MNI ASIA MARKETS ANALYSIS: Cautious Risk-On Ahead Jobs Data

HIGHLIGHTS

- Treasuries look to finish near late session highs Monday, cautious risk-on tone as Canada withdrew plans to implement a digital tax on US tech companies, trade talks to resume with US, Hassett said.

- Despite Tsy curve bull flattening, projected rate cuts remained firm - SOFR pricing in over 66bp in cuts by December.

- Stocks extended highs in late trade - potentially month-end related as accounts reallocated ahead of Thursday's June employment report.

- US$ ratcheted lower in the second half, Bbg US$ index falling to 1190.5 - lowest level since March 2022.

US TSYS

MNI US TSYS: Tsys Near Late Session Highs with Stocks, US$ at March '22 Lows

- Treasuries look to finish near late Monday highs, curves bull flattening amid mildly cautious risk-on tone after Canada withdrew last Friday's plans to implement a digital tax on US tech companies, trade talks to resume with US, Hassett said.

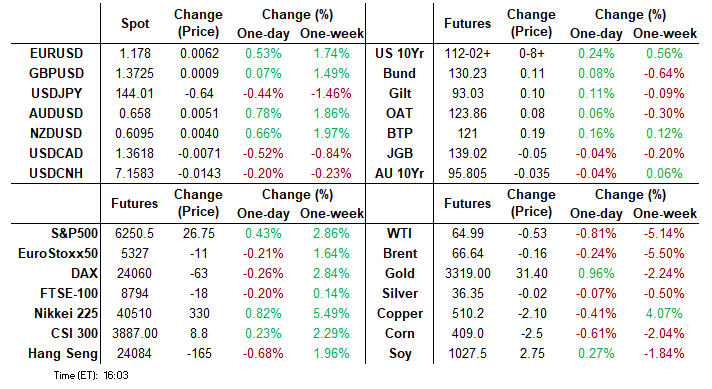

- Tsy Sep'25 10Y trades +10 at 112-04 after the bell, key resistance above at 112-23 (High May 1), 2s10s -2.210at 50.476, 5s30s -1.630 at 98.714.

- Amid the renewed focus on rate differentials in FX, the bull flattening move for the US curve has helped the US dollar extend its most recent weakness, with the dollar index falling around 0.5% to fresh cycle lows (March 2022 levels).

- The moves come amid President Trump stepping up his criticism of Fed Chair Powell and his ‘entire board’ over the level of US interest rates. Notably, Goldman Sachs have also pulled forward their call for the next Fed cut to September.

- Also note: Morgan Stanley strategists suggest buying SFRZ5 futures ahead of tomorrow's May Jolts and Thursday's June Non-Farm Payrolls release that may underpin rate cut projections that are over halfway between 50bp to 75bp in rate cuts by year end. "Downside risks to US labor market data remain underpriced, especially considering the potential for near 0k payroll prints starting as soon as July," MS suggested in a recent strategy piece.

- Stocks extended late Monday session highs - either caution to the wind ahead of a heavy data (shortened) week (markets are closed for the Independence Day holiday Friday, which draws the June employment release one day forward). Or month-end tied buying as money managers reallocated funds.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.39% (-0.01), volume: $2.775T

- Broad General Collateral Rate (BGCR): 4.37% (-0.01), volume: $1.083T

- Tri-Party General Collateral Rate (TCR): 4.37% (-0.01), volume: $1.058T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $122B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $262B

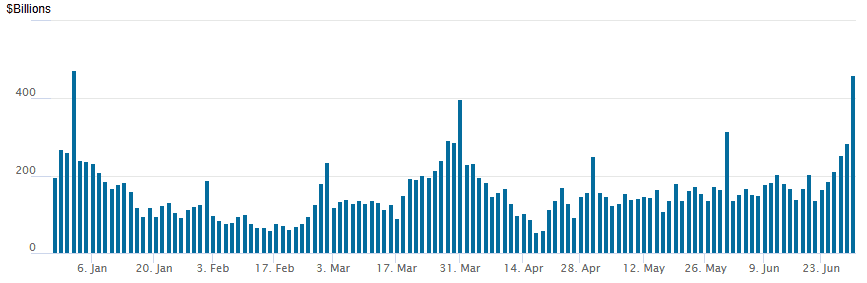

FED Reverse Repo Operation: Highest Since December 31

RRP usage surged to $460.731B this afternoon (highest since December 31) from $285.742B Friday, total number of counterparties climbs to 62. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option trade looked mixed on net, some chunky flows traded sporadically: Large Mar'26 SOFR Straddle buy vs. calls, while Treasury options say a pick-up in Sep & Aug 10Y call buying in the second half. Projected rate cut pricing gains slightly vs. late Friday (*) levels: Jul'25 at -5.3bp (-4.8bp), Sep'25 at -28.6bp (-28.2bp), Oct'25 steady at -46.3bp, Dec'25 at -66.8bp (-66.2bp).

SOFR Options:

-4,000 0QZ52QZ5 96.00 put spd, 2.0 net flattener

+2,000 0QQ5 96.62/2QQ5 96.50/3QQ5 96.12 put fly, 1.5 net db

+45,000 SFRH6 96.12 straddles vs. 97.00 calls, 28.5-29.0 vs. 97.00/0.20%

+5,000 SFRN5 95.75/95.81 put spds, 0.25

+2,000 SFRU5 95.75/95.81/95.87 put flys, .25 ref 95.985

+4,000 2QZ5 96.25 puts, 9.0 vs. 96.785/0.20%

Block/screen, 4,000 SFRU6 97.00/97.75 2x1 put spds, 4.0 net ref 96.91 to -.92

-1,500 0QQ5 97.50 calls, 3.0 ref 96.92

2,000 SFRN5 95.87 puts

-3,000 SFRU5 96.12/96.25 1x2 call spds, 5.5

Treasury Options:

25,000 TYQ5 110.5/111.5 3x2 put spds, 24 ref 112-04

+30,000 TYU5 112 calls, 1-04 ref 112-03

12,500 TYQ5 113 calls, 21 ref 112-02.5

3,500 TYQ5 110.75/111.25 put spds

10,000 TYU5 108/110 put spds ref 111-29

-2,000 FVQ5 107.75 puts, 5

over +11,300 FVQ5 108 puts, 7.5-8

6,000 TYQ5 110 puts

+1,500 TYU5 109.5/111 put spds, 24 ref 111-31.5 vs. 111-29/0.10%

+2,000 wk1 TY 111.25 puts, 6 vs. 111-28.5/0.10%

+1,100 USQ5 116/119 2x3 call spds, 105 ref 114-30/0.36%

MNI BONDS: EGBs-GILTS CASH CLOSE: Bunds Underperform Despite Softer German Inflation

Gilts outperformed Bunds Monday despite softer-than-expected Eurozone inflation readings.

- Early data showed a downside surprise in German state-level inflation tracking, with national HICP turning out 0.2pp below the pre-consensus, which helped Bunds (and Gilts) catch an early bid.

- A de-escalation in US-Canada trade tensions also appeared to help Global FI early.

- The session was more notable for idiosyncratic moves that had no apparent immediate macro or headline drivers.

- A selloff in Gilts to yields' session highs (10Y 4.514%) in early afternoon trade quickly faded. Later in the afternoon Bunds dropped sharply, again with no apparent macro driver but instead appeared to be flow-related with large selling at around 1530 London time.

- The German curve bear steepened on the day, with the UK's twist steepening.

- Periphery/semi-core EGB spreads mostly tightened modestly, with BTPs outperforming.

- Tuesday's calendar includes panel appearance with both ECB's Lagarde and BOE's Bailey, May ECB inflation expectations, and the second reading of the welfare reform bill in the UK.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.1bps at 1.861%, 5-Yr is up 0.7bps at 2.17%, 10-Yr is up 1.5bps at 2.607%, and 30-Yr is up 3bps at 3.1%.

