MNI ASIA MARKETS ANALYSIS: Equities, USD Pick Up Post-Holiday

MNI (NEW YORK) -

HIGHLIGHTS:

- Cash equities saw a broad-based rally in return from UK/US holidays, with the dollar firming

- Long-end bonds consolidate overnight JGB-led outperformance in return from US/UK holidays

- RBNZ decision (25bp cut expected) and Australia CPI are coming up

US TSYS: Bull Flattening In Return From Long Weekend

The cash Treasuries curve bull flattened Tuesday in the return to trading after the Memorial Day weekend.

- Global core FI was roundly boosted by soaring long-end JGBs on an overnight Reuters report that the Japanese finance ministry was considering shifting its issuance profile away from long-dated paper.

- Data broadly confirmed the narrative of US economic stabilization, with durable goods orders softer but not necessarily falling off a cliff in April, and Conference Board consumer confidence surprisingly bounced in May (though the so-called labor differential weakened in a possible warning sign for the labor market).

- In supply, the 2Y Note was well digested (1bp trade-through was the best since February), helping consolidate Treasury gains through the afternoon session.

- The June/September futures roll picked up where it left off last week, with most contracts now around two-thirds complete.

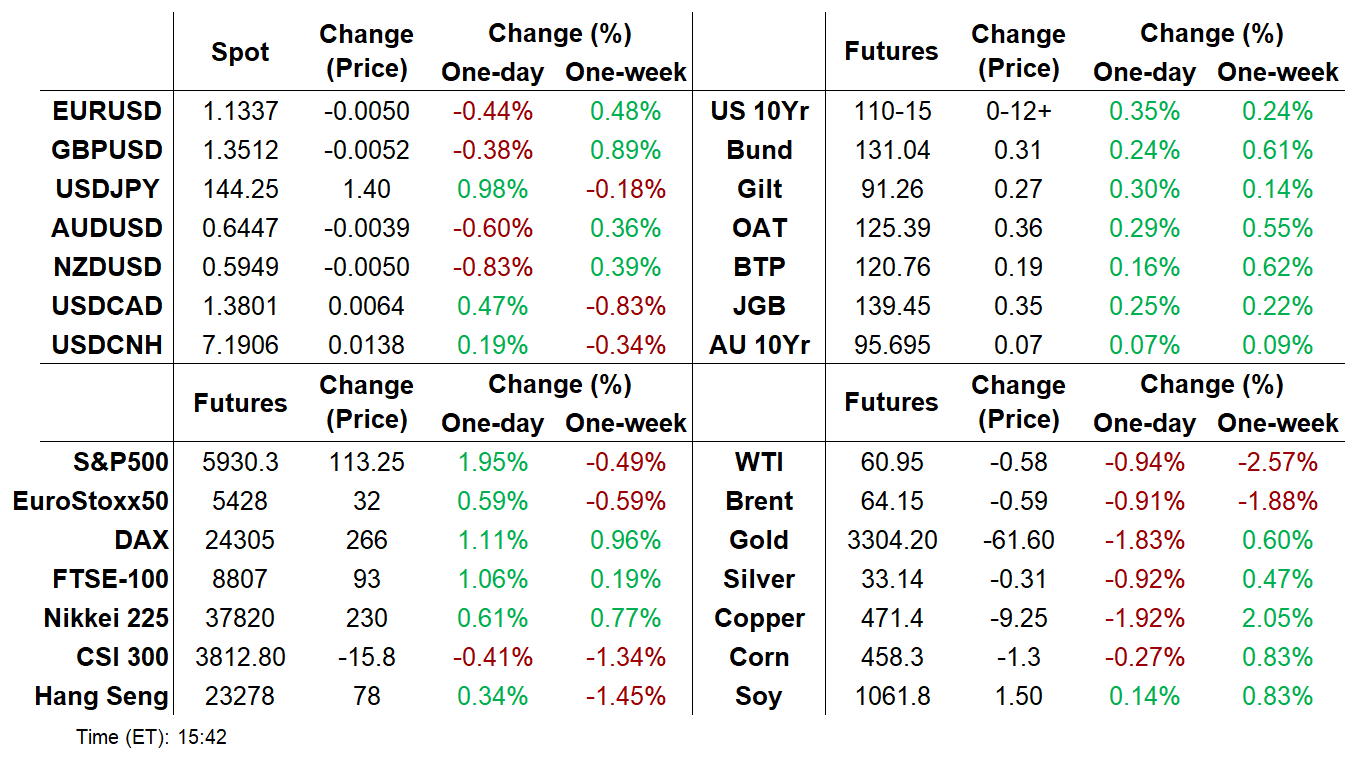

- Latest cash levels: The 2-Yr yield is down 1.9bps at 3.9723%, 5-Yr is down 5.1bps at 4.0298%, 10-Yr is down 7.1bps at 4.4397%, and 30-Yr is down 9.2bps at 4.9459%. The Jun 25 T-Note future is up 12/32 at 110-14.5, having traded in a range of 109-24.5 to 110-18.

- Wednesday's calendar includes more regional Fed surveys (Richmond services/manufacturing, Dallas services) and an appearance by FOMC's Kashkari, with supply including 2Y FRN and 5Y Note. We then get the minutes of the May FOMC meeting in the afternoon.

