MNI ASIA MARKETS ANALYSIS: EU Prepared To Respond US Tariffs

HIGHLIGHTS

- Treasuries look to finish near late Tuesday session highs, partially buoyed by weaker stocks, decent 10Y auction and headlines the EU is prepared to slap E100B in tariffs on US goods if trade negotiations fail.

- Little react to data - final March trade data confirmed a new record (nominal) deficit and the largest on a relative basis since 2005/06 at -$140.5B.

- Main focus on Wednesday's FOMC policy announcement: steady rate and no meaningful changes in the Statement expected.

US TSYS

MNI US TSYS: Near Late Highs, Curves Off Highs As Bonds Gain Ahead Wednesday FOMC

- Treasuries look to finish near late Tuesday session highs, early curve steepening consolidating as 30Y Bonds pulled higher late. Main focus on Wednesday's FOMC policy annc.

- Steady rate and no meaningful changes in the Statement expected, though any signal that the Fed is looking seriously at “soft” survey data to assess the outlook could be significant.

- Final March trade data confirmed a new record (-$140.5B nominal) deficit and the largest on a relative basis since 2005/06 in the imbalances ahead of the Great Financial Crisis. However, pharmaceutical tariff front-running and continued heavy imports of gold are greatly clouding interpretation of underlying trends.

- Early short end support after latest tariff-related headlines: EU to target E100B of US goods if trade negotiations fail. Meanwhile, decent $42B 10Y Note auction stops 1.3bp through: drawing 4.342% high yield vs. 4.355% WI.

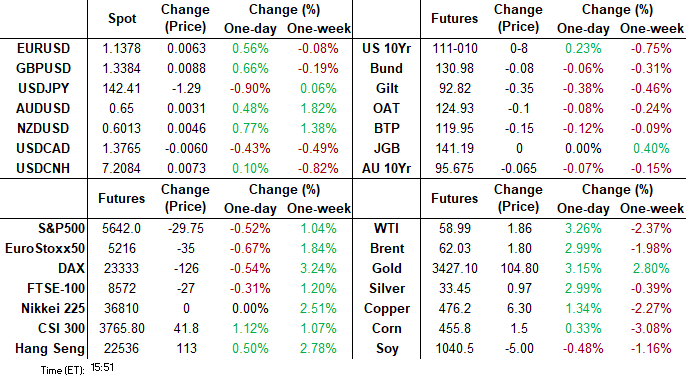

- Tsy Jun'25 10Y futures currently +7.5 at 111-09.5 vs. 111-11.5 high, initial technical resistance well above at 112-01.5 (High May 2). For bulls, price needs to trade above key short-term resistance at 112-20+, the May 1 high, to reinstate a bullish theme.

- Cross asset roundup: Bbg US$ index near late lows (BBDXY -3.49 at 1217.28), Gold plowing higher late (3416.95 - not for off April 22 all-time high of 3494.52), Crude rebounding (WTI +1.87 at 59.0.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.33% (-0.03), volume: $2.632T

- Broad General Collateral Rate (BGCR): 4.31% (-0.02), volume: $1.072T

- Tri-Party General Collateral Rate (TCR): 4.31% (-0.02), volume: $1.026T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $117B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $293B

FED Reverse Repo Operation

RRP usage inches up to $129.858B this afternoon from $124.690B yesterday, total number of counterparties at 34. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option volumes gradually improved Tuesday, flow shifted from low delta put trade to more pared with some upside call structures as underlying pared losses ahead of Wednesday's FOMC, curves mildly steeper/well off early highs. Projected rate cut pricing gains slightly vs. late Monday levels (*) as follows: May'25 steady at -0.5bp, Jun'25 steady at -8.4bp, Jul'25 steady at -25.2bp, Sep'25 -46.2bp (-45.3bp).

