MNI ASIA MARKETS ANALYSIS: Fed Gov Cook Dec is Live

HIGHLIGHTS

- Treasuries extended early lows after unexpectedly large corporate bond issuance announced

- Treasuries gapped back to pre-open level after lower than expected ISM Mfg & Prices paid data, undershooting implications from regional Fed surveys, MNI Chicago PMI and more optimistic S&P Global PMI.

- Fed Gov Cook says in a speech Monday that she viewed the decision to cut rates in October "as appropriate, because I believe that the downside risks to employment are greater than the upside risks to inflation."

US TSYS

MNI US TSYS: Fed Gov Cook: Dec Meeting Live; Tsy Borrow Reqs Lowered

- Treasuries look to finish steady (10s) to mixed, curves steeper (2s10s curve +.423 at 50.602) with the short end outperforming after the bell.

- Treasuries extended early lows after unexpectedly large corporate bond issuance announced ($40.5B with Alphabet making up $17.5B over 8 tranches) - only to gap back to pre-open level after lower than expected ISM Mfg & Prices paid data, undershooting implications from regional Fed surveys, MNI Chicago PMI and more optimistic S&P Global PMI.

- Fed Gov Cook says in a speech Monday that she viewed the decision to cut rates in October "as appropriate, because I believe that the downside risks to employment are greater than the upside risks to inflation", while noting that this cut was "another gradual step toward normalization" keeping rates "modestly restrictive, which is appropriate given that inflation remains somewhat above our 2 percent target."

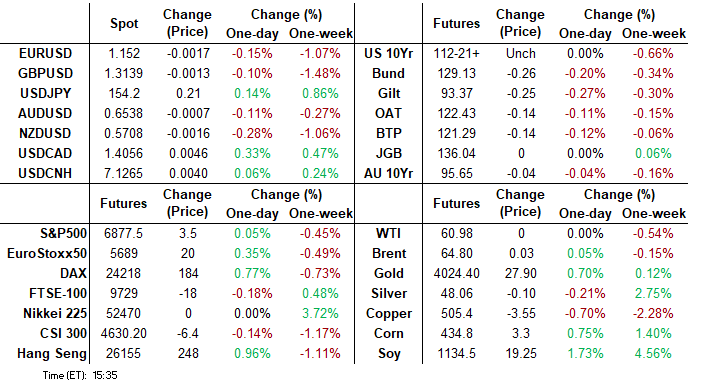

- Currently, the 10Y holds steady at 112-21.5, 10Y yield 4.1065% (+.0291). The contract has traded through the 50-day EMA, at 112-26+, highlighting potential for a deeper retracement near-term. A continuation lower would open 112-06, the Sep 25 low and the next key support. On the upside, the contract needs to trade above 113-18+, the Oct 28 high to signal a possible bullish reversal. Key resistance and the bull trigger is at 114-02, the Oct 17 high.

- The current quarter's borrowing requirements were lowered to $569B from August's $590B estimate. For the initial estimate of Jan-Mar requirements, a slight further uptick to $578B is seen. These borrowing estimates are below MNI's expectations and are at the lower end of most estimates we'd seen.

- Despite the greenback making initial further progress on Monday, the USD index rally has stalled just ahead of the psychological 100 mark, and the August highs at 100.25.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.22% (+0.18), volume: $3.211T

- Broad General Collateral Rate (BGCR): 4.15% (+0.16), volume: $1.153T

- Tri-Party General Collateral Rate (TCR): 4.15% (+0.16), volume: $1.117T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.86% (-0.01), volume: $107B

- Daily Overnight Bank Funding Rate: 3.86% (-0.01), volume: $195B

FED Reverse Repo Operation

RRP usage retreats to $23.792B with 18 counterparties going into month end - from $51.802B Friday. Compares to $2.435B on October 24 (lowest level since mid-March 2021) and the year's highest usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR/Treasury option flow remained mixed Monday, modest week-opener volumes with no Gov-tied data on day 34 of the shutdown. Underlying futures weaker out the curve, short end mildly higher. Projected rate cut pricing gains slightly vs. late Friday levels (*): Dec'25 at -16.4bp (-15.6bp), Jan'26 at -24.6bp (-23.5bp), Mar'26 at -32.9bp (-32.1bp), Apr'26 at -39.1bp (-38.5bp).

SOFR Options:

3,500 SFRZ5 96.06/96.12 put spds 1.75 ref 96.24

+7,500 0QF6 97.12/97.37/97.43/97.68 call condors, 3.0 vs. 96.905/0.10%

4,000 SFRZ5 96.18/96.31/96.43/96.56 call condors ref 96.245

7,000 SFRX5 96.37/96.50 call spds, 0.37 ref 96.235

2,000 SFRM6 96.62 straddles, 39.5

+7,000 0QF6 97.56 calls, 2.0 vs. 96.915/0.08%

+2,000 SFRF6 96.37 put 1.25 over 0QF6 96.75 puts

1,750 0QZ5 96.68/96.75/96.87 put trees ref 96.895

1,000 SFRZ5 96.18/96.37/96.56 2x3x1 put flys ref 96.245

1,250 SFRZ5 96.18/96.31 put spds ref 96.24

+2,500 SFRZ5 96.25/96.3125/96.4375/96.50 call condor, 3.25 vs. 96.27/0.05%

2,000 SFRZ5 96.12/96.18/96.25/96.31 call condors, 0.5

Block, 4,000 SFRZ5 96.12/96.18 2x1 put spds, 0.5 ref 96.245

Treasury Options:

5,000 TUG6 104.25 puts ref 104-10

+10,000 TYZ5 112.25/Mon wkly 112.5 put diagonal spd, 6

+1,000 FVF6 108.5/110.25 strangles 23 over FVZ5 108.25/110.5 strangles covered

+5,000 TYZ5 111/112 put spds, 8

-1,000 USF6 102/133 strangles, 2

5,000 wk2 TY 113 calls ref 112-26

MNI EGB BONDS: EGBs-GILTS CASH CLOSE: Bunds Underperform Amid Light Bear Steepening

European curve bear steepened modestly Monday, with Bunds underperforming.

- Global core FI was under pressure through much of the session due to large US corporate issuance.

- A softer-than-expected US ISM Manufacturing report triggered a relief rally in Treasuries that spilled over the Atlantic.

- However most of the session's damage was done toward the cash close though as EGB futures were sold in size, despite no obvious headline trigger for the move.

- In data, Spanish and Italian manufacturing PMIs improved more than expected in October.

- The UK and German curves each bear steepened very slightly, with Bunds slightly underperforming on the day. Periphery/semi-core EGB spreads tightened modestly.

- Tuesday's data schedule is light, with French budget data and Spanish labour market data, alongside several ECB speakers (including Lagarde and Rehn) and BOE's Breeden. In the UK, focus remains on pre-Budget fiscal speculation and setup ahead of this week's BoE decision.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3bps at 1.998%, 5-Yr is up 3.5bps at 2.268%, 10-Yr is up 3.4bps at 2.667%, and 30-Yr is up 4bps at 3.251%.

- UK: The 2-Yr yield is up 2.4bps at 3.795%, 5-Yr is up 2.5bps at 3.907%, 10-Yr is up 2.6bps at 4.435%, and 30-Yr is up 3bps at 5.208%.

- Italian BTP spread down 0.8bps at 74.3bps / French OAT down 0.4bps at 77.8bps

MNI EGB OPTIONS: Active Session In Sonia Includes Bull Flattener

Monday's Europe rates/bond options flow included:

- 0RH6 97.87/97.75/97.68/97.56p condor, bought for 2.5 in 4k

- SFIX5 96.20/96.15ps, sold at 1.25 in 3k

- SFIZ5 96.35/96.45cs, bought for 1.25 in 2k

- SFIZ5 96.35/96.50cs vs 0NZ5 96.70/96.90cs, bought the mid for 4.25 in 10k

- SFIH6 96.60c vs SFIM6 96.70c, bough the June for 5 in 4k

- +5k 0NZ5 96.70/96.90 cs vs -5k SFIZ5 96.35/96.50 cs, pays 3.75 to Buy the 0NZ5 cs (bull flattener)

MNI FOREX: August Highs Cap DXY Topside for Now, CHF & CAD Weakest in G10

- Despite the greenback making initial further progress on Monday, the USD index rally has stalled just ahead of the psychological 100 mark, and the August highs at 100.25. Additionally, weaker-than-expected ISM manufacturing and prices paid data have provided a moderate dollar headwind, especially against a backdrop of relatively few US data releases in recent weeks.

- Softer-than-expected CPI data in Switzerland this morning has resulted in the Swiss Franc being the weakest currency across the G10 today. EURCHF (+0.28%) held a significant medium-term support last week, and spot is now operating roughly 100 pips above the key 0.9206 level. A break back above 50-day EMA resistance at 0.9308 would be a bullish development, likely allowing the cross to re-establish the 0.93-0.94 range that was broadly in place between May/September.

- USDCAD's +0.30% Monday rally puts the pair on course for a third consecutive higher daily close but, more importantly, the pair is on course to test and break 1.4080 resistance to clear to the best levels since mid-April's Liberation Day. Tomorrow's Federal Budget in Canada remains a key risk with some analysts touting risks of a "significantly more expansionary than previous" annual budget. The next topside level would be 1.4111, the Apr 10 high.

- There was a slight divergence between the antipodeans to start the week, with AUDNZD trading to a fresh cycle high of 1.1461. Solid demand was found beneath 1.13 and the latest strength further narrows the gap towards the 2022 highs at 1.1491. A break of this level would place the cross at its highest point since 2013. The RBA decision highlights the APAC calendar on Tuesday, and NZ employment data is scheduled Wednesday.

- Other central bank decisions due later in the week include the Riksbank, Norges Bank and the Bank of England.

