MNI ASIA MARKETS ANALYSIS: Dollar Sags As Fed Cut Bets Build

MNI (NEW YORK) -

HIGHLIGHTS:

- Dollar softens, stocks rise and cash Treasuries have best session since Aug 1 as September Fed rate cut gets fully priced in

- Crude oil prices resume decline ahead of Friday's Trump-Putin meeting

- Upcoming focus on Australia employment data, UK GDP, and the Norges Bank decision (MNI preview below)

US TSYS: Belly Outperforms As September Fed Cut Gets Fully Priced

The belly outperformed on the Treasury curve Wednesday as Fed easing prospects incrementally increased.

- The space early was buoyed in early New York trade after Treasury Secretary Bessent said the Fed should consider a 50bp cut next month, and 150-175bp of easing overall.

- Later in the session, the front end of the futures strip reacted favorably to commentary by FOMC's Bostic (view of only one 2025 cut predicated on labor market remaining solid ) Goolsbee (September meeting will be "live").

- This saw a September cut become more than fully priced, with the futures-implied Fed funds rate for that meeting (4.07%) at the lowest since the first days of July.

- Also helping was a modest pullback in implied breakeven inflation, as oil prices remained under pressure ahead of the Trump/Putin talks on Friday.

- Against this backdrop, yields across the curve dropped the most since Aug 1. 5s30s neared the steepest close since October 2021 (which was set Friday at 106.32bp).

- Thursday's data includes weekly jobless claims and PPI, eyed for both price pressures in their own right and helping hone July PCE estimates (after the CPI data, MNI's survey of estimates points to 0.25% M/M for core PCE). Fed speakers include Musalem and Barkin.

- Latest levels: the 2-Yr yield is down 5.2bps at 3.6786%, 5-Yr is down 5.8bps at 3.765%, 10-Yr is down 5.2bps at 4.2365%, and 30-Yr is down 5.1bps at 4.8273%. Sep 10-Yr futures (TY) up 11.5/32 at 112-5.5 (L: 111-23 / H: 112-09)

STIR: Sept Implied Fed Rates At 6-Week Lows After Bostic, Goolsbee Comments

Fed funds futures-implied cuts for September's meeting extend through 26bp, up 2+bp on the day and 1bp since commentary this afternoon by Atlanta Fed's Bostic and 2025 FOMC voter, Chicago's Goolsbee. The 4.07% implied funds rate is the lowest for the September meeting since the solid June payrolls data release on July 3.

- This dovish intraday shift is a little counter-intuitive: Bostic, who doesn't vote in 2025 or 2026, sounded the more dovish of the two, acknowledging that continued evidence of weakness in the labor market could put at risk his current view that only one cut by year-end would be appropriate; =

- Goolsbee, who actually votes in September, said that fall Fed meetings would be "live" but didn't sound all that enthusiastic about easing soon, fretting over the services inflation pickup in July's CPI report report, and seeing job growth weakness as potentially the result of a drop in population growth.

- The shift in September pricing accounts for the bulk of the shift in implied pricing through the next several meetings: Oct and Dec see 3.5bp more implied cuts (43bp and 64bp respectively) on the day, with an additional 4bp through March (5 meetings from now).

| Meeting | Current FF Implieds (%), LH | Cumulative Change From Current Rate (bp) | Incremental Chg (bp) | Yesterday (Aug 12) | Chg Since Then (bp) |

| Sep 17 2025 | 4.07 | -26.5 | -26.5 | 4.09 | -2.3 |

| Oct 29 2025 | 3.90 | -43.2 | -16.7 | 3.93 | -3.5 |

| Dec 10 2025 | 3.69 | -63.8 | -20.6 | 3.73 | -3.5 |

| Jan 28 2026 | 3.58 | -75.2 | -11.4 | 3.61 | -3.5 |

| Mar 18 2026 | 3.45 | -88.4 | -13.2 | 3.49 | -3.9 |

NORGES BANK: MNI Norges Bank Preview - Aug '25: Slow and Steady

- Norges Bank is unanimously expected to keep the policy rate on hold at 4.25% on Thursday, while continuing to guide towards further cuts in H2.

- After surprising markets with a 25bp cut in June, macroeconomic data has broadly confirmed Norges Bank’s outlook. With the June MPR rate path consistent with “one or two” more cuts in H2 and implied probabilities tilted in favour of easing at the September and December MPR meetings, there appear few reasons to go against market consensus in August.

- We expect the primary guidance language from June to be maintained in the policy statement. With a rate hold fully priced and unanimously expected, a significant market reaction would require material deviations from the existing guidance language.

- Quarterly cuts in September and December remains the base case amongst analysts.