SOFR Options:

+20,000 0QU5 97.25/97.75 call spds 6.0-6.5 over SFRN5 96.75 calls

+5,000 SFRN5 95.75/95.87/96.00 put flys, 2.25

+8,000 SFRN5 95.50/95.62/95.75/95.87 put condors, 2.0 ref 96.16

+5,000 SFRH6 97.25/98.25 call spds .25 over 2QH6 97.12/98.12 call spds

+5,000 SFRZ5 96.50/2QZ5 96.75 call spds, 0.5

+25,000 SFRU5 96.75/97.50 call spds, 4.75 ref 96.16

8,250 0QZ5 96.25/96.37 put spds ref 96.85 to -.855

+2,500 SFRZ5 call spds, 4.0 ref 96.46

-2,000 SFRK5 95.87/95.93 put spds, 5.75

Block, 5,000 SFRM5 95.62 puts, 0.5 vs. 95.765/0.10%

3,000 SFRQ5 96.25/0QQ5 97.25 call spds

5,500 0QU5 97.25/97.75 call spds ref 96.845

2,500 SFRN5 95.68/95.75/95.87 2x3x1 put flys

5,000 SFRK5 95.75/95.81 put spds ref 95.795

6,000 SFRN5 96.25/97.25 call spds ref 96.15

3,000 SFRV5 95.62/95.75 2x1 put spds

2,500 SFRM5 95.75 puts ref 95.79

2,000 SFRK5 95.75/95.87 strangles, ref 95.785

Treasury Options:

Block, -7,500 wk2 TY 109.75/110.25/110.75/111.25 put condors, 13.0

+10,000 wk2 FV 108.75/109 call spds, 3

Block, 10,000 TYN5 108.5 puts, 15 vs. 111-04/0.19%

1,500 TUM5 103.37 puts vs. 103.75/104 call spds

7,300 TYN5 109 puts, 22 ref 111-07

over 7,000 FVM5 108.25/109.25 1x2 call spds, 11

1,000 FVM5 107.25/108.25 put spds vs. 108.25/109.25 call spds ref 108-12

over 5,300 wk2 TY 110.5 puts, 9 ref 110-29.5 (exp 5/9)

1,600 TYM5 109.25 puts, ref 111-00

MNI FOREX: Trump’s Big Imminent Announcement Unable to Curtail USD Weakness

- US yields have moved lower on Tuesday, which alongside some downward pressure on equity benchmarks, have enabled the underlying trend of a weakening dollar to prevail through the session. Having respected its 20-day exponential moving average well, the USD index is now back below 99.50, highlighting that the recent move above 100 in early May appears to be technically corrective.

- This dynamic sees the Japanese Yen as the best performer, with USDJPY comfortably back below the 143.00 mark, having entirely eroded the post-BOJ upswing from last week. Even the late rhetoric from President Trump suggesting there will be a “very big” positive announcement in the coming days was quickly brushed aside. The trend direction in USDJPY remains bearish and gains since Apr 22 are considered corrective. This refocuses short-term attention on initial support at 141.97, the Apr 29 low.

- Divergence between the low yielders is also notable today, as CHFJPY weakens around 0.85%. 176.00 has provided an important pivot point this year for that cross, and this week’s selloff bolsters the short-term significance of that resistance level. Moves have been underpinned by a more concerned tone regarding Swiss Franc strength from SNB President Schlegel, potentially highlighting that the risk reward for further Franc gains may be diminishing at this juncture.

- Elsewhere, gains for G10 currencies have largely mirrored the adjustment for the DXY, with the likes of EUR, GBP, AUD, NZD and CAD all rising around half a percent.

- Notably, USDCAD printed fresh cycle lows as President Trump made comments on the USMCA being still very effective and potentially not needing to be renegotiated. A dominant downtrend is in place for USDCAD, signalling scope for a move towards 1.3643, the Oct 9 ’24 low.

MNI OPTIONS: Expiries for May07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1400(E763mln)

- USD/JPY: Y142.50($804mln), Y143.00($595mln), Y143.20($746mln), Y145.50-55($1.1bln), Y145.85-00($1.6bln)

- EUR/GBP: Gbp0.8555-68(E501mln)

- AUD/USD: $0.6400(A$676mln), $0.6600(A$717mln)

- USD/CAD: C$1.3750-65825mln), C$1.3775-80($961mln)

- USD/CNY: Cny7.2000($500mln)

EQUITIES

MNI US STOCKS: Late Equities Roundup: Utilities & Energy Sectors Outperform

- Stocks continue to trade weaker late Tuesday, but off morning lows, buoyed by Utilities and Energy sectors as crude prices rebound (WTI +1.93 at 59.06). Currently, the DJIA trades down 304.04 points (-0.74%) at 40914.08, S&P E-Minis down 29.75 points (-0.52%) at 5642, Nasdaq down 107.1 points (-0.6%) at 17737.53.