OPTIONS: Expiries for Nov4 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1475(E651mln), $1.1525(E1.1bln), $1.1635-40(E1.3bln)

- GBP/USD: $1.3150(Gbp510mln)

- AUD/USD: $0.6625-30(A$1.2bln)

MNI US STOCKS: Late Equities Roundup: Tech Heavy Nasdaq Still Outperforms

- Stocks remain mixed late Monday, inside session ranges while the tech-heavy Nasdaq still outperforms. Currently, the DJIA trades down 243.74 points (-0.51%) at 47327.76, S&P E-Minis down 2.75 points (-0.04%) at 6873 Nasdaq up 98.6 points (0.4%) at 23829.47.

- Consumer Discretionary and Information Technology sector shares continued to lead advances in the second half, Amazon.com +4.58%, Tesla +2.07% and Wynn Resorts +4.82% led the former, while IT supported by: Western Digital +5.75%, Micron Technology +5.28%, Seagate Technology +4.55%, Palantir Technologies +3.28% and NVIDIA +3.22%.

- Conversely, a mix of Consumer Staples, Materials and Financials sector shares led declines in late trade:

- Kimberly-Clark -14.25%, Hershey Co -4.26%, Estee Lauder -2.66%, Colgate-Palmolive -2.19% and Kraft Heinz -2.16%.

- International Paper -4.58%, PPG Industries -2.58%, Albemarle -2.52%, Dow -2.45% and Eastman Chemical -2.15%

- Coinbase Global -4.07%, Arthur J Gallagher -2.25%, Fiserv -2.16%, Brown & Brown -2.06% and Erie Indemnity -1.99%

- Earnings expected after the close include: Qorvo Inc, Clorox, Navitas Semiconductor, Hims & Hers Health Inc, Palantir Technologies, Solaris Energy Infrastructer, Williams Cos, Vertex Pharmaceuticals and Comstock Resources.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Path Of Least Resistance Remains Up

- RES 4: 7000.00 Psychological round number

- RES 3: 6993.12 3.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6974.04 3.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 1: 6953.75 High Oct 30

- PRICE: 6882.00 @ 1441 ET Nov 3

- SUP 1: 6812.25/6795.74 High Oct 9 / 20-day EMA

- SUP 2: 6690.58 50-day EMA

- SUP 3: 6540.25 Low Oct 10 and a key short-term support

- SUP 4: 6506.50 Low Sep 5

The trend condition in S&P E-Minis is unchanged, it remains bullish and the latest pullback appears corrective. The fresh cycle high last week confirms a resumption of the primary uptrend and maintains the bullish price sequence of higher highs and higher lows. Sights are on 6974.04 next, a Fibonacci projection point. Initial firm support to watch lies at 6795.74, the 20-day EMA. Key pivot support lies at 6690.58, the 50-day EMA.

COMMODITIES

MNI AMERICAS OIL: US OIL: November 3 - Americas End of Day Oil Summary: Crude Sideways

US OIL: November 3 - Americas End of Day Oil Summary: Crude Sideways

WTI crude prices ended the day nearly unchanged after earlier rallying without a clear headline driver. The market had previously been weighing OPEC’s decision to increase the output target in December by 137kb/d with the announcement that it would pause production rises through Q1 during seasonal lower demand. Sanctions on Russian oil are also in the spotlight.

- OPEC Secretary-General said the group have the flexibility to alter, pause or reverse decisions and are making sure to maintain the supply demand balance. OPEC sees good signs for demand with growth at 1.3mb/d this year.

- Morgan Stanley has lifted its Brent forecast by $2.50/bbl to $60/bbl for Q1, after OPEC decided to leave production targets unchanged over Jan-Mar, according to Bloomberg.

- The OPEC halt appears to preserve “policy optionality for any eventuality” amid uncertain supply and anticipated demand softness, according to RBC cited by Bloomberg.

- WTI Dec futures were up 0.1% at $61.05

- WTI Jan futures were up 0.2% at $60.73

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 04/11/2025 | 0740/0840 | ECB Lagarde Keynote Speech At Bulgarian National Bank | ||

| 04/11/2025 | 0745/0845 | Budget Balance | ||

| 04/11/2025 | 0945/1045 | ECB Lagarde At Bulgarian National Bank Press Conference | ||

| 04/11/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 04/11/2025 | 1135/0635 | Fed Vice Chair Michelle Bowman | ||

| 04/11/2025 | 1140/1140 | BOE Breeden at International Banking Conference | ||

| 04/11/2025 | 1330/0830 | ** | Trade Balance | |

| 04/11/2025 | 1330/0830 | ** | Trade Balance | |

| 04/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 04/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 04/11/2025 | 1500/1000 | *** | JOLTS jobs opening level | |

| 04/11/2025 | 1500/1000 | *** | JOLTS quits Rate | |

| 04/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 04/11/2025 | 2100/1600 | Canada federal budget, release expected just after 4pm EST | ||

| 05/11/2025 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 05/11/2025 | 2200/0900 | ** | S&P Global Final Australia Composite PMI | |

| 05/11/2025 | - | Riksbank Meeting | ||

| 05/11/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 05/11/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI |