MNI ASIA MARKETS ANALYSIS: DJIA Record High While Gold Tumbles

HIGHLIGHTS

- Early risk-off (Tsys extended highs, equities sold off) after Pres Trump posted retribution on Hamas if they continue "to act badly, in violation of their agreement with us."

- Second half risk-off coincided with Pres Trump expecting "$20T in US until year end", while Trump anticipates having "a good deal with Xi" the meeting in S Korea at end of the month may NOT happen.

- Despite the bouts of risk-off, the DJIA managed to mark a new record high of 47,125.66 in the first half.

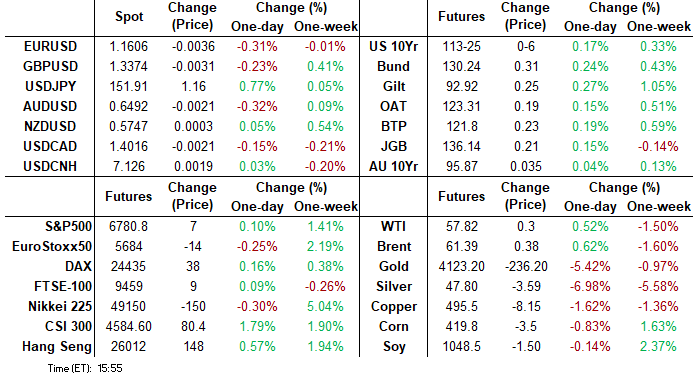

- Precious metals sold off sharply on Tuesday, with spot gold currently down by 5.6% at $4,113/oz and silver down by 7.7% at $48.4/oz, albeit off session lows.

US TSYS

MNI US TSYS: Tsys Hold Near Highs, New Record High for DJIA, Gold Record Decline

- Treasuries holding narrow, higher range since gaining early Tuesday - apparently sensitive to a couple social media posts by Pres Trump while stocks dipped too after he posted retribution on Hamas if they continue "to act badly, in violation of their agreement with us."

- Second half risk-off coincided with Pres Trump expecting "$20T in US until year end", while Trump anticipates having "a good deal with Xi" the meeting in S Korea at end of the month may NOT happen.

- Currently, the Dec'25 10Y contract trades +5.5 at 113-24.5 vs 113-27.5 high. Moving average studies are in a bull-mode position and this set-up continues to highlight a dominant uptrend. Sights are on 114-10, the Apr 7 high (cont) and the next key resistance. Firm support lies at 113-01+, the 20-day EMA.

- Projected rate cut pricing steady to mildly mixed vs. late Monday levels (*): Oct'25 at -24.2bp (-24.7bp), Dec'25 at -49.2bp (-50bp), Jan'26 at -64.2bp (-63.7bp), Mar'26 at -78.2bp (-77bp).

- Stocks remain mixed late Tuesday, the DJIA outperforming after managing to mark a new record high of 47,125.66 in the first half. Reporting earnings after the close: Netflix, Capital One Financial, Mattel, Western Alliance Bancorp (in the hot seat last week after announcing bad loan losses), Omnicom, EQY and Texas Instruments.

- Precious metals sold off sharply on Tuesday, with spot gold currently down by 5.6% at $4,113/oz and silver down by 7.7% at $48.4/oz, albeit off session lows. Platinum and palladium have also fallen by 5-6%.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.16% (-0.02), volume: $2.945T

- Broad General Collateral Rate (BGCR): 4.12% (-0.04), volume: $1.164T

- Tri-Party General Collateral Rate (TCR): 4.12% (-0.04), volume: $1.135T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.11% (+0.00), volume: $82B

- Daily Overnight Bank Funding Rate: 4.11% (+0.00), volume: $163B

FED Reverse Repo Operation

RRP usage recedes to $4.699B with 10 counterparties this afternoon from $5.931B Monday. Compares to $3,516B on Tuesday, Oct 13 (lowest level since early April 2021) & this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR/Treasury options trade mixed on modest volumes Tuesday as the US Gov enters shutdown day 20. Underlying futures modestly higher (TYZ5 113-23.5 +4.5) while US$ firmer. Projected rate cut pricing steady to mildly mixed vs. late Monday levels (*): Oct'25 at -24.2bp (-24.7bp), Dec'25 at -49.2bp (-50bp), Jan'26 at -64.2bp (-63.7bp), Mar'26 at -78.2bp (-77bp).

SOFR Options:

-5,000 SFRZ5 96.25/96.37/96.50/96.62 call condors, 7.25 vs. 96.37/0.10%

-3,000 SFRH6 96.50 straddles, 31.75 vs. 96.65/0.32%

-2,000 SFRZ5 96.25/96.50/96.75 call flys. 9.5 ref 96.38

+5,000 3QM6 96.00/97.50 put over risk reversals, 1.5

-2,500 2QM6 96.37/97.37 call over risk reversals, 0.5 vs. 96.875/0.45%

+1,000 2QH6 96.93 straddles, 44.0 vs. 96.875/0.04%

+5,000 SFRX5 96.12/96.25 2x1 put spds 0.5 ref 96.375

13,000 SFRX5 96.75/96.87 call spds, cab

-3,000 SFRZ5 96.50/96.62 call spds, 1.25

Treasury Options:

Block: 6,750 USZ5/USF6 123 call spds, 25 vs. 473 TYZ5 at 119-11

8,000 USZ5/USF6 111 put spds, 8

Block, 11,640 USZ5 110/USF6 111 put diagonal/calendar spread, 10 net

3,525 TYZ5 114/114.5 call spds vs. 113/113.5 put spds ref 113-24

5,000 TYZ5 114/116 call spds call spds 28 ref 113-26

2,000 TYZ5 113/114 put spds, 29 ref 113-24.5

2,000 TYZ5 114/115.5 2x3 call spds ref 113-26

3,000 TYZ5 114 calls, 39 ref 113-25

1,500 TYX5 112.75/113.5/114.5 broken call flys

2,500 TYG6 111/116 3x1 put over risk reverals (putx3)

3,000 TYF6 116/117.5 call spds vs. 2,000 TYF6 114.5 calls ref 113-16.5

-1,500 TYZ5 113.5 calls, 43 vs. 113-16.5/0.52%

1,800 TYF 111.5/115.5 strangles ref 113-16.5

+4,300 TYZ5 115.5 calls, 14 vs. 113-29/0.15%

+2,000 TYX5 114/114.25/114.5 call flys, 2 vs. 113-24/0.08%

2,000 TYX5 113.25/113.75 1x2 call spds, 6 ref 113-20.5

MNI BONDS: EGBs-GILTS CASH CLOSE: Light Bull Flattening Ahead Of UK CPI

European long-end yields fell slightly Tuesday, with UK CPI data looming.

- The highlight of the session was the release of UK September public finance data which showed a slightly lower-than-expected public sector net borrowing figure plus downward revision to August.

- That saw the UK yield curve bull flatten, mirrored across EGBs, and accelerating in mid-afternoon after US President Trump said on social media that there was a possibility of allies potentially "going into Gaza with a heavy force".

- The German curve bull flattened, with the UK's twist flattening.

- Periphery/semi-core EGB spreads closed slightly wider.

- Wednesday's scheduled highlight is the UK inflation data release - MNI's preview is here. As we note in the preview, despite some BOE MPC members appearing to have more entrenched views, we think that this data release will have huge importance for the prospects for a Q4 cut.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is unchanged at 1.908%, 5-Yr is down 1.3bps at 2.155%, 10-Yr is down 2.5bps at 2.552%, and 30-Yr is down 3.6bps at 3.128%.

- UK: The 2-Yr yield is up 0.4bps at 3.858%, 5-Yr is down 0.9bps at 3.944%, 10-Yr is down 2.7bps at 4.478%, and 30-Yr is down 4.3bps at 5.266%.

- Italian BTP spread up 0.3bps at 79.2bps / French OAT up 0.7bps at 79.2bps

MNI EGB OPTIONS: Upside Lean Remains Across European Rate Options Tuesday

Tuesday's Europe rates/bond options flow included:

- DUZ5 107.40/107.50cs, sold at 1.25 in 10k

- RXF6 128.50p, bought for 32 in 3.4k

- ERH6 98.00/98.0625/98.125/98.1875 call condor, paper pays 0.5 in 2.25k

- ERH6 98.125/98.25cs vs ERZ5 98.0625/98.1875cs, bought for 2 in 1.5k

- ERJ6 98.25/98.43/98.62c fly, bought for 2.25 in 5k

- ERM6/ERZ5 97.9375p calendar spread, bought for 1.75 in 4k

- ERU6 98.50/75 1x1.5 call spread, paper pays 1.0 for 5k

- 0RH6 98.25/98.50/98.75c fly, bought for 2.5 in 5k

- SFIG6 96.40/96.55cs 1x1.5, bought for 2.5 in 3k

- SFIH6 96.50/96.55cs, bought for 1.25 in 2k

MNI FOREX: Gold Unwind Assists Greenback Outperformance, JPY Notably Weaker

- Tuesday’s session was categorized by a sharp selloff for precious metals, with the significant 6% unwind for spot gold providing a bid for the greenback against G10 peers. As such, the USD index has risen 0.3% on the session, to extend the bounce from Friday’s lows to just shy of 1%.

- The Japanese yen has been hardest hit in the G10 space, as markets focussed on Japan’s parliament confirming Sanae Takaichi as the new PM, and details emerged surrounding her new cabinet and her imminent plans to compile a new stimulus package. Furthermore, with Satsuki Katayama taking the finance minister role, expectations for a fiscal phase prioritising an Abenomics-like policy set have been reinforced.

- USDJPY rose from overnight lows of 150.47 to reach a session high of 152.17, with the recovery from last Friday’s low in USDJPY is beginning to highlight a stronger bullish signal. The pair fell from its best levels as PM Takaichi said there is "no immediate plan to revise the gov't-BoJ joint agreement on economic policy.

- Elsewhere, the Canadian dollar has outperformed following an above expectation set of inflation data. For USDCAD, the move lower narrows the gap to initial support at the 20-day EMA, which lies at 1.3972. However, it is worth highlighting that moving average studies are in a bull-mode position, highlighting a dominant uptrend.

- Initial weakness for EURCHF saw the cross trade within 4 pips of significant medium-term support at 0.9206. A break of this level would place EURCHF at the lowest level since the peg removal in 2015, and may garner attention as the inaugural SNB minutes are released this Thursday.

- In emerging markets, the dollar/gold dynamic has weighed significantly on the South African Rand, standing out among the EM FX basket. Despite the 1% USDZAR rally, spot remains shy of last Thursday’s highs, located at 17.4857, while bearish trend conditions do remain intact overall. A clear break of the 50-day EMA (at 17.44) would signal a potential reversal and open 17.8190, the Sep 4 high.

MNI OPTIONS: Expiries for Oct22 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1525(E732mln), $1.1595-00(E1.1bln), $1.1620-25(E586mln), $1.1640-50(E750mln) $1.1810-30(E1.1bln)

- USD/JPY: Y149.90-00($1.5bln), Y151.00($876mln), Y152.00($1.1bln)

- EUR/GBP: Gbp0.8740(E498mln)

- AUD/USD: $0.6535(A$516mln)

- NZD/USD: $0.5700(N$1.2bln)

- USD/CAD: C$1.3800($1.9bln), C$1.4085($551mln), C$1.4200($1.1bln)

- USD/CNY: Cny7.3000($749mln)

MNI US STOCKS: Late Equities Roundup: DJIA Outperforms After New Record High

- Stocks remain mixed late Tuesday, the DJIA outperforming after managing to mark a new record high of 47,125.66 in the first half. A couple social media posts by President Trump tempered risk sentiment, however.

- Stocks whipsawed off early session highs after Pres Trump social media post warning retribution "if Hamas continues to act badly, in violation of their agreement with us." Stocks reacted negatively a second half post by President Trump that while he anticipates having "a good deal with Xi" the meeting in S Korea at end of the month may NOT happen.

- While Treasury futures drift near highs (10Y yield fell to 3.9455%), equities have managed to stay off early lows. A noticeable exception: mining stocks underperformed after Gold fell sharply (appr -240.0 at 1050ET to 4115.0, appr -6.3% from session highs).

- Currently, the DJIA trades up 280.59 points (0.6%) at 46,988.65, S&P E-Minis up 6.5 points (0.1%) at 6,781, Nasdaq down 16.9 points (-0.1%) at 22,974.59.

- In addition to Materials and Utility Services sector share underperformed: Newmont Corp -8.97%, Philip Morris Int -5.45%, Albemarle Corp -3.93%, Constellation Energy -3.62% Vistra Corp -3.19% and NRG Energy -2.23.

- On the positive side, Consumer Discretionary and Industrials sector shares outperformed in the first half, General Motors surged +15.5% after reporting better than expected Q3 earnings, Lululemon Athletica +6.08%, Ford Motor +5.30%, CarMax +4.58% and Aptiv +3.86%..

- Supporting the Industrials sector: RTX +8.42%, 3M Co +6.09%, Carrier Global +3.68%, Builders FirstSource +3.44% and Stanley Black & Decker +3.29%.

- Reporting earnings after the close: Netflix, Capital One Financial, Mattel, Western Alliance Bancorp (in the hot seat last week after announcing bad loan losses), Omnicom, EQY and Texas Instruments.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Support Intact

- RES 4: 6850.87 1.618 proj of the Aug 1 - 15 - 20 price swing

- RES 3: 6831.38 2.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6819.25 1.500 proj of the Aug 1 - 15 - 20 price swing

- RES 1: 6812.25 High Sep 9 and the bull trigger

- PRICE: 6778.50 @ 1455 ET Oct 21

- SUP 1: 6621.99 50-day EMA

- SUP 2: 6540.25 Low Oct 10 and a key short-term support

- SUP 3: 6506.50 Low Sep 5

- SUP 4: 6427.00 Low Sep 2

A bullish theme in S&P E-Minis remains intact and the contract is trading above support at the 50-day EMA. The average, currently at 6621.99, has been pierced but remains intact - for now. Note that the Oct 10 low of 6540.25 marks the key short-term support. Clearance of this level would undermine a bull theme. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend. The bull trigger is 6812.25, the Oct 9 high.

MNI COMMODITIES: Precious Metals Fall Sharply, Crude Ticks Higher

- Precious metals sold off sharply on Tuesday, with spot gold currently down by 5.6% at $4,113/oz and silver down by 7.7% at $48.4/oz, albeit off session lows. Platinum and palladium have also fallen by 5-6%.

- There was no obvious trigger for today’s weakness, which has allowed an overbought condition to swiftly unwind.

- As noted earlier, the moves have been largely isolated to precious metals, supporting the idea that they have been flow/momentum driven, with profit-taking at play after an extremely strong rally since August.

- For gold, today’s losses have rapidly narrowed the gap to key support at $4,030.4, the 20-day EMA. A break of this would open $3,819.6, the Oct 2 low.

- For silver, the move unwinds some of the recent liquidity squeeze, with price piercing initial support at $49.037, the 20-day EMA. A clear break of this level would open the next support at $45.135, the 50-day EMA.

- Elsewhere, WTI has risen today, having recovered from earlier losses. Geopolitical developments weighed against the supply/demand outlook as seaborne crude in transit continues to rise.

- WTI Nov 25 is up by 0.5% at $57.8/bbl.

- Despite the move, a bearish theme in WTI futures remains intact, with sights still on $54.89 next, the May 5 low. Initial firm resistance is seen at $61.61, the 50-day EMA.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 22/10/2025 | 0600/0700 | *** | Consumer inflation report | |

| 22/10/2025 | 0600/0700 | *** | Producer Prices | |

| 22/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 22/10/2025 | 1100/1300 | ECB de Guindos at Barcelona Real Assets Meeting | ||

| 22/10/2025 | 1225/1425 | ECB Lagarde Keynote at Frankfurt Finance & Future Summit | ||

| 22/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 22/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 22/10/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 22/10/2025 | 2000/1600 | Fed Governor Michael Barr |