MNI ASIA MARKETS ANALYSIS: Curves Bull Flatten Ahead FOMC Mins

HIGHLIGHTS

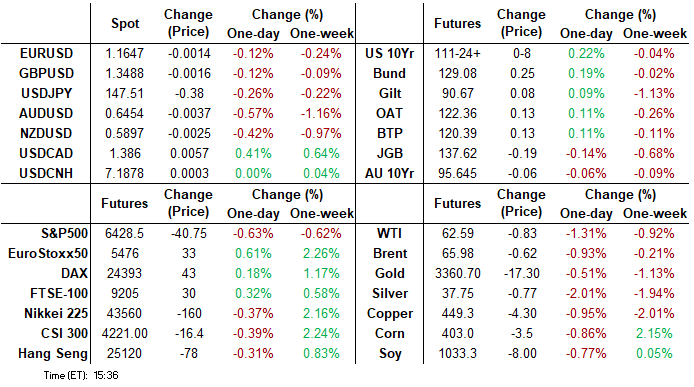

- Treasuries look to finish near late Tuesday session highs, curves bull flattening, US$ rising to one week highs, stocks in retreat ahead of Wednesday's July FOMC minutes.

- Rates rebounded after this morning's data - lower than expected build permits outweighing higher than expected housing starts, while softer Canadian CPI aggregates added to support.

- Bund yields traded almost entirely within the prior session's ranges, with the 2.80% level holding for the 10Y.

US TSYS

MNI US TSYS: Early Support From Soft US Build Permits & Canadian CPI Data

- Treasuries look to finish near late Tuesday session highs (TYU5 +8.5 at 111-25), curves bull flattening with bonds outperforming (2s10s -2.245 at 54.607, 5s30s -.571 at 107.952).

- Rates rebounded after this morning's data - lower than expected build permits outweighing higher than expected housing starts, while softer Canadian CPI aggregates added to support.

- Housing starts were far stronger than expected in July at 1428k (saar, cons 1297k) after an upward revised 1358k (initial 1321k) in June. It left starts rising 5.2% M/M (cons -1.8%) after a stronger than first thought 5.9% (initial 4.6%) as they bounced after a -8.3% M/M decline in May (also revised from -9.7%).

- Canadian all-items CPI rose 1.73% Y/Y unrounded (1.86% prior, 1.8% expected by MNI median), and 0.12% M/M (0.18% prior, 0.4% expected).

- US$ rising to one week highs, price action was assisted by a dip lower for the major equity benchmarks, as a cautious risk off mood prevails given the lack of progress regarding a Russia/Ukraine ceasefire and the notable weakness for tech stocks in the US.

- Stocks in retreat (Nasdaq -323.04 at 21306.66) ahead of Wednesday's July FOMC minutes not to mention Friday's annual economic symposium in Jackson Hole Wyoming.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.34% (-0.02), volume: $2.810T

- Broad General Collateral Rate (BGCR): 4.33% (-0.01), volume: $1.159T

- Tri-Party General Collateral Rate (TCR): 4.33% (-0.01), volume: $1.134T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $112B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $244B

FED Reverse Repo Operation

RRP usage retreats to $22.344B this afternoon (lowest since April 5, 2021) from $38.240B yesterday, total number of counterparties at 29.

US SOFR/TREASURY OPTION SUMMARY

SOFR and Treasury options traded a little more evenly between calls & puts Tuesday after better SOFR call interest in the first half. Underlying futures trading near late session highs helped projected rate cut pricing gain some traction vs. early morning (*) levels: Sep'25 at -21.7bp (-20.9bp), Oct'25 at -35.1bp (-34.1bp), Dec'25 at -54.4bp (-53.5bp), Jan'26 at -65.6bp (-64.1bp).

SOFR Options:

+10,000 SFRU5 95.81 puts, 3.0 vs. 95.9125/0.21%

4,400 0QV5 96.56/96.68 put spd vs. 2QV5 96.50/96.62 put spds

+2,000 SFRU5 95.93/96.00/96.06/96.12 call condors, 0.75

+2,000 SFRU5 95.75/95.81/95.87 put flys, .37 ref 95.90

+2,000 SFRU5 96.12/96.25 call spds. .87 ref 95.897

+4,000 SFRU5 96.00/96.12/96.18 broken call flys, 1.0

6,600 SFRX5 96.12/96.25/96.50 call trees ref 96.205

2,000 2QZ5 96.12/96.31/96.56 2x3x1 put flys

5,000 0QU5 96.50/96.68 put spds ref 96.795

3,500 SFRX5 96.12/96.25/96.50 broken call trees ref 96.195

2,000 SFRZ5 95.87/96.00 put spds

10,000 SFRU5 96.00/96.12 1x2 call spds

17,000 SFRU5 96.00/96.12/96.25 call flys ref 95.895 (adds to some +60k traded through Mon at .75)

(Note: Large late Monday buying in Oct'25 96.50 calls, volume 180,197 saw open interest climb +95,227 to 226,924)

Treasury Options: (reminder Sep options expire Friday)