- UK: The 2-Yr yield is down 2.2bps at 3.817%, 5-Yr is down 1.8bps at 3.95%, 10-Yr is down 1.5bps at 4.489%, and 30-Yr is up 0.7bps at 5.279%.

- Italian BTP spread down 1.2bps at 86.9bps / French OAT down 0.5bps at 67.4bps

MNI EGB OPTIONS: A Little More Downside Than Usual With US Payrolls In View

Monday's Europe rates/bond options flow included:

- OEU5 117.50/116.50ps, sold at 29.5 in 2k

- RX (3rd July) 130.5/131.00cs, bought for 16 in 2.17k (weekly)

- RXQ5 129p, bought for 30 and 31 in ~8.7k

- RXV5 127/125 put spread, bought for 13.5k vs 130.41 RXU5 13 delta @ 0.36

- ERZ5 98.25 call vs 2RZ5 98.00 call, trades for -1.5 to -1.0 in 15k

- 0RU5 97.875/97.75ps, bought for 1 in 5k

MNI FOREX: USD Downtrend Extends as Trump Steps Up Rhetoric on Fed Rates

- Amid the renewed focus on rate differentials in FX, the bull flattening move for the US curve has helped the US dollar extend its most recent weakness, with the dollar index falling around 0.5% to fresh cycle lows (March 2022 levels). The moves come amid President Trump stepping up his criticism of Fed Chair Powell and his ‘entire board’ over the level of US interest rates. Notably, Goldman Sachs have also pulled forward their call for the next Fed cut to September.

- Gains across G10 have been led by the likes of CHF (+0.71%) AUD (+0.72%) and NZD (+0.64%) as the continued resilience for major equity benchmarks underpins the firm sentiment for risk. For AUDUSD, this promotes spot to a fresh cycle high above 0.6570. A clear break of key resistance and the bull trigger, at 0.6552, would confirm a resumption of the trend and initially opening 0.6603, the Nov 11 2024 high.

- USDCHF now tracks around 0.7930 as the move below the psychological 0.80 handle extends. Indeed, CHFJPY has had an impressive bounce of the early morning lows at 180.20 to trade at a fresh record high once more above 181.75.

- EURUSD has also edged to fresh session/cycle highs Monday, continuing to track at the best traded levels since September 2021 above 1.1770. Last week’s gains reinforced the uptrend, emboldened by a breach of the bull trigger at 1.1631, the Jun 12 high. Immediate sights are on 1.1783, a Fibonacci projection, before 1.1821, the Sep 16 2021 high.

- Rates/dollar dynamics may place a greater focus than usual on this week’s US employment report, notably scheduled on Thursday owing to the July 4th holiday. Separately, ISM and JOLTS data are scheduled tomorrow. The global calendar kicks off with the release of Eurozone HICP.

MNI US STOCKS: Late Equities Roundup: Alternative Energy Under the Weather

- Stocks are mildly higher in late Monday trade - holding to narrow ranges ahead of a heavy data (shortened) week. Markets are closed for the Independence Day holiday Friday, which draws the June employment release one day forward.

- Currently, the DJIA trades up 113.14 points (0.26%) at 43931.97, S&P E-Minis up 7 points (0.11%) at 6231, Nasdaq up 12.4 points (0.1%) at 20286.85.

- Stocks gained earlier after Canada withdrew plans to implement a digital tax on US tech companies economic advisor Kevin Hassett confirmed Monday - the tax had spurred Pres Trump to terminate trade talks late last Friday.

- Otherwise, "90 deals in 90 days" remains a tall order ahead the July 9 deadline, while Pres Trump floated the idea of keeping 25% tariffs on Japan’s cars as talks between the two nations continued with little more than a week to go before a slew of higher duties are set to kick in if a trade deal isn’t reached.

- Technology sector shares continued to lead gainers in late trade: Hewlett Packard Enterprise +11.65%, Juniper Networks +8.35%, First Solar +8.21%, Palantir Technologies +5.15%, Oracle Corp +4.59% and Arista Networks +3.53%.

- Conversely, Industrials - particularly stocks that dealt with alternative energy retreated Monday as Pres Trump's "Big" policy looks to withdraw clean energy initiatives: Ralliant Corp -8.25%, Fortive Corp -5.21%, Boeing -3.00%, Lamb Weston Holdings -2.88% and Albemarle Corp -2.71%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Bulls Remain In The Driver’s Seat

- RES 4: 6300.00 Round number resistance

- RES 3: 6281.12 1.618 proj of the Apr 7 - 10 - 21 price swing

- RES 2: 6277.50 High Feb 19 and a bull trigger

- RES 1: 6255.00 Intraday high

- PRICE: 6239.00 @ 14:54 BST Jun 30

- SUP 1: 6069.53/5952.84 20- and 50-day EMA values

- SUP 2: 5811.50 Low May 23

- SUP 3: 5645.75 Low May 7

- SUP 4: 5500.00 Low Apr 30

The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract has started this week on a firm note. Short-term resistance and a bull trigger at 6128.75, the Jun 11 high, has recently been breached. The clear break confirms a resumption of the uptrend that started Apr 7. The 6200.00 handle has been cleared too, this opens 6277.50, the Feb 21 high and bull trigger. Key support is at the 50-day EMA - at 5952.84.

COMMODITIES

MNI AMERICAS OIL: WTI crude has been under some pressure today

June 30 - Americas End-of-Day Oil Summary: WTI crude has been under some pressure today with the market now weighing the prospects of another large OPEC+ output hike at the meeting on July 6, while geopolitical risks in the Middle East have eased.

- China's factory activity improved slightly but still contracted for a third straight month in June, as weak domestic demand and soft exports weigh amid US trade uncertainty.

- Oil traders expect OPEC+ will agree a fourth bumper oil supply increase on July 6, Bloomberg reports. Eight key OPEC+ nations have agreed on 411kb/d increases in each of the previous three months, and several delegates are ready to consider the same hike again for August.

- President Trump has hinted at sanctions relief for Iran if 'they can be peaceful'. Trump said he doesn’t think he’ll need to extend the July 9 trade deadline he has imposed on countries to secure deals with the US to avoid higher tariffs.

- WTI Aug futures were down 0.6% at $65.11

- WTI Sep futures were down 0.3% at $63.84

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 01/07/2025 | 0630/0830 | ** | Retail Sales | |

| 01/07/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 01/07/2025 | 0740/0940 | ECB de Guindos Chairs Sintra Panel | ||

| 01/07/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 01/07/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 01/07/2025 | 0755/0955 | ** | Unemployment | |

| 01/07/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 01/07/2025 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 01/07/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 01/07/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 01/07/2025 | 0840/1040 | ECB Elderson Chairs Sintra Panel | ||

| 01/07/2025 | 0900/1100 | *** | HICP (p) | |

| 01/07/2025 | 1040/1240 | ECB Schnabel Chairs Sintra Panel | ||

| 01/07/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 01/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 01/07/2025 | 1330/1430 | BOE Bailey On Panel At Sintra Conference | ||

| 01/07/2025 | 1330/0930 | Fed Chair Jerome Powell | ||

| 01/07/2025 | 1330/1530 | ECB Lagarde On Sintra Panel | ||

| 01/07/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/07/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 01/07/2025 | 1400/1000 | * | Construction Spending | |

| 01/07/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 01/07/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 01/07/2025 | 1400/1000 | * | Construction Spending | |

| 01/07/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 02/07/2025 | 0130/1130 | * | Building Approvals | |

| 02/07/2025 | 0130/1130 | ** | Retail Trade |