US STOCKS: Late Equities Roundup: At the Whim of Ephemeral Peace Negotiations

Apr-09 18:09

- Equities are drifting near late Thursday session highs, sentiment improving after headlines reported ceasefire negotiations had at least opened up between Israel and Lebanon.

- The situation remains fluid and veracity of reports in question at times.

- Earlier, senior Iranian figures had claimed a ceasefire in Lebanon formed part of the deal with the US, and that if Israel's assault did not halt the US-Iran deal would be deemed moot and talks in Islamabad on Friday will not take place.

- On cue, sentiment tempered after Israel's Netanyahu said "we wont stop until Northern Israel is secure" .. followed by: "there is no ceasefire in Lebanon."

- Adding to yesterday's rally: the DJIA +.7%, SPX eminis +.55%, Nasdaq +.6%.

- Utilities/Industrials and Consumer Discretionary sector shares led advances in late trade, Vistra Corp, Constellation Energy, PG&E and Entergy gained 2.5-4.0% while Discretionary was led by Amazon +4.4% after the online retailer announced an additional $12B in Mississippi data center investment.

- Energy sector shares led declines as crude retreated from morning highs: Marathon Petroleum Corp, Phillips 66, Valero Energy, EOG Resources and Occidental Petroleum Corp trade -2.5-4.0%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