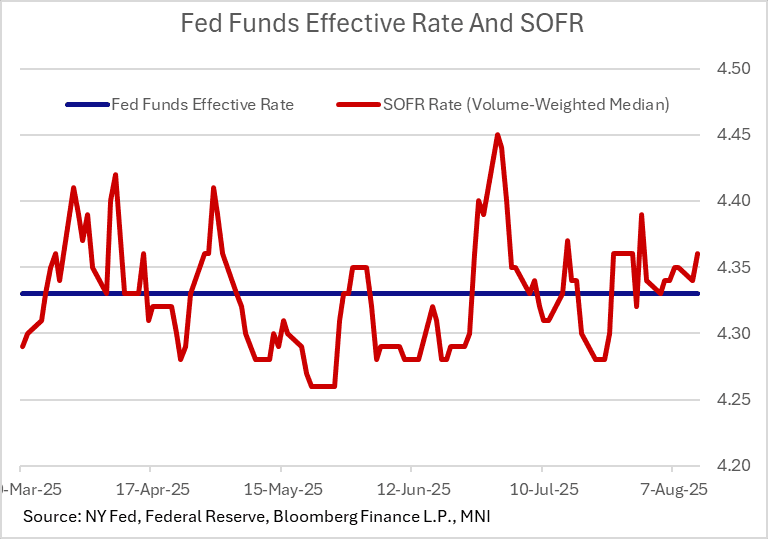

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

US TSYS/OVERNIGHT REPO: Secured Rates Ticked Up Tuesday, May Subside Wednesday

Secured rates ticked up Tuesday as largely expected, primarily on account of Treasury bill settlements ($55B in net cash today). SOFR rose 2bp to 4.36%, with BGCR and TGCR up 1bp apiece. Upside pressure is due to relent today, but could subsequently pick up with $42B in bill settlements on Thursday, followed by $35B in coupon settlements Friday.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.36%, 0.02%, $2804B

* Broad General Collateral Rate (BGCR): 4.34%, 0.01%, $1175B

* Tri-Party General Collateral Rate (TGCR): 4.34%, 0.01%, $1144B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.33%, no change, volume: $114B

* Daily Overnight Bank Funding Rate: 4.33%, no change, volume: $247B

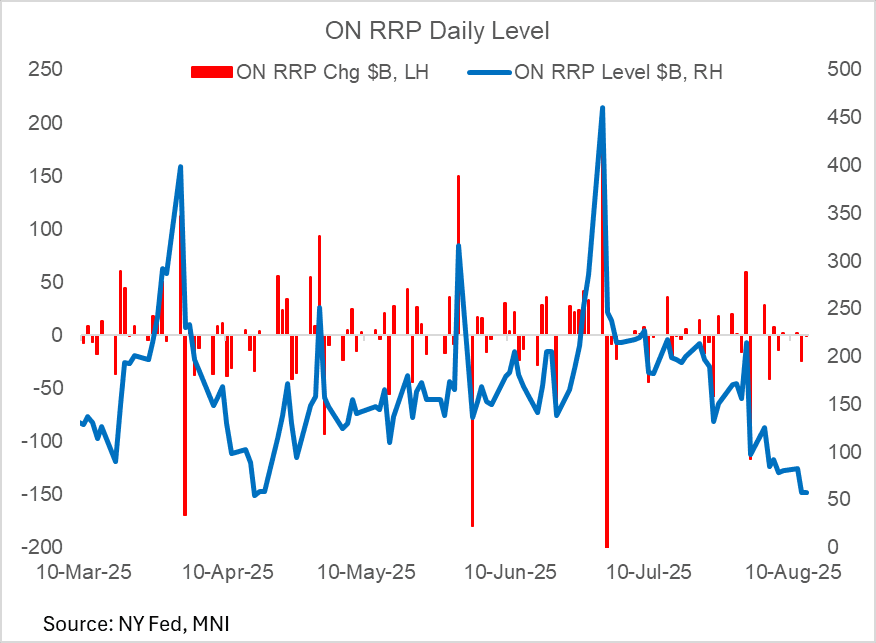

US TSYS/OVERNIGHT REPO: ON RRP Takeup Remains Well Below $100B

Overnight Reverse Repo facility takeup at the New York Fed was basically unchanged Wednesday vs the prior session, at $57.2B (vs $57.5B).

- This marked a fresh 4-month low (Apr 16's tax date saw $54.8B takeup) but it's now the 8th session in the past 9 below $100B, for the first time since February.

OPTIONS: US Options Roundup - Aug 13 2025

Wednesday's US rates/bond options flow included:

- SFRU5 96.00/96.12/96.25c fly, trades again for 1, bought for 0.75 and 1 in 15k Total

- SFRU5 95.81/95.75/95.68p fly, traded half in 3k.

- SFRU5 95.93/96.00/96.12c fly 2x3x1, traded 2.25 in 2.5k.