12,300 wk5 FV 107.5/108 2x1 put spds 1 vs. 108-29/0.05%

-6,000 TYV5/TYZ5 112 call spds 29

-5,000 TYV5 110.5/112.5 call over risk reversals, 11 vs. 111-23

-7,300 FVV5 108.25/109.5 call over risk reversals, 3 vs. 108-28

2,000 USU5 117/119 call spds ref 114-07

+5,000 TYV5 111.5 puts, 45 ref 111-19/0.48%

50,000 TYV5 113 calls, 19 ref 111-20

over 10,200 TYU5 112.5 calls, 2 last

over 7,800 TYU5 113 calls, 1 last

over 9,000 TYV5 111 puts, 31 last ref 111-19

4,700 TYU5 113 calls, 1 ref 111-19

3,900 TUV5 103.75/104.5 strangles ref 104-01.38

1,500 TYU5 111.5/111.75 2x3 call spds ref 111-16.5

1,250 TUV5 103.5 puts ref 104-01.75

1,750 TUV5 103.75 puts ref 104-01.88

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Underperform Again Pre-UK CPI

European curves flattened Tuesday, with Gilts underperforming yet again ahead of UK CPI data.

- With no evident catalysts today amid a thin data/speaker slate, Monday's weakness in Gilts on the back of lingering fiscal concerns spilled over into today's session. 10Y Gilt yields hit a fresh post-May high (4.756%) in early trade.

- Bund yields traded almost entirely within the prior session's ranges, with the 2.80% level holding for the 10Y. Longer-end German instruments led the space overall in a broader rally over the most of the remainder of the session, with Buxl rallying after yields hit a fresh post-2011 high.

- Yields fell to session lows a little over an hour before the cash close, as equities tumbled (led by US megacap tech), resulting in a modest safe-haven bid that also saw periphery EGB spreads move a little wider.

- The German curve bull flattened on the day, with the UK's twist flattening. Periphery/semi-core EGB spreads closed mixed, with BTPs underperforming.

- Attention Wednesday will be on the UK CPI report. MNI's preview is here: the BOE MPC is focused on headline CPI which is expected to come in higher than in June.

- We also get an appearance by ECB's Lagarde and the Swedish Riksbank decision, as well as final Eurozone July inflation.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.1bps at 1.958%, 5-Yr is down 1.3bps at 2.306%, 10-Yr is down 1.3bps at 2.75%, and 30-Yr is down 1.5bps at 3.323%.

- UK: The 2-Yr yield is up 1.5bps at 3.98%, 5-Yr is up 1.5bps at 4.138%, 10-Yr is up 0.2bps at 4.74%, and 30-Yr is down 0.9bps at 5.602%.

- Italian BTP spread up 1.2bps at 80.5bps / French OAT down 0.1bps at 68.3bps

MNI OPTIONS: A Couple Of Sonia Call Condors Sold Ahead Of UK CPI

Tuesday's Europe rates/bond options flow included:

- RXU5 128.5/128/127.5p fly, bought for 5 in 2k.

- RXX5 132c, bought for 15 in 1.2k

- SFIH6 96.40/96.60cs, bought for 5 in 7k.

- SFIZ5 96.15/96.25/96.35/96.45c condor, sold at 2.75 in 6k.

- SFIZ5 96.10/25/40/55 call condor, paper sells for 5.0 in 3k (covered 21 delta)

MNI FOREX: CAD Weakens Post CPI, Softer Equities Weigh on AUD & NZD

- Despite some initial weakness on Tuesday, the USD index tilted back into positive territory late in the session, set to moderately extend the rally this week. Price action was assisted by a dip lower for the major equity benchmarks, as a cautious risk off mood prevails given the lack of progress regarding a Russia/Ukraine ceasefire and the notable weakness for tech stocks in the US.

- Canada inflation data came in slightly below expectations and while unlikely to prompt renewed easing from the BOC, the Canadian dollar has sold off today. USDCAD has risen 0.4% to 1.3860, closing in on the August 01 highs off 1.3879. A break of this level would cancel a bear threat and resume the recent bull cycle.

- Elsewhere, risk dynamics have negatively impacted the likes of AUD and NZD, while Norwegian Krone is at the bottom of the G10 leaderboard.

- For AUDUSD, the pair is comfortably off its most recent highs but continues to trade in a range. From a trend perspective, the condition remains bullish highlighted by MA studies that remain in a bull-mode position; however, spot has narrowed the gap substantially to key support at 0.6419, the Aug 1 low.

- Kiwi weakness is notable ahead of Wednesday’s RBNZ decision, recording the first print below 0.5900 in two weeks. With a 25bp cut widely forecast, attention will be on the revised RBNZ outlook and tone of the statement and press conference. The focus is likely to be on the projected OCR path and whether it is revised lower suggesting further easing towards stimulatory territory as excess capacity persists.

- GBPUSD has consolidated around the 1.35 mark on Tuesday amid gilts paring some of yesterday's weakness. A technical bull cycle remains intact, keeping sights on 1.3636, the 76.4% retracement of the bear leg between Jul 1 and Aug 1 ahead of tomorrow's UK CPI release.

