MNI ASIA MARKETS ANALYSIS: Fed's Waller, Daly Favoring Dec Cut

HIGHLIGHTS

- Treasuries look to finish near session highs Monday, buoyed by dovish comments from Fed Gov Waller ahead of the NY open and by SF Fed Pres Daly on the close in an interview with the WSJ.

- Stocks are trading higher late Monday, buoyed by Fed Gov Waller comments on Fox Business - supportive of a December rate cut. Short covering also apparent ahead of Tuesday's heavy economic data calendar.

- Tuesday highlighted by retail sales and PPI inflation for September, although the Conference Board's consumer survey and its labor differential should also command attention.

- Heavy Tsy futures volumes tied to the Dec/Mar roll with 2s and 30Y Ultra-bond over 75% complete ahead Friday's First Notice when the Mar'26 contract takes lead.

US TSYS

MNI US TSYS: Remain Buoyed, SF Fed Daly Supports Dec Rate Cut

- Treasuries running at/near late session highs as SF Fed Pres Daly says she is supportive of a Dec rate cut in an interview with the Wall Street Journal, adding the "FED SHOULDN'T HOLD OFF ON RATE CUT OUT OF FEAR .. DISAGREEMENT AMONG OFFICIALS REFLECTS UNCERTAINTY" WSJ.

- Daly book-ends the session after early morning comments from Fed Gov Waller - "SINCE LAST FED MEETING AVAILABLE DATA SUGGESTS NOT MUCH CHANGE, INFLATION NOT A BIG PROBLEM WITH LABOR MARKET WEAK, ADVOCATING FOR A RATE CUT AT THE DECEMBER MEETING".

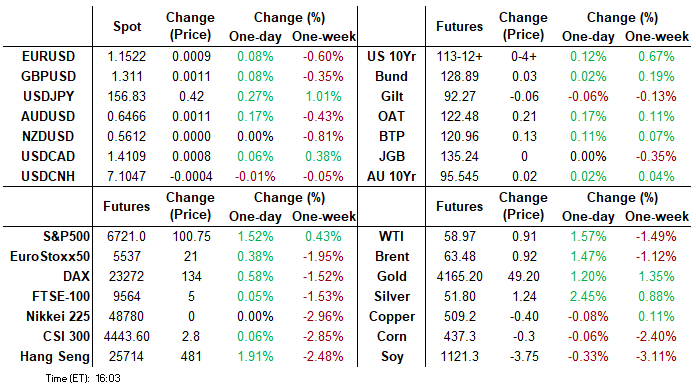

- Currently, TYZ5 trades +4 at 113-12 vs. 113-13 high. Last week’s breach of resistance at 113-02, an area of congestion since Nov 5, marks a bullish development and suggests scope for a climb towards 113-18+, the Oct 28 high. Note that the move higher also cancels a recent short-term bearish theme.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.93% (+0.02), volume: $3.203T

- Broad General Collateral Rate (BGCR): 3.90% (+0.04), volume: $1.276T

- Tri-Party General Collateral Rate (TCR): 3.90% (+0.04), volume: $1.251T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.88% (+0.00), volume: $81B

- Daily Overnight Bank Funding Rate: 3.88% (+0.00), volume: $174B

FED Reverse Repo Operation

RRP usage slips to $1.077B with 7 counterparties this afternoon from $2.503B Friday. Compares to last Tuesday's $0.905B - lowest level since mid-March 2021; this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

Decent two-way SOFR & Treasury option flow Monday, leaning towards low delta call plays as projected rate cut pricing near recent highs after dovish comments from Fed Gov Waller & SF Daly advocating for Dec rate cut after NY Fed Williams dovish comment on Friday. Current levels vs. early morning (*): Dec'25 at -20.1bp (-17bp), Jan'26 at -27.4bp (-26.1bp), Mar'26 at -35.5bp (-34.5bp), Apr'26 at -44.4bp (-44.1bp).

SOFR Options:

-10,000 0QF6 96.50/96.62/96.81/96.93 put condors, 4.0 ref 97.005

-20,000 SFRZ5 96.12 puts, 1.25

+3,000 SFRH6 96.37/96.50/96.68/96.81 call condors, 2.75 ref 96.45

-3,000 SFRZ5 96.31/96.37 call spds, 0.5 ref 96.24

+5,000 SFRH6 96.00 puts, 0.5 ref 96.435/0.05%

-5,000 SFRG6 96.00/96.12/96.25 put flys, 1.0

-10,000 SFRH6 96.06/96.25 2x1 put spds 1.5-1.75 ref 96.455

2,000 SFRZ5 96.12/96.18/96.25 put trees ref 96.235

2,000 SFRZ5 96.06/96.12/96.18 call flys ref 96.235

over 10,000 SFRZ5 96.31/96.43 call spds .75 ref 96.235

5,000 SFRZ5 96.25/96.31/96.37 call flys

2,000 SFRZ5 96.18/96.31/96.43/96.56 call condors ref 96.24

2,000 SFRZ5 96.37/96.50 call spds vs. 2QZ5 96.93/97.06 call spds

3,000 SFRZ5 96.12 straddles ref 96.2375

5,000 SFRZ5 96.31/96.37 call spds ref 96.2325

3,000 SFRZ5 96.25/96.31/96.37 call trees vs. 96.12 puts ref 96.23

over 5,000 SFRZ5 96.25/96.31 call spds ref 96.2275 to -.23

over 10,000 SFRZ5 96.12/96.25 call spds ref 96.23 to -.2275

2,200 SFRH6 96.18/96.31/96.43 2x3x1 put flys ref 96.445

1,850 SFRF6 96.37/96.68 strangles, ref 96.45

Treasury Options: (Dec options expired Friday)

2,000 USF6 119/121 call spds ref 117-08

1,500 FVF6 110 calls, 21.5 ref 109-23.25

7,500 wk1 TY/wk4 TY 113.25 call spds

3,000 TYF6 112/112.5 put spds ref 113-09

1,750 FVF6 108.75 puts ref 109-23

2,000 USF6 118/120/121 broken call flys ref 117-08

1,500 TYG6 113 straddles, 155

1,500 TYF6 113.5/114.5/115 broken call trees ref 113-06

2,700 TYG6 113.5 calls, 51 ref 113-06.5

MNI FOREX: Buoyant Equity Sentiment Unable to Dent Dollar Optimism

- The positive impulse for the major equity benchmarks on Monday has had very little effect on the dollar, as the USD index remains close to unchanged levels on the session. This keeps the DXY within close range of the recovery highs.

- Additionally, the uncertainty surrounding the Fed’s December decision in the absence of fresh data also provides a moderately supportive dollar tone. A break above 100.48 (May 29 high) would be a broader bullish development for the index.

- These dynamics have allowed USDJPY (0.30%) to extend its impressive post-election surge to around 6.3%, while positioning dynamics have also played their part, as the likes of USDZAR and USDBRL were among the best performing pairs last week.

- Geopolitics remain in focus for the Euro as European officials managed to push for some amendments on the Russia / Ukraine ceasefire deal proposed by the US. This initially provided a moderate boost for the single currency, with EURUSD rising to 1.1550 before reversing around 30 pips to current levels as we approach the APAC crossover.

- Overall, EURUSD continues to threaten a more meaningful break below the 1.15 handle and sights remain on key support at 1.1469, the Nov 5 low and a bear trigger.

- Amid the supportive tone for the greenback, USDCAD has spent the majority of Monday’s session consolidating back above 1.41, which keeps a bullish theme intact. Sights are on 1.4140, the Nov 5 high as the next important resistance. Note too that the top of the bull channel, drawn from the Jul 23 low, has moved up to 1.4185 and also represents a key resistance.

- For GBPUSD, spot has consolidated its bounce back to 1.31, leaving the pair around 90 pips above the cycle lows ahead of this week’s UK budget. Key short-term resistance is at the 20-day EMA, at 1.3167.

MNI FX OPTIONS: Expiries for Nov25 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1625(E1.4bln)

- USD/JPY: Y156.00($909mln)

- NZD/USD: $0.5600(N$600mln), $0.5720(N$646mln)

- USD/CNY: Cny7.00($1.2bln)

MNI US STOCKS: Late Equities Roundup: Tech & Communication Sectors Outperforming

- Stocks are trading higher late Monday, buoyed by Fed Gov Waller comments on Fox Business - supportive of a December rate cut. Short covering also apparent ahead of Tuesday's heavy economic data calendar.

- The tech-heavy Nasdaq outperformed as semiconductor makers continued to recover from mid-November selling, Communication Services sector shares close behind on the shortened Thanksgiving Holiday week.

- Currently, the DJIA trades up 231.66 points (0.5%) at 46476.58, S&P E-Minis up 99.75 points (1.51%) at 6719.75, Nasdaq up 581.2 points (2.6%) at 22853.09.

- Leading advances in late trade include: Broadcom +10.40%, Western Digital +9.08%, Micron Technology +8.11%, Tesla +7.65%, Seagate Technology +7.26%, AppLovin +6.27%, Lam Research +6.25%, Palantir Technologies +6.24% and Advanced Micro Devices +6.07%.

- Alphabet +5.93% and Meta Platforms +3.60% buoyed the Communication Services sector.

- Consumer Staples shares underperformed: General Mills -3.03%, Campbell's Company -2.80%, Procter & Gamble -2.77%, Target -2.59% and Kroger Co -2.48%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Key Support Remains Exposed

- RES 4: 6953.75 High Oct 30 and bull trigger

- RES 3: 6900.50 High Nov 12

- RES 2: 6735.63/6791.25 20-day EMA / High Nov 20

- RES 1: 6729.50 Intraday high

- PRICE: 6616.00 @ 14:47 ET Nov 24

- SUP 1: 6525.00 Low Nov 21

- SUP 2: 6500.00 Round number support

- SUP 3: 6476.62 23.6% retracement of the Apr 7 - Oct 30 uptrend

- SUP 4: 6427.00 Low Sep 2

S&P E-Minis remain in a short-term bear-mode condition and weakness last week reinforces current conditions. The breach of 6655.70, the Nov 7 low cancels recent bullish signals and signals scope for an extension of the corrective cycle. Sights are on 6540.25 (pierced), the Oct 10 low and a key support. A clear break of it would open 6476.62, a Fibonacci retracement point. Initial firm resistance to watch is 6735.63, the 20-day EMA.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 25/11/2025 | 0700/0800 | ** | PPI | |

| 25/11/2025 | 0700/0800 | *** | GDP (f) | |

| 25/11/2025 | 0745/0845 | ** | Consumer Sentiment | |

| 25/11/2025 | 0800/0900 | ** | PPI | |

| 25/11/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 25/11/2025 | 1100/1100 | ** | CBI Distributive Trades | |

| 25/11/2025 | 1330/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 25/11/2025 | 1330/0830 | *** | PPI | |

| 25/11/2025 | 1330/0830 | *** | PPI | |

| 25/11/2025 | 1330/0830 | *** | Retail Sales | |

| 25/11/2025 | 1330/0830 | *** | Retail Sales | |

| 25/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 25/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 25/11/2025 | 1400/0900 | ** | S&P Case-Shiller Home Price Index | |

| 25/11/2025 | 1400/0900 | ** | FHFA Home Price Index | |

| 25/11/2025 | 1400/0900 | ** | FHFA Home Price Index | |

| 25/11/2025 | 1400/0900 | ** | FHFA Quarterly Price Index | |

| 25/11/2025 | 1400/0900 | ** | FHFA Quarterly Price Index | |

| 25/11/2025 | 1400/1500 | ECB Cipollone Keynote at Central Bank of Ireland | ||

| 25/11/2025 | 1500/1000 | ** | NAR Pending Home Sales | |

| 25/11/2025 | 1500/1000 | *** | Conference Board Consumer Confidence | |

| 25/11/2025 | 1500/1000 | ** | Richmond Fed Survey | |

| 25/11/2025 | 1500/1000 | * | Business Inventories | |

| 25/11/2025 | 1500/1000 | * | Business Inventories | |

| 25/11/2025 | 1530/1030 | ** | Dallas Fed Services Survey | |

| 25/11/2025 | 1630/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 25/11/2025 | 1800/1300 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 25/11/2025 | 1800/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 26/11/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 26/11/2025 | 0030/1130 | *** | Quarterly construction work done | |

| 26/11/2025 | 0030/1130 | *** | CPI inflation | |

| 26/11/2025 | 0100/1400 | *** | RBNZ official cash rate decision |