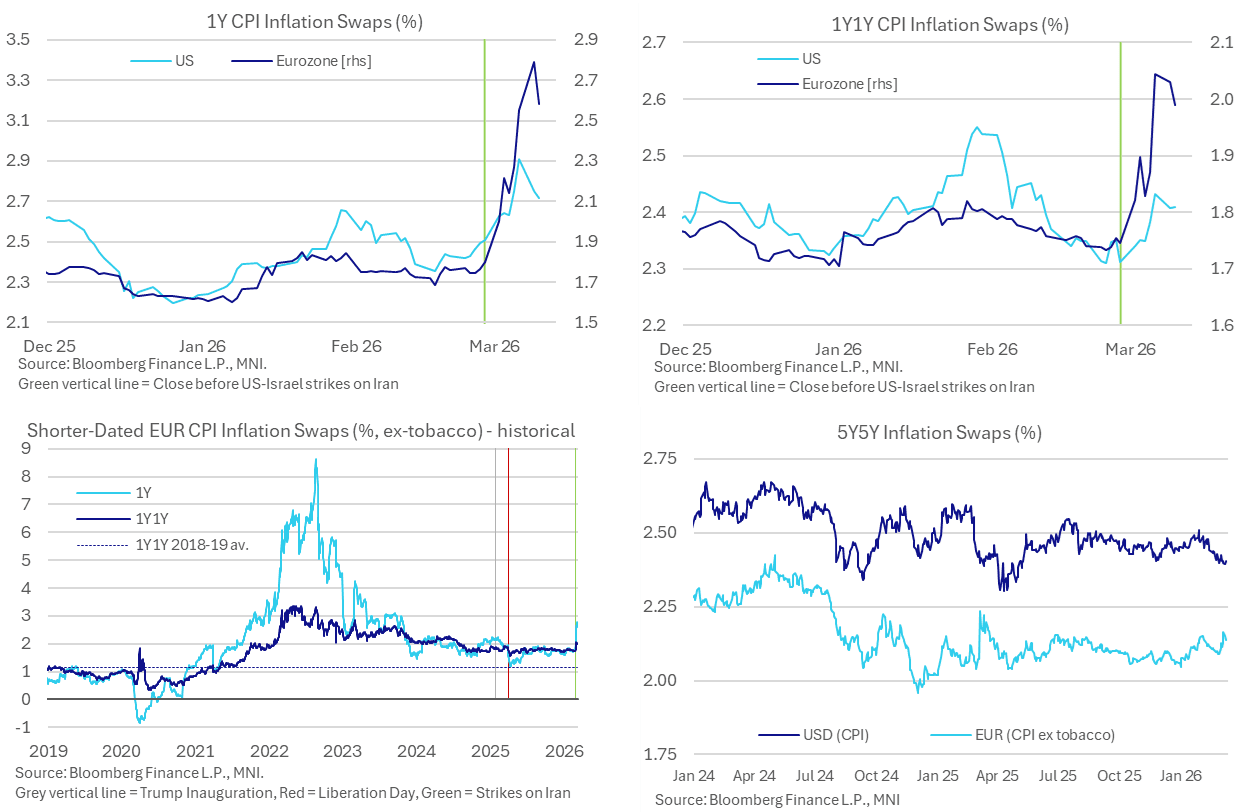

INFLATION: Cooling In Inflation Expectations But EU Near-Term Still Elevated

Mar-10 18:02

- With the huge pullback off yesterday’s early highs for oil and gas prices, market-based inflation expectations have eased, still elevated by recent month standards for the EU but much less so the US.

- Taking stock of cumulative changes since the initial US-Israel strikes on Iran:

- US 1Y +21bp, 1Y1Y +10bp

- EU 1Y +78bp, 1Y1Y +24bp

- EU 5Y5Y inflation expectations at 2.14% are +5bp since Feb 28 but more broadly contained by ranges over the past year.

FOREX: Lower Oil Weighs on USD, Plethora of Factors Significantly Boost AUD

Mar-10 18:01

- The US Dollar has traded on the back foot on Tuesday, reflective of the extension on energy price weakness, albeit in a more contained manner. The USD index sits around half a percent lower, having extended the pullback from Monday’s peak to around 1%. Late headlines surrounding tankers operating in the Strait of Hormuz provided some further greenback pressure, however, the deletion of a social media post from the US Energy Secretary has stalled the downside momentum.

- With crude futures remaining towards the lower end of the most recent range and major equity benchmarks continuing to trade in a resilient manner, the Australian dollar continues to outperform on Tuesday. As a reminder, the initial Aussie boost was provided by a hawkish leaning RBA Hauser and combining this with a softer dollar backdrop, AUDUSD has extended intraday gains to around 1%.

- Fresh cycle highs at 0.7168 have pierced the key resistance point at the 2023 highs. 0.7208 represents the next notable target, the 61.8% of the Feb 25 ‘21 - Apr 9 ‘25 bear leg, while above here, 0.7283 is the June 2022 high.

- Separately, the much stronger than expected Chinese trade data in January/February have supported renewed optimism for the Chinese Yuan, helping to bolster renewed optimism for the emerging market FX basket, with Latin American currencies and the Hungarian Forint particular beneficiaries.

- Elsewhere in the majors, USDJPY has traded in a very contained range, having slipped back below the prior ‘rate check’ zone above 158.00. While the primary driver for the greenback will be the Iranian developments and impact on energy prices, US CPI headlines the week’s data calendar tomorrow.

EURUSD TECHS: Gains Considered Corrective

Mar-10 18:00

- RES 4: 1.1835 High Feb 23

- RES 3: 1.1748 50-day EMA

- RES 2: 1.1730 20-day EMA

- RES 1: 1.1664 High Mar 10

- PRICE: 1.1645 @ 16:18 GMT Mar 10

- SUP 1: 1.1507 Mar 09

- SUP 2: 1.1491 Low Nov 21 ‘25

- SUP 3: 1.1456 1.50 proj of the Jan 27 - Feb 6 - 10 price swing

- SUP 4: 1.1392 Low Aug 1 ‘25

Short-term gains in EURUSD are - for now - considered corrective. A bear cycle remains in play and Monday’s fresh cycle low reinforces current conditions. Price has breached 1.1573, the Jan 19 low and a key support. The clear break of it opens 1.1491, the Nov 21 ‘25 low. Note that moving average studies highlight a bearish cross - if confirmed this would signal a medium-term bearish development. First resistance is 1.1655, the Mar 4 high.

Trending Top

May-22 16:54