MNI RBNZ Preview-May 2025: May 25bp Cut, Then?

- Download full report here.

- The RBNZ decision is announced on May 28 and rates are widely expected to be cut 25bp to 3.25% bringing total easing this cycle to 225bp. 23 out of 24 analysts surveyed by Bloomberg are forecasting this outcome.

- Given heightened uncertainty, the MPC is likely to retain its easing bias again stating it has “scope” to cut rates further if required and its updated OCR path will be scrutinised to this end. A downward revision bringing the terminal to below 3%, estimated 'neutral', would signal a need for accommodation.

- The attention will be on the medium-term which is likely to show a softer outlook driven by weaker trading-partner growth due to recent global uncertainty. The RBNZ said in April that “on balance, these developments create downward risks to the outlook for economic activity and inflation in New Zealand”.

- Markets continue to price in 25bps of easing for the May meeting, with a total of 64bps expected by November 2025.

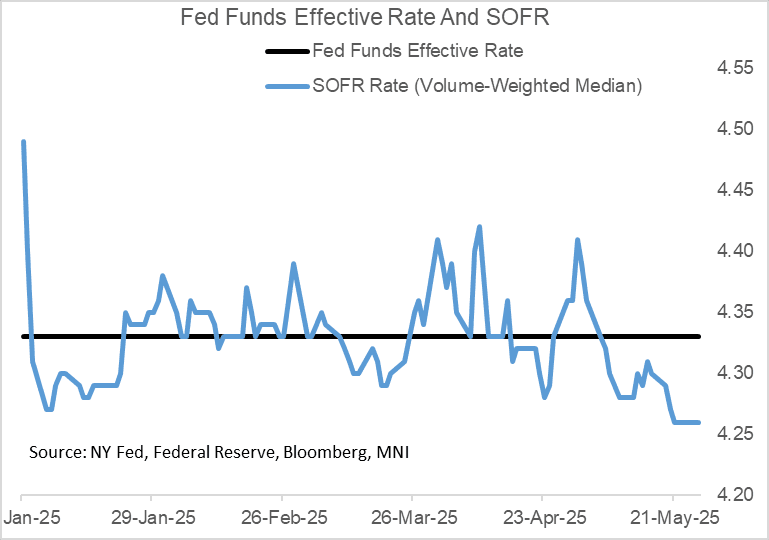

US TSYS/OVERNIGHT REPO: SOFR Remained Subdued Last Week, But Should Pick Up

Secured rates remained soft on Friday, with SOFR unchanged vs Thursday at 4.26%. SOFR was softer than most had anticipated last week, with GSE cash inflows appearing to weigh down rates for an extended period, but that effect should start to dissipate with rates picking up this week.

- Upside pressures will be exacerbated by Friday's month-end dynamics, with Thursday seeing $46B in net new cash raised via coupon auction settlements, though Wednesday's rates could be subdued in the meantime by $29B in net bill paydown.

- As usual, Fed funds rates remained at 4.33%.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.26%, no change, $2542B

* Broad General Collateral Rate (BGCR): 4.26%, no change, $1048B

* Tri-Party General Collateral Rate (TGCR): 4.26%, no change, $1013B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.33%, no change, volume: $123B

* Daily Overnight Bank Funding Rate: 4.33%, no change, volume: $305B

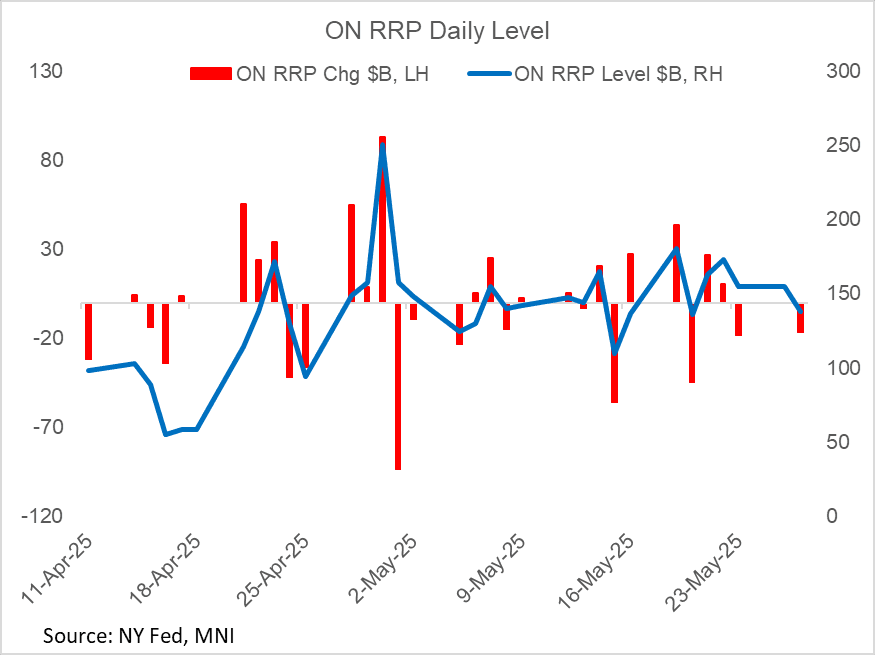

US TSYS/OVERNIGHT REPO: Reverse Repo Takeup Dips, Within Recent Ranges

Takeup of the Fed's overnight reverse repo facility fell $16.7B to $138.1B Tuesday, in the return from the Memorial Day weekend.

- That's the lowest level since May 20, with the pullback in facility usage since the start of last week ($180B high) potentially reflecting a pullback of GSE cash from markets.

- Takeup is next expected to rise at the end of the week, reflecting end-month dynamics.

BONDS: EGBs-GILTS CASH CLOSE: Long-Ends Outperform

European yields were mixed Tuesday, with long-end bonds outperforming.

- Yields dropped in early trade following a large Japanese government bond rally overnight, with longer-end US and German instruments outperforming for the day.

- From the morning lows though, yields edged higher through the session as equities gained.

- In particular, Gilt yields caught up after Monday's holiday with a broader risk-on sentiment coming out of the weekend, following US President Trump's decision to postpone new tariffs on the EU (from an originally announced June 1 date) pending talks.

- French flash May inflation was much softer than expected, helping EGB short-end outperform the UK; the EC's May confidence surveys saw an improvement in May following the US/China tariff de-escalation (but pre-EU/US back-and-forth).

- In ECB-speak, Lane noted the ECB will cut rates further if it sees signs of further falling inflation; Nagel didn't explicitly lean towards a June ECB cut or hold.

- The German and UK curves both curve twist flattened. EGB periphery / semi-core spreads were flat/slightly tighter.

- Wednesday's calendar includes an appearance by BOE's Pill, and the ECB CPI expectations survey.

Closing Yields / 10-Yr EGB Spreads To Germany:

- Germany: The 2-Yr yield is up 0.9bps at 1.791%, 5-Yr is down 0.6bps at 2.093%, 10-Yr is down 2.8bps at 2.532%, and 30-Yr is down 6.3bps at 3.002%.

- UK: The 2-Yr yield is up 3.7bps at 4.02%, 5-Yr is up 2.2bps at 4.152%, 10-Yr is down 1.5bps at 4.666%, and 30-Yr is down 4.5bps at 5.435%.

- Italian BTP spread down 0.9bps at 98.5bps / Portuguese down 0.9bps at 49.4bps

EU FI OPTIONS: Light Call Fly Buying Bought In UK Return From Holidays

Tuesday's Europe rates/bond options flow included:

- ERQ5 98.00/98.12/98.25c fly, bought for 3.25 in 3k

- ERZ5 98.25/98.37cs, sold at 5 in 5k

- SFIQ5 96.05/96.15/96.25c fly, bought for 2 in 2k

US Options Roundup - May 27 2025

Tuesday's US rates options flow included:

- SFRU5 95.87/95.75ps 1x2, with 95.93/95.75ps 1x2, bought the strip for 3.25 in 5k

- SFRZ5 96.50/97.00cs vs 95.87p, traded for 3 in 2k

- SFRZ5 96.00/65.62ps 1x2, traded 11.5 in 3.5k

- TYN5 107.5 put bought for 4 in 20k

FOREX: USD Index Trades with More Constructive Tone, JPY Underperforms

- The greenback trades on a firmer footing on Tuesday alongside the step lower for long-end core yields and the prevailing optimism for major equity benchmarks. As noted, long-end JGBs are outperforming after Reuters sources suggested the MOF will consider skewing the composition of its current issuance programme away from super-long-end instruments.

- This dynamic has helped USDJPY extend its intra-day recovery to around 1.65% on the session, narrowing the gap to the initial resistance zone at 144.40, last Thursday’s high and the 20-day EMA. Above here, the 50-day EMA currently intersects at 145.73.

- NZD and AUD also sit among the worst performers in G10 on Tuesday, shrugging off the more optimistic tone for global equities and taking its cues from the broader dollar rebound. Today’s 0.95% selloff has seen NZDUSD gravitate back below 0.6000 handle, as a cluster of US election related highs between 0.6025/38 continue to cap the topside for the pair.

- GBPs more modest 0.45% dip lower stands out in G10, and underpins the prevailing bullish/resilient theme for GBPUSD. The break of 1.3444 (Apr 28 / 29 high) remains significant here, confirming a resumption of the technical uptrend. This allowed the pair to print fresh cycle highs of 1.3593 on Monday, narrowing the gap substantially to 1.3605, a Fibonacci retracement. Moving average studies continue to highlight a dominant uptrend. First support lies at 1.3351, the 20-day EMA.

- Spillover USD buying is, in turn, meeting a weaker EUR after this morning's soft French CPI print and the resultant losses for EUR/USD are closing the gap with the 1.13 handle support and sizeable option strikes set to roll off at tomorrow's NY cut (which also happens to be value date month-end).

- Australia CPI and the RBNZ (expected to cut 25bp to 3.25%) decision will take focus on Wednesday. Later in the session, the FOMC minutes are also scheduled.

FX OPTIONS: Expiries for May28 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1300(E1.4bln), $1.1390-00(E1.4bln), $1.1445-55(E1.0bln), $1.1500-20(E1.4bln)

- USD/JPY: Y141.00($1.3bln), Y141.75-80($990mln), Y143.00($2.0bln), Y143.90-00($1.9bln), Y145.00($1.8bln)

- AUD/USD: $0.6325-30(A$500mln)

- NZD/USD: $0.5725(N$1.1bln)

EQUITIES: Tech, Cyclicals Lead Broad Gains

Equities were bid Tuesday with the S&P 500 experiencing a strong and broad rally, up 2% in late trade with cyclical stocks leading the way for the most part. Market breadth was positive, with 94% of securities set to finish the day higher.

- After some weakness at the cash open, it looked as though futures would be unable to advance from their gains coming into the weekend (cash was closed Monday for holidays), but the rest of the session saw a steady rally to the best levels since May 21 on a US-EU tariff reprieve and the Treasury market regaining ground.

- Leading the cash gains were growth-oriented sectors: Consumer Discretionary equities were the top performer, surging +2.7%, with Tech also saw significant gains, rising +2.4%. Communication Services followed with a solid +1.97% increase.

- NVidia (+3%), Oracle (+3.8%) and Apple (+2.6%) were notable gainers, the latter after a prolonged multi-day tariff-related selloff, and Tesla rising 5.9% to the best levels since mid-February.

- All sectors finished in positive territory. Even the day's relative underperformers posted gains: Energy was up +0.8%. Consumer Staples rose +0.9%, with Utilities up +1.1%.

EQUITY TECHS: E-MINI S&P: (M5) Support Remains Intact

- RES 4: 6080.75 High Feb 26

- RES 3: 6057.00 High Mar 3

- RES 2: 6000.00 Round number resistance

- RES 1: 5993.50 High May 20 and the bull trigger

- PRICE: 5882.50 @ 14:32 BST May 27

- SUP 1: 5756.50/5719.58 Low May 23 / 50-day EMA and key support

- SUP 2: 5596.00 Low May 7

- SUP 3: 5455.50 Low Apr 30

- SUP 4: 5355.25 Low Apr 24

A bullish trend condition in S&P E-Minis remains intact and the latest pullback is considered corrective. Last Friday’s sell-off resulted in a print below the 20-day EMA, at 5779.53. A key support lies at 5719.58, the 50-day EMA. A clear break of this average is required to highlight a stronger reversal and signal scope for a deeper retracement. Sights are on the bull trigger at 5993.50, the May 20 high.

COMMODITIES: Gold, Copper Pull Back, Crude Loses Ground

- Spot gold has fallen by 1.3% to $3,300/oz on Tuesday, amid a firmer dollar and rally in long-end core yields.

- Despite an improvement in US-EU trade relations, policy uncertainty remains high. Alongside continued US fiscal concerns, the case for holding gold remains. TD Securities notes that CTAs will buy gold in any scenario over the coming week.

- From a technical perspective, the recovery in gold from the May 15 low has signalled an end to the corrective phase that started on April 22.

- Medium-term trend signals are unchanged and remain bullish, and a move higher would open $3,435.6 next, the May 7 high. Key support and the bear trigger has been defined at $3,121.0, the May 15 low.

- Elsewhere, copper has also pulled back by 2.0% today to $474/lb, amid signs of weaker Chinese demand as orders for electrical wires have slowed in May.

- A bearish threat for copper remains and a breach of $447.75, the May 9 low, would confirm a resumption of the bear leg, exposing $436.00, the Apr 10 low. On the upside, resistance to watch is $498.25, the Apr 23 high.

- Meanwhile, WTI lost ground today amid reports that OPEC is likely to commit to another larger than planned hike in output from July at its May 31 meeting.

- WTI Jul 25 is down by 1.2% at $60.8/bbl.

- A continuation lower would refocus attention on $54.33, the Apr 9 low and bear trigger. On the upside, key resistance to watch is $62.63, the 50-day EMA.

DATA/EVENTS CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 28/05/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 28/05/2025 | 0130/1130 | *** | CPI Inflation Monthly | |

| 28/05/2025 | 0130/1130 | *** | Quarterly construction work done | |

| 28/05/2025 | 0200/1400 | *** | RBNZ official cash rate decision | |

| 28/05/2025 | 0600/0800 | ** | Retail Sales | |

| 28/05/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 28/05/2025 | 0645/0845 | ** | PPI | |

| 28/05/2025 | 0645/0845 | *** | GDP (f) | |

| 28/05/2025 | 0645/0845 | ** | Consumer Spending | |

| 28/05/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 28/05/2025 | 0755/0955 | ** | Unemployment | |

| 28/05/2025 | 0800/0400 | Minneapolis Fed's Neel Kahkari | ||

| 28/05/2025 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 28/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 28/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 28/05/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 28/05/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 28/05/2025 | 1500/1600 | BOE's Pill on monetary policy panel at Austria National Bank / SUERF | ||

| 28/05/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 28/05/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 28/05/2025 | 1800/1400 | FOMC Minutes | ||

| 28/05/2025 | 1800/1400 | *** | FOMC Minutes | |

| 28/05/2025 | 0000/2000 | New York Fed's John Williams | ||

| 29/05/2025 | 0130/1130 | * | Private New Capex and Expected Expenditure |