- SFRU5 96.00/95.75ps, traded 8 in 5k.

- SFRU5 96.00p, traded 8.5 in 5k.

- SFRU5 96.06/96.12cs traded 1 in 8k total.

- SFRU5 96.12/96.25cs, traded 1.5 in 13k.

- SFRU5 95.8125 puts bought for 1.75 in 5k (block)

- SFRV5 96.37/96.50cs, traded 3 in 2k.

- SFRZ5 95.75/95.68cs, traded 0.25 in 12k.

- SFRZ5 96.37/96.50cs vs 2QZ5 96.93/97.06cs, bought the front for -0.25 in 2.5k. This was bought Yesterday for -0.5 in 2.5k.

- SFRH6 96.25p, traded 10.5 in 2k.

- FVU5 109/108.5 put spread sold at 10.5 in 7.5k (block) - (cov 109-00, 34%)

- TYU5 113 calls bought for 6 in 15.5k (block) - (vs 112-03+, 5%)

BONDS: EGBs-GILTS CASH CLOSE: Bull Flattening Fades Prior Session's Weakness

European yields reversed some of Tuesday's sell-off in a bull flattening move Wednesday.

- In addition to fading the prior session's somewhat unusual sell-off that didn't seem driven by headline/macro developments, Wednesday saw yields pull back in tandem with a retreat in oil prices in anticipation of peace developments on the Russia-Ukraine front.

- Also helping buoy global instruments was US Treasury Secretary Bessent opining that the Federal Reserve should consider cutting rates by 50 basis points in September, and 150-175 overall.

- Data was limited in impact, with German and Spanish final July HICP confirming flash estimates.

- Gilts lagged the Bund rally, with the UK Guardian reporting on potential inheritance tax adjustments in the Autumn Budget.

- Periphery/semi-core EGBs had a constructive session led by BTPs, in a broader risk-on move (10Y BTP/Bund approaches the 2010 low of 75.4bp).

- Thursday's agenda includes UK monthly economic activity / Q2 GDP data, with Eurozone industrial production, GDP, and Employment data also featuring.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 3.3bps at 1.934%, 5-Yr is down 6.1bps at 2.257%, 10-Yr is down 6.4bps at 2.68%, and 30-Yr is down 7.1bps at 3.228%.

- UK: The 2-Yr yield is down 2.2bps at 3.863%, 5-Yr is down 3.1bps at 4.009%, 10-Yr is down 3.7bps at 4.589%, and 30-Yr is down 3.9bps at 5.428%.

- Italian BTP spread down 1.7bps at 77.1bps / French OAT down 1.2bps at 65.6bps

FOREX: USD Index Slips Again; Bessent Argues Fed Rate Should be 150bps Lower

- The greenback again traded weaker, making for a second session of losses for the USD Index. Key support into the early August low at 97.945 has given way, opening 97.109 in the short-term ahead of the bear trigger at 96.377. USD weakness came alongside further reports around the leadership and make-up of the Fed into next year. Treasury Secretary Bessent spoke on the interview process, and stated that if the Fed had effective leadership the key rate would be as much as 175bps lower now than it would have been otherwise - further affirming the administration's preference for a low-rates Fed chair once Powell departs next year.

- The list of candidates grew further according to reports, with a number of private sector economists added to the list of those considered, on top of the well known names of Hassett, Warsh, Waller and Bowman.

- GBP rallied further, extending the recent spell of strength and further building on the gains posted after the break of the 50-day EMA on the August BoE rate decision. This firms the speed of the recovery off the 1.3142 pullback low and signals a greater probability of a bullish reversal. For now, S/T momentum is still pointed higher, with the Jul 24 high of 1.3589 the next notable upside level.

- Meanwhile, speculation around the Trump-Putin meeting in Alaska at the end of the week continues to build. Following a call with European leaders today, it was disclosed that Trump is set to pursue an immediate ceasefire in the conflict - at which point more sincere negotiations and talks can begin over a conclusion to the war. Territory remains the key issue, with Kyiv ruling out the handing over of eastern territories, and Putin requiring some concessions as a result of his multi-year special operation. Oil and risk markets remain sensitive to the issue, with Trump warning of "very severe consequences" if no interim agreement is reached on Friday.

- Australia jobs data is the highlight Thursday. With May and June employment gains disappointing, the July data will be monitored closely for signs that the labour market has turned. Q2 employment averaged 28.8k/month up from Q1's 1.4k but slightly lower than Q2 2024's 32.2k. Consensus expects a 25k gain in July after June's +2k, slightly below the Q2 average. The unemployment rate is forecast to decline 0.1pp to 4.2%, returning to the Q2 average.

FX OPTIONS: Expiries for Aug14 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E2.8bln), $1.1590-00(E1.8bln), $1.1625-35(E829mln), $1.1645-50(E1.3bln), $1.1660-65(E943mln), $1.1695-02(E4.9bln), $1.1710-15(E1.2bln), $1.1750(E774mln)

- USD/JPY: Y145.00($924mln), Y146.00($616mln), Y146.65-85($1.0bln), Y147.00-20($1.3bln), Y148.15-30($1.2bln), Y149.00($1.2bln)

- GBP/USD: $1.2975-00(Gbp1.2bln)

- EUR/GBP: Gbp0.8690-05(E1.1bln)

- AUD/USD: $0.6575(A$516mln), $0.6600(A$1.3bln)

- NZD/USD: $0.6000-11(N$636mln)

- USD/CAD: C$1.3860-70($768mln)

EQUITIES: Rate-Sensitive Sectors Buoyed By Fed Cut Expectations

Equity indices edged up Wednesday, helped by increasing expectations of the Federal Reserve resuming its easing cycle in September. The S&P 500 and Nasdaq saw fresh record high closes albeit off mid-morning session intraday highs.

- Unlike Tuesday, sectoral performances were a little more mixed though most were in the green. Within the S&P, materials (+1.7%) and health care (+1.6%) led gains, with consumer staples (-0.4%) and communication services (-0.5%) lagging.

- Homebuilders and other rate-sensitive sectors showed notable strength, as rate futures pricing showed a September 25bp Fed cut now fully discounted: the Dow outperformed the S&P and Nasdaq on strong performances by Home Depot (+2.9%) and Sherwin-Williams (+3.1%).

- Latest futures levels: Dow Jones mini up 483 pts or +1.08% at 45040, S&P 500 mini up 20 pts or +0.31% at 6488.5, NASDAQ mini down 5.5 pts or -0.02% at 23933.5.EQUITIES

COMMODITIES: Crude Falls Amid Ceasefire Push, Gold Ticks Up, Silver Recovers

- Crude has declined following reports that Trump will push for a ceasefire in Friday’s meeting with Putin, adding to pressure from the IEA’s lower 2025 oil demand growth forecast.

- WTI Sep 25 is down by 0.9% at $62.6/bbl.

- The IEA has revised down its 2025 global oil demand growth forecasts for both 2025 and 2026, according to the August Oil Market Report. Growth this year is the weakest since 2019.

- With today’s move, WTI futures have pierced initial support at $62.77, a clear break of which would expose $58.17, the May 30 low.

- Meanwhile, gold is off the weekly low, with the yellow metal ticking up by 0.1% to $3,352/oz today. However, the bounce appears shallow at these levels, keeping price within the mid-point of the recent range.

- The phase of weakness into the end of July supported the view that short-term pullbacks are corrective - for now - and the bull cycle that started Jun 30 remains intact. Key near-term resistance is at $3,439.0, the Jul 23 high.

- However, the yellow metal has traded through support at $3,334.6, the 50-day EMA, signalling scope for a deeper retracement and exposing the next key support at $3,248.7, the Jun 30 low.

- Elsewhere, silver has outperformed today, rising by 1.5% to $38.5/oz.

- Trend signals in silver remain bullish, with sights on $39.655 a Fibonacci projection.

DATA/EVENTS CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 14/08/2025 | 0130/1130 | *** | Labor Force Survey | |

| 14/08/2025 | 0600/0700 | *** | UK Monthly GDP | |

| 14/08/2025 | 0600/0800 | *** | Final Inflation Report | |

| 14/08/2025 | 0600/0700 | ** | Trade Balance | |

| 14/08/2025 | 0600/0700 | ** | Index of Services | |

| 14/08/2025 | 0600/0700 | ** | Index of Production | |

| 14/08/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 14/08/2025 | 0600/0700 | *** | GDP First Estimate | |

| 14/08/2025 | 0600/0800 | *** | Final Inflation Report | |

| 14/08/2025 | 0645/0845 | *** | HICP (f) | |

| 14/08/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 14/08/2025 | 0900/1100 | ** | Industrial Production | |

| 14/08/2025 | 0900/1100 | *** | GDP (p) | |

| 14/08/2025 | 0900/1100 | * | Employment | |

| 14/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 14/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 14/08/2025 | 1230/0830 | *** | PPI | |

| 14/08/2025 | 1230/0830 | *** | PPI | |

| 14/08/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 14/08/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 14/08/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 14/08/2025 | 1800/1400 | Richmond Fed's Tom Barkin | ||

| 15/08/2025 | 2350/0850 | *** | GDP | |

| 15/08/2025 | 0200/1000 | *** | Fixed-Asset Investment | |

| 15/08/2025 | 0200/1000 | *** | Retail Sales | |

| 15/08/2025 | 0200/1000 | *** | Industrial Output | |

| 15/08/2025 | 0200/1000 | ** | Surveyed Unemployment Rate M/M |