- Constellation Energy surged 12.22% after missing earnings but revenues beat ($6.8B), Vistra +4.56%, Duke Energy +2.64% and AES Corp +2.19%. Leading oil and gas stocks included APA +2.16%, Marathon +1.97%, Exxon Mobil +1.70%, Occidental Petroleum +1.44% and Kinder Morgan +1.04%.

- Conversely, Health Care and Information Technology sectors underperformed, pharmaceuticals weighing on the former: Vertex Pharmaceuticals -11.69% on light first quarter sales, Moderna -11.68%, Regeneron Pharmaceuticals -6.76% and Eli Lilly -5.41%.

- Meanwhile, Information Technology sector shares underperformed: despite better than expected earnings, Palantir Technologies fell 11.69% as analysts raise international growth concerns; elsewhere, Teradyne -1.71% and Intel Corp -1.50%.

- The latest earnings cycle is approximately 76.8% complete (by market cap of the S&P 500). Earnings expected after today's close include: Cytokinetics Inc, Lucid Group, Arista Networks, Advanced Micro Devices, Rivian Automotive, Astera Labs, International Flavors & Fragrances, Electronic Arts, Mosaic, Wynn Resorts, Eos Energy, Devon Energy and Super Micro Computer.

MNI EQUITY TECHS: E-MINI S&P: (M5) Bull Cycle Intact

- RES 4: 5864.93 200-dma

- RES 3: 5837.25 High Mar 25 and a bull trigger

- RES 2: 5773.25 High Apr 2

- RES 1: 5724.75 High May 2

- PRICE: 5641.00 @ 14:35 ET May 6

- SUP 1: 5527.21 20-day EMA

- SUP 2: 5355.25/5127.25 Low Apr 24 / 21 and a key support

- SUP 3: 4996.43 76.4% retracement of the Apr 7 - 10 bounce

- SUP 4: 4832.00 Low Apr 7 and the bear trigger

Recent gains in the e-mini S&P reinforce current bullish conditions.The contract has breached the 50-day EMA, at 5622.87. A continuation of the bull phase would expose 5837.25 next, the Mar 25 high and a bull trigger. It is still possible that the entire rally since Apr 7 is a correction. A reversal lower would signal the end of this corrective phase and expose initially, support at 5127.25, the Apr 21 low. First support to watch is 5527.21, the 20-day EMA.

MNI COMMODITIES: Crude Rebounds Amid Mid-East Tensions, Gold Recovers

- Crude has rebounded back to levels seen late last week amidst signs of rising tensions in the Middle East, while the market continues to digest oversupply risks after OPEC+ decided on a large output hike for June.

- WTI June 25 is up by 3.6% at $59.2/bbl.

- OPEC+ agreed to increase output by 411k b/d in June, following a similar rise in May.

- A medium-term bearish trend in WTI futures remains intact and short-term gains are considered corrective.

- Attention is on $54.67, the Apr 9 low and a bear trigger. Resistance to watch is $64.13, the 50-day EMA.

- Meanwhile, gold has rallied by a further 2.5% today to $3,417/oz, taking total gains this week to over 5%.

- The move comes amid a further decline in the dollar, which will have provided some support to the price of gold, along with continued haven demand stemming from ongoing tariff and geopolitical uncertainty.

- The rally in gold this week suggests that the correction between Apr 22 - May 1 is over. A continuation higher would refocus attention on key resistance and the bull trigger at $3,500.1, the Apr 22 all-time high. Clearance of this level would confirm a resumption of the primary uptrend.

- Elsewhere, copper has also rallied by a further 1.3% to $476/lb, taking total gains this week to almost 2%.

- For copper, key short-term resistance has been defined at $498.25, the Apr 23 high. A resumption of weakness would expose $436.00, the Apr 10 low.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 07/05/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 07/05/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 07/05/2025 | 0645/0845 | * | Foreign Trade | |

| 07/05/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 07/05/2025 | 0800/1000 | * | Retail Sales | |

| 07/05/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 07/05/2025 | 0900/1100 | ** | Retail Sales | |

| 07/05/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 07/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 07/05/2025 | 1400/1000 | Treasury Secretary Scott Bessent | ||

| 07/05/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 07/05/2025 | 1800/1400 | *** | FOMC Statement | |

| 07/05/2025 | 1900/1500 | * | Consumer Credit | |

| 08/05/2025 | - | NorgesBank Meeting |