50/96.62/96.81 broken call flys, 0.5 ref 96.495

8,000 SFRZ5 96.06 puts ref 96.305

+1,500 0QZ5 96.50/96.62/96.75/96.87 put condors, 3.5 ref 96.90

10,000 SFRV5 96.43/96.50 call spds, 0.25-0.5 ref 96.34

+2,000 SFRZ5 96.18/96.31/96.50/96.62 put condors, 6.0

+4,000 SFRZ5 95.93/96.06/96.18 put flys, 2.25

Treasury Options:

+87,000 TYZ5 113 calls, 46 vs. 112-19/0.42% (open interest 87,527 coming into the session). Paper was a large buyer of low delta calls last week: +100,000 TYZ5 113.5 calls, 38 vs. 112-21 to -21.5/0.35% and appr +200k TYZ5 114 calls since Mon from 31-33.

+11,000 TYX5 111/112 put spds +1/-1 over 113.75 calls

8,600 FVX5 110 calls, 7.5 ref 109-07, total volume over 18.6k

10,000 TYZ5 113/113.5/114/114.5 4x4x4x3 call condors ref 112-19.5 to -20

4,400 FVX5 109.25/109.75/110/110.75 broken call condors, 6.5 ref 109-05.75/0.06%

2,000 TYX5 108.75/117.25 strangles ref 112-20

+3,300 Wed Weekly TY 112.5 calls, 16 (exp 10/01)

MNI BONDS: EGBs-GILTS CASH CLOSE: Modest Dip In Yields To Close The Month

European yields mostly fell Tuesday, to close September on a slightly positive note.

- Core FI saw an early bid with French flash September inflation softer-than-expected, and a US federal government shutdown on Oct 1 looming. German CPI was in line, but HICP was slightly above consensus (as was Italy's).

- On net ahead Wednesday's flash Eurozone HICP print, we track the Y/Y at 2.2-2.3%Y/Y, broadly in line with consensus coming into the week. In other data, there was little reaction to modest revisions to UK Q2 GDP.

- BOE's Breeden spoke toward the cash close, calling current policy restrictive and sounding supportive of easing policy but did not specify a timeline. UK STIR futures were little changed.

- The German curve twist steepened slightly, with UK yields modestly lower across the curve. Periphery/semi-core EGB spreads tightened a bit, helped by Spain lowering its net issuance target for the year by E5bln.

- The possible US government shutdown will bear attention after the cash close. Apart from the Eurozone inflation data, Wednesday's schedule includes final PMIs and appearances by ECB's Kazimir, Kocher, Simkus and Guindos, as well as BOE's Mann.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.4bps at 2.019%, 5-Yr is down 0.3bps at 2.309%, 10-Yr is up 0.4bps at 2.711%, and 30-Yr is up 0.8bps at 3.28%.

- UK: The 2-Yr yield is down 0.3bps at 3.985%, 5-Yr is down 0.9bps at 4.136%, 10-Yr is down 0.1bps at 4.699%, and 30-Yr is down 0.3bps at 5.506%.

- Italian BTP spread down 0.3bps at 82.3bps / French OAT down 0.5bps at 82.2bps

MNI EGB OPTIONS: Busy Session For Euribor Call Buying, Larger Bund Put Purchase

Tuesday's Europe rates/bond options flow included:

- RXX5 125p, bought for 2 in 10k

- ERH6 98.0625/98.1875cs vs 97.875p, bought the cs for 1.25 in 7k total

- ERH6 98.25/98.12/98.06/97.81p condor, bought for 0.75 in 2k

- ERH6 98.00/98.06/98.12/98.18c condor, bought for 0.25 for 4k

- ERM6 98.37c, bought for 3.25 in 12k

- 0RX5 98.06c vs 0RV5 98.00c, bought the Nov for 1 and 1.25 in 10k Total.

- SFIZ5 95.95/96.25^^, bought for 2 in 2k

- SFIF6 96.25/96.15ps 1x2, bought for 1.5 in 1k.

- SFIZ6 96.25/96.75/97.00cfly vs SFIM6 96.00p x2, traded 7.75 for the fly in 2.5k

MNI FOREX: AUD and JPY Lead G10 Advance as Dollar Dips Further

- Bearish dollar momentum continues to be a function of concerns related to the potential US government shutdown, which President Trump has said will probably occur. Haven demand for the Japanese yen has prompted USDJPY to fall another 0.5%, while a moderate hawkish tilt to the September RBA meeting promotes AUD to the top of the G10 leaderboard.

- USDJPY traded to a low of 147.66, with spot narrowing the gap to initial support which lies at 147.59, the 50-day EMA. Stronger pivot support has been defined at 145.49, the Sep 17 and post-Fed low.

- The broad dollar weakness has boosted AUDUSD back above the 0.66 handle on Tuesday. RBA Governor Michele Bullock declined to say whether the central bank retains an easing bias after the Board held the cash rate at 3.6%, stressing that future moves will depend on incoming data, with the current level still viewed as slightly restrictive.

- Overall, the AUDUSD uptrend remains intact and recent weakness appears to have been a correction. Initial firm resistance to watch at 0.6628 has been met today and will be closely monitored ahead of the APAC crossover. A stronger reversal higher would refocus attention on 0.6707, the Sep 17 and post-Fed high.

- Price action prompted another impressive surge for AUDNZD, rising to a fresh cycle high above 1.14, continuing to narrow the gap with the 2022 highs located at 1.1491.

- US data did little to spur volatility in currency markets. Job openings were relatively steady in August in the latest JOLTS report, but secondary metrics suggested further loosening in labor market conditions. Consumer confidence was weaker-than-expected.

- On Wednesday, the first focus will be on Japan’s Q3 Tankan Survey. Eurozone inflation data, US ADP employment and the ISM manufacturing PMI release are all scheduled.

MNI FX OPTIONS: Expiries for Oct01 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600-10(E3.3bln), $1.1700-10(E2.2bln), $1.1750-60(E2.1bln), $1.1775(E709mln), $1.1791-05(E1.9bln), $1.1900(E1.3bln), Y147.50($651mln), Y148.65-75($1.0bln)

- USD/JPY: Y146.15($864mln), Y146.40-50($1.7bln)

- EUR/JPY: Y175.00(E802mln)

- EUR/GBP: Gbp0.8780(E599mln)

- AUD/USD: $0.6600-10(A$1.1bln), $0.6700(A$1.6bln)

- USD/CAD: C$1.3900-10($655mln)

- USD/CNY: Cny7.1900($599mln)

MNI US STOCKS: Late Equities Roundup: Off Lows, Narrow Ranges Ahead Likely Shutdown

- Stocks continue to drift near steady (SPX eminis) to mildly negative late Tuesday, apprehension over a looming US government shutdown at midnight tonight keeping trading accounts at bay. Currently, the DJIA trades down 25.04 points (-0.05%) at 46284.74, S&P E-Minis up 6.5 points (0.1%) at 6719.5, Nasdaq down 0.8 points (0%) at 22588.13.

- Energy, Financial and Consumer Discretionary sector shares continued to lead decliners in the second half.

- Oil and gas stocks weaker as crude prices retreat even after OPEC issued a statement rejecting reports of production increases: Schlumberger -3.30%, Occidental Petroleum -2.91%, Halliburton -2.68%, Marathon Petroleum -2.53% and Phillips 66 -2.33%.

- A mix of financial services and travel related shares weighed on Financial and Consumer Discretionary sectors: Capital One Financial -5.83%, KKR & Co -5.57%, Apollo Global Management -5.53% and Blackstone -4.98%; MGM Resorts Int -6.21%, Expedia Group -3.40%, Las Vegas Sands -3.19% and Wynn Resorts -3.13%.