- FOMC minutes are also due for release tomorrow before the Jackson Hole symposium kicks off Thursday.

MNI OPTIONS: Expiries for Aug20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E915mln), $1.1600(E854mln), $1.1660-75(E1.4bln)

- USD/JPY: Y147.25-35($982mln), Y148.00-10($1.5bln)

- USD/CAD: C$1.3800($1.1bln), C$1.3835-55($872mln)

- USD/CNY: Cny7.1050($500mln)

MNI US STOCKS: Late Equities Roundup: Extending Lows as Greenback Rises

- Stocks continued to extend session lows late Tuesday as the US$ climbed to one week highs (BBDXY +2.71 at 1207.33). Currently, the DJIA trades down 62.57 points (-0.14%) at 44847.07, S&P E-Minis down 43.75 points (-0.68%) at 6425, Nasdaq down 319.9 points (-1.5%) at 21308.83.

- Information Technology and Communication Services sectors continued to underperform in the second half, the former weighed by Palantir Technologies -9.02%, Oracle Corp -5.30%, Advanced Micro Devices -4.90%, First Solar -4.58% and Super Micro Computer -4.58%.

- The Communication Services sector was weighed by: Trade Desk -4.48%, Warner Bros Discovery -2.66%, Netflix -2.47% and Meta Platforms -1.79%.

- On the positive side, Real Estate, Consumer Staples and Health Care sectors continued to outperform. Investment trust stocks supported the former following this morning jump in (albeit volatile) Housing Starts data: Prologis +4.07%, Federal Realty Investment Trust +2.33%, Kimco Realty +1.97% and Weyerhaeuser +1.73%.

- Supporting Consumer Staples stocks included: Philip Morris Int +1.42%, Procter & Gamble +1.40% and PepsiCo +1.40%. Meanwhile, pharmaceuticals buoyed the Health Care sector in late trade: Molina Healthcare +2.76%, Baxter International +2.29% and Labcorp Holdings +2.18%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Trend Needle Points North

- RES 4: 6600.00 Round number resistance

- RES 3: 6554.98 2.0% 10-dma envelope

- RES 2: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6508.75 High Aug 15 and Alltime High

- PRICE: 6426.75 @ 1455 ET Aug 19

- SUP 1: 6399.62 20-day EMA

- SUP 2: 6313.25 Low Aug 6

- SUP 3: 6275.86 50-day EMA

- SUP 4: 6239.50 Low Aug 1

The dominant uptrend in S&P E-Minis remains intact and the contract is trading just below its recent highs. Moving average studies are in a bull-mode position, highlighting a clear uptrend. A resumption of gains would pave the way for a climb towards 6523.63, a Fibonacci projection. On the downside, supports to watch are; 6399.62, the 20-day EMA, and 6275.86, the 50-day EMA.

MNI COMMODITIES: Crude Loses Ground, Gold Edges Lower, Copper Bear Threat Seen

- Crude prices have lost ground today as the market weighs the outlook for a ceasefire/peace deal in Ukraine and possible trilateral talks between the US, Ukraine and Russia.

- WTI Sep 25 is down by 1.6% at $62.4/bbl.

- A meeting between Zelenskyy and Putin could happen before the end of August, with another including Trump to occur thereafter.

- WTI futures remain in a clear bear cycle, and the contract is trading closer to its recent lows. A key support at $61.99, the Jun 30 low, was recently breached, strengthening a bearish theme.

- A continuation lower would open $57.71, the May 30 low.

- Meanwhile, spot gold has fallen by 0.4% to $3,318/oz, as the USD index tilted back into positive territory late in the session, amid the cautious risk-off mood.

- A bull cycle in gold remains intact and the sideways trend that has been in place since the April peak appears to be a corrective phase - a pause in the uptrend.

- A resumption of gains would open $3,439.0, the Aug 23 high. On the downside, first support to watch lies at $3,268.2, the Jul 30 low.

- Copper has also fallen by 1.0% today to $449/lb.

- The sharp reversal down from the Jul 30 high cancels a recent bullish theme and instead highlights a bearish threat. A continuation lower would signal scope for a test of key support at $418.85, the Apr 7 low.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 20/08/2025 | 0600/0700 | *** | Consumer inflation report | |

| 20/08/2025 | 0600/0800 | ** | PPI | |

| 20/08/2025 | 0710/0910 | ECB Lagarde at WEF Intl Business Council | ||

| 20/08/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 20/08/2025 | 0900/1100 | *** | HICP (f) | |

| 20/08/2025 | 0900/1100 | Q2 Flash Vacancies and Labour Cost Index | ||

| 20/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 20/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 20/08/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 20/08/2025 | 1500/1100 | Fed Governor Christopher Waller | ||

| 20/08/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 20/08/2025 | 1800/1400 | FOMC Minutes | ||

| 20/08/2025 | 1900/1500 | Atlanta Fed's Raphael Bostic | ||

| 21/08/2025 | 2300/0900 | *** | Judo Bank Flash Australia PMI | |

| 21/08/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI |