MNI ASIA MARKETS ANALYSIS: Ebb & Flow of War Negotiations

HIGHLIGHTS

- Treasuries look to finish mixed Thursday, near the middle of the day's range, cures twist steeper as midday support in bonds evaporated.

- Sentiment ebb & flow: improved after headlines reported ceasefire negotiations had at least opened up between Israel and Lebanon - sentiment tempered after Israel's Netanyahu said "we wont stop until Northern Israel is secure" .. followed by: "there is no ceasefire in Lebanon."

- WTI crude remains higher on the day, although it has pared some of its earlier gains amid comments from President Trump that Israel will scale back operations in Lebanon - key threat to the ongoing fragile ceasefire.

- OIS-implied Eurozone rates dipped after MNI published a piece citing ECB sources that pointed to reduced urgency for a rate hike in April given the ceasefire (see MNI SOURCES: Ceasefire Reduces Urgency Of ECB Hike Talk).

US TSYS

MNI US TSYS: War Headlines Keep Markets on Edge

- Treasuries look to finish mixed, near middle of Thursday's range, curves twist steeper with midday support in bonds evaporating as middle east war headlines kept markets on edge. Sentiment improving after headlines reported ceasefire negotiations had at least opened up between Israel and Lebanon.

- The situation remains fluid and veracity of reports in question at times:

- Earlier, senior Iranian figures had claimed a ceasefire in Lebanon formed part of the deal with the US, and that if Israel's assault did not halt the US-Iran deal would be deemed moot and talks in Islamabad on Friday will not take place.

- On cue, sentiment tempered after Israel's Netanyahu said "we wont stop until Northern Israel is secure" .. followed by: "there is no ceasefire in Lebanon."

- TYM6 trades steady at 111-07.5 (111-00.5 low / 111-15.5 high). Attention on important resistance at 111-21, the 50-day EMA. A clear break of this average is required to signal scope for a stronger recovery. This would open 111-31, a Fibonacci retracement. Moving average studies are in a bear-mode position, highlighting a dominant downtrend. First key support to watch is 110-16, the Apr 2 low. A break would be bearish.

- On data: Initial jobless claims jumped by more than expected in the week ending April 4, to 219k from 203k prior (rev from 202k) versus the 210k consensus. Real GDP growth was surprisingly revised down a little further in the third Q4 update to just 0.48% annualized (cons 0.7) after a more material trimming to 0.65% in the second update from 1.42% in the advance. Personal income fell by 0.07% M/M, the first contraction since last May and surprising the consensus for 0.3% growth.

- LOOK AHEAD: Friday Data Calendar: CPI, UofM Sentiment, Durables/Cap Goods

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.59% (-0.03), volume: $3.169T

- Broad General Collateral Rate (BGCR): 3.58% (-0.03), volume: $1.314T

- Tri-Party General Collateral Rate (TCR): 3.58% (-0.03), volume: $1.286T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $106B

- Daily Overnight Bank Funding Rate: 3.63% (+0.00), volume: $223B

FED Reverse Repo Operation

RRP usage at $0.402B with 4 counterparties this afternoon vs. $0.177B Wednesday. Compares to last year's highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options trade mixed on net after a pick-up in call spread buying in SOFR earlier while Tsys saw moderate position unwinds. Underlying futures steady to mixed, curves twist steeper late as midday support evaporated in bonds. Projected rate moves largely steady vs. late Wednesday lvls (*): Apr'26 at +.4bp (+.1bp), Jun'26 at -.7bp (+.1bp), Jul'26 at -1.1bp (-.4bp), Sep'26 at -2.3bp (-1.4bp), Oct'26 -3.6bp (-2.9bp).

SOFR Options:

25,000 SFRU6 96.37/96.62 call spds, 5.5 vs. 96.335/0.20%

Block, 5,000 SFRZ6 98.00/99.00 call spds, 2.0 ref 96.415

+5,000 SFRH7 98.00 calls, 5.25

-1,000 SFRH8 95.50/97.50 put over risk reversals, 3.0

+10,000 SFRU6 95.75 puts, , 5.0 vs. 96.335/0.06%

+5,000 0QZ6 97.50/98.50 call spds

-2,500 SFRK6 96.43/96.50 call spds, 0.5 ref 96.32

2,500 SFRJ6 96.31/96.37 put spds ref 96.325

+15,000 SFRU6 96.37/96.62 call spds, 5.25 vs 96.335-.34

2,000 0QK6/0QM6 97.25 call spds ref 96.47

+2,000 0QM6 96.25/96.37/96.87/97.00 call condors, 7.0 vs. 96.495/0.08%

Block, +3,000 0QJ6 96.31/96.37 put spds, 1.0 ref 96.475

-6,500 SFRN6 96.06/96.18 put spds, 2.0 ref 96.33

Treasury Options:

-3,000 TYM6 110.5/111.5 strangles, 119

11,750 USK6/USM6 109 put spds, 16, total volume over 33k

6,400 FVK6 109 calls, 4

10,000 TYK6 110/110.5 put spds, 5 ref 111-03.5

2,000 TYK6 109/110.5 3x1 put spds ref 111-06.5

5,000 TYK6 109.5 puts, 6 ref 111-05.5

5,000 TYM6 107/108/109/110 put condors ref 111-09.5

-5,000 wk2 TY 111.5 calls, 9 vs. 111/13/0.32%

-3,000 TYK6 109.5/111.25 put spds, 25 vs. 111-07.5/0.43%

-1,200 TYM6 111.5 calls, 44

-2,000 TYK6 106.25/116 strangles, 2

+4,000 wk2 TY 110.75/111 put spds, 4

-3,000 TYK6 113.5 calls, 2 ref 111-01/0.05%

-1,650 TYK6 109/110 put spds, 5 vs. 111-11/0.08%

-3,000 wk2 FV 107.75/108.75 strangles, 3

-3,000 wk2 FV 108 calls, 21-20.5 vs. 108-08.75/0.74%

MNI BONDS: EGBs-GILTS CASH CLOSE: Intraday Recovery As Ceasefire Proves Shaky

EGBs and Gilts recovered from sizeable intraday losses to close only moderately weaker Thursday.

- Gilts and EGBs weakened in early trade with oil firmer, as the stability of the 2-week ceasefire in the MidEast war was called into question following Israeli attacks on Lebanon overnight. 10Y yields rose as far as 3.032% in Germany (+8bp on the day), and 4.831% in the UK (+11bp).

- Global FI saw a reprieve (alongside equities) as oil pulled back toward the European cash close, after talks between Israel and Lebanon were announced - thereby removing a key obstacle to ceasefire ahead of the Iran-US/Israel negotiations due to start this weekend.

- The short-end of curves outperformed. OIS-implied Eurozone rates dipped after MNI published a piece citing ECB sources that pointed to reduced urgency for a rate hike in April given the ceasefire (see MNI SOURCES: Ceasefire Reduces Urgency Of ECB Hike Talk).

- The UK and German curves bear steepened, with Gilts slightly outperforming Bunds.

- In a light European data schedule, German February industrial production was weaker than expected, though January's was revised up.

- Friday's agenda includes Italian industrial production and German final March inflation, though most attention will be on the US CPI release.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.8bps at 2.519%, 5-Yr is up 3.5bps at 2.67%, 10-Yr is up 4.4bps at 2.988%, and 30-Yr is up 5.9bps at 3.524%.

- UK: The 2-Yr yield is up 0.9bps at 4.18%, 5-Yr is up 2.8bps at 4.284%, 10-Yr is up 3.8bps at 4.749%, and 30-Yr is up 4.7bps at 5.401%.

- Italian BTP spread down 1.3bps at 74.9bps / French OAT down 1.1bps at 62.6bps

MNI OPTIONS: More Limited Post-Ceasefire Flow, But Again Leans To Upside

Thursday's Europe rates/bond options flow included:

- ERN6 97.75/97.875 call spread paper paid 1.75 on 7K

- ERU6 97.6875/97.8125/97.9375c fly, bought for half in 10k

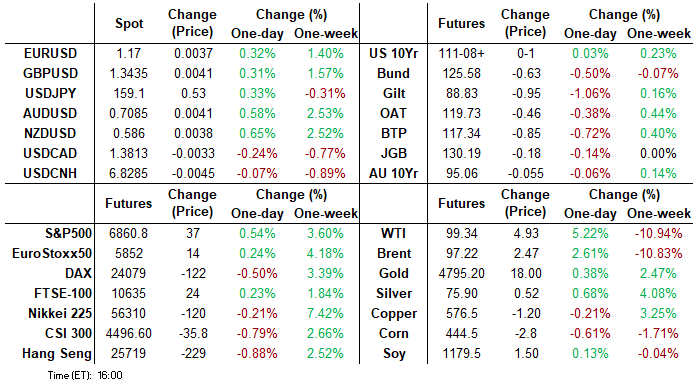

MNI FOREX: Risk Optimism/USD Weakness on Israel/Lebanon Negotiations

- Today’s FX session has been characterised by dollar weakness. Although gradual at first, the moves started to accelerate in late session as Israel PM Netanyahu announced he has instructed his cabinet to open direct negotiations with Lebanon at the earliest possible time.

- The news put the top in crude futures and has assisted a fresh wave of equity strength, with the major benchmarks extending fresh post-ceasefire highs. While the dollar index is exhibiting 0.45% losses on the session, the DXY remains shy of yesterday’s lows, located at 98.53.

- High beta currencies within the G10 are rallying well, with the likes of NOK, AUD and NZD outperforming, while EUR and GBP are posting 0.4% advances against the greenback. Emerging markets continue to be well supported, with USDMXN sinking to 17.35 as the peso extends its impressive rebound. The pair has narrowed the gap back to prior cycle lows around 17.10 substantially.

- Combined with the positive equity senitment, the more contained retracement for fixed income markets reflects the concerns regarding the inflationary shock, all contributing to relative pressure on the Japanese yen on Thursday, which underperforms its G10 peers. EURJPY has rallied 0.6% today, taking the cross back above the 186.00 mark with this week’s climb highlighting a bullish reversal and a recent false break of a bull channel support drawn from the Feb 28 ‘25 low.

- 186.36 is the next level on the topside (the Feb 9 high), before 186.87, the Jan 23 high and a key medium-term resistance. Meanwhile, EURUSD has pressed back above 1.17, with price action strengthening a short-term bullish theme and signalling scope for an extension to 1.1746, a Fibonacci retracement.

- All focus turns to Friday’s release of US CPI. Other scheduled releases include China CPI/PPI, Canada employment and prelim readings of UMich sentiment and inflation expectations.

MNI FX OPTIONS: Expiries for Apr09 NY cut 1000ET (Source DTCC):

- EUR/USD: $1.1700(E786mln), $1.1725(E767mln)

- USD/JPY: Y158.00($1.8bln), Y159.50($781mln), Y160.00($1.1bln)

- GBP/USD: $1.3500(Gbp572mln)

- EUR/GBP: Gbp0.8700(E550mln)

- EUR/JPY: Y178.00(E650mln)

- NZD/USD: $0.5800(N$503mln)

- USD/CNY: Cny6.8000($750mln)

MNI US STOCKS: Late Equities Roundup: At the Whim of Ephemeral Peace Negotiations

- Equities are drifting near late Thursday session highs, sentiment improving after headlines reported ceasefire negotiations had at least opened up between Israel and Lebanon.

- The situation remains fluid and veracity of reports in question at times.

- Earlier, senior Iranian figures had claimed a ceasefire in Lebanon formed part of the deal with the US, and that if Israel's assault did not halt the US-Iran deal would be deemed moot and talks in Islamabad on Friday will not take place.

- On cue, sentiment tempered after Israel's Netanyahu said "we wont stop until Northern Israel is secure" .. followed by: "there is no ceasefire in Lebanon."

- Adding to yesterday's rally: the DJIA +.7%, SPX eminis +.55%, Nasdaq +.6%.

- Utilities/Industrials and Consumer Discretionary sector shares led advances in late trade, Vistra Corp, Constellation Energy, PG&E and Entergy gained 2.5-4.0% while Discretionary was led by Amazon +4.4% after the online retailer announced an additional $12B in Mississippi data center investment.

- Energy sector shares led declines as crude retreated from morning highs: Marathon Petroleum Corp, Phillips 66, Valero Energy, EOG Resources and Occidental Petroleum Corp trade -2.5-4.0%.

MNI EQUITY TECHS: E-MINI S&P: (M6) Retracement Mode

- RES 4: 7035.00 High Feb 25

- RES 3: 6963.00 High Mar 2

- RES 2: 6921.09 76.4% retracement of the Jan 28 - Mar 31 bear leg

- RES 1: 6873.25 High Mar 11

- PRICE: 6853.00 @ 14:45 ET Apr 9

- SUP 1: 6667.15 20-day EMA

- SUP 2: 6567.00/6503.75 Low Apr 6 and key S/T support / Low Apr 2

- SUP 3: 6353.25 Low Mar 31 and key support

- SUP 4: 6316.61 3.236 proj of the Feb 11 - 17 - 25 price swing

A strong rally in S&P E-Minis on Wednesday highlights an extension of the reversal that started Mar 31. Note that trend signals remain bearish and for now, gains are considered corrective. A continuation higher would open 6921.09 next, a Fibonacci retracement point. Key medium-term resistance and the bull trigger is far off at 7096.50, the Jan 28 high. Initial firm support to watch lies at 6567.00, the Apr 6 low.

MNI COMMODITIES: Crude Rises, Precious Metals Extend Gains

- WTI remains higher on the day, although it has pared some of its earlier gains amid comments from President Trump that Israel will scale back operations in Lebanon. This has been a key threat to the ongoing fragile ceasefire.

- WTI May 26 is up by 3.7% at $97.9/bbl.

- Direct negotiations between Israel and Lebanon will begin next week in Washington while Lebanon pushes for a temporary ceasefire, according to Axios.

- However, Netanyahu later said there is currently no ceasefire in Lebanon and that Israel will not stop until Northern Israel is secure.

- For now, the Strait of Hormuz remains largely blocked with limited ships observed leaving the region.

- The sharp pullback in WTI futures is for now, considered corrective. The contract has traded through the 20-day EMA, exposing a key support around the 50-day EMA, at $85.85.

- Elsewhere, precious metals have extended gains, as the US dollar has continued to trade on the backfoot amid the ceasefire optimism.

- Spot gold is up by 1.2% at $4,773/oz, while silver has rallied by 2.2% to $75.7/oz.

- Recent gains in gold still appear to be corrective, although for now the short-term bull cycle remains intact. Price has pierced the 50-day EMA, signalling scope for an extension towards $4,914.9, a Fibonacci retracement point.

- Meanwhile, a bear cycle in silver remains intact and recent gains appear corrective. However, a clear break of initial resistance at $77.385, the 50-day EMA, would signal scope for a stronger retracement.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 10/04/2026 | 0600/0800 | ** | Private Sector Production m/m | |

| 10/04/2026 | 0600/0800 | *** | CPI Norway | |

| 10/04/2026 | 0600/0800 | *** | Germany CPI (f) | |

| 10/04/2026 | 0600/0800 | *** | Germany CPI (f) | |

| 10/04/2026 | 0800/1000 | * | Industrial Production | |

| 10/04/2026 | 1000/1200 | ECB de Guindos Remarks at Development Event | ||

| 10/04/2026 | - | *** | New Loans | |

| 10/04/2026 | - | *** | Money Supply | |

| 10/04/2026 | - | *** | Social Financing | |

| 10/04/2026 | 1200/0800 | ** | Brazil Final CPI | |

| 10/04/2026 | 1230/0830 | *** | CPI | |

| 10/04/2026 | 1230/0830 | *** | CPI | |

| 10/04/2026 | 1230/0830 | *** | CPI | |

| 10/04/2026 | 1230/0830 | *** | CPI | |

| 10/04/2026 | 1230/0830 | *** | Labour Force Survey | |

| 10/04/2026 | 1230/0830 | *** | Labour Force Survey | |

| 10/04/2026 | 1400/1000 | *** | UMich Surveys of Consumers | |

| 10/04/2026 | 1400/1000 | *** | UMich Surveys of Consumers | |

| 10/04/2026 | 1400/1000 | ** | Factory New Orders | |

| 10/04/2026 | 1400/1000 | ** | Factory New Orders | |

| 10/04/2026 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/04/2026 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/04/2026 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/04/2026 | 1800/1400 | ** | Treasury Budget |