- On the positive side, Health Care and Information Technology sector shares led gainers. Pfizer climbed over 6% after headlines reported the pharmaceutical maker will get a three year grace period from Trump's drug tariffs. Merck & Co gained +4.85% and IQVIA Holdings +4.70%.

- Dell Technologies +3.71%, NVIDIA +2.51% and Super Micro Computer +2.91% supported the Tech sector.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Trend Needle Points North

- RES 4: 6812.29 2.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 3: 6800.00 Round number resistance

- RES 2: 6787.63 1.382 proj of the Aug 1 - 15 - 20 price swing

- RES 1: 6756.75 High Sep 22

- PRICE: 6733.50 @ 1601 ET Sep 30

- SUP 1: 6647.54 20-day EMA

- SUP 2: 6577.25 Low Sep 10

- SUP 3: 6533.46 50-day EMA

- SUP 4: 6481.75 Low Sep 3

A bull cycle in S&P E-Minis remains intact. Key short-term resistance has been defined at 6756.75, the Sep 22 high where a break would resume the primary uptrend. This would open 6787.63, a Fibonacci projection. On the downside, the contract has recently pierced initial support at the 20-day EMA, currently at 6647.54. A clear breach of this average would signal scope for a deeper retracement, potentially towards the 50-day EMA, at 6526.11.

MNI COMMODITIES: Crude Falls Amid Oversupply Concerns, Gold Hits Fresh Record High

- Crude has fallen further today ahead of Sunday’s OPEC meeting, amid conflicting reports on the size of a potential hike. Crude pared some losses after an OPEC statement rejected reports that the group is considering a 500k b/d increase.

- WTI Nov 25 is down by 1.5% at $62.5/bbl.

- The bloc’s retort came after a report from Bloomberg had suggested that OPEC is discussing fast tracking its latest round of supply hikes in three monthly instalments of about 500k b/d, while Reuters sources said it was around 411k b/d.

- The pullback in WTI futures refocuses attention on key support at $60.85, the Aug 13 low. A break of this level would reinstate the downtrend, with next support below there at $57.50, the May 30 low.

- Meanwhile, spot gold printed a new record high at $3,871/oz earlier today, before paring gains, with the yellow metal currently up by 0.4% at $3,849.

- The move comes ahead of a potential US government shutdown, which President Trump has said will probably occur.

- The trend condition in gold is unchanged, and a bull cycle remains in play. Today’s fresh cycle high confirms a resumption of the primary uptrend, with MA studies in a bull-mode position, highlighting a dominant uptrend.

- Sights are on $3,909.4 next, a Fibonacci projection. On the downside, support to watch lies at $3,681.6, the 20-day EMA. A pullback would be considered corrective.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 01/10/2025 | 0630/0830 | ** | Retail Sales | |

| 01/10/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 01/10/2025 | 0730/0930 | ECB Elderson Keynote at ECB Climate Conference | ||

| 01/10/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 01/10/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 01/10/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 01/10/2025 | 0755/0955 | ECB de Guindos Interview & Panel at Politico Summit | ||

| 01/10/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 01/10/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 01/10/2025 | 0900/1100 | *** | EZ HICP Flash | |

| 01/10/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 01/10/2025 | 0955/1055 | BOE Mann In Bloomberg Interview | ||

| 01/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 01/10/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 01/10/2025 | 1215/0815 | *** | ADP Employment Report | |

| 01/10/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/10/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 01/10/2025 | 1400/1000 | * | Construction Spending | |

| 01/10/2025 | 1400/1000 | * | Construction Spending | |

| 01/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 01/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 01/10/2025 | 1730/1330 | BOC Summary of Deliberations | ||

| 01/10/2025 | 1805/1405 | BOC Sr Deputy Rogers speaks at competition panel | ||

| 02/10/2025 | 0130/1130 | ** | Trade Balance |