MNI ASIA MARKETS ANALYSIS: Admin Telegraph Weaker Jobs Gains

HIGHLIGHTS

- Peter Navarro, counselor to Pres Trump, expressed the "need to revise expectations on monthly job numbers" Bbg. (NFP for January released tomorrow).

- Softer-than-expected US retail sales data appeared to have exacerbated the USDJPY decline, although the dollar has shown much broader stability against other G10 currencies.

- Looking ahead to Friday’s CPI report for January, we currently see a median unrounded estimate of 0.35% M/M for core CPI across nine analysts, pointing to upside risk to Bloomberg consensus of 0.3% M/M.

- Axios is running a report (in full, here) saying US President Trump might send a second aircraft carrier strike group to the Middle East to prepare for military action if negotiations with Iran fail.

US TSYS

MNI US TSYS: Tsys Hold Curve Flattening Gains Ahead Wednesday's January Employ Data

- US Treasuries look to finish higher Tuesday, curves bull flattening (2s10s -2.617 at 68.665, 5s30s -2.461 at 108.724) with bonds outperforming. Massive block sales over a 90 minute midday period: saw -115,000 TYH6 over 90 minutes from 112-17.5 to -15, as well as -95k FVH6 from 109-11.25 to -10.

- Incidentally, Treasury futures held near highs (TUH6 104-11.88, +1.5, TYH6 +10 at 112-16) after the $58B 3Y note auction (91282CQA2) drew 3.518% high yield vs. 3.519% WI; 2.62x bid-to-cover vs. 2.65x prior.

- Treasuries gained after Peter Navarro, counselor to Pres Trump, expressed the "need to revise expectations on monthly job numbers" Bbg. (NFP for January released tomorrow).

- Taking another round of geopolitical risk with a grain of salt - markets showed little react to Pres Trump stating he may may send second carrier to Iran if talks fail, Axios reporting. Trump is meeting the Israeli PM tomorrow, with the date for the next US Iran meeting yet to be finalised.

- Japanese assets have firmed on Tuesday, bolstered by comments from Finance Minister Katayama, who appears to have successfully calmed the markets on the timing and financing of the sales tax cut. Stabilisation across the JGB curve has facilitated an extension of the Japanese yen rebound, with the USDJPY pullback from yesterday’s post-election high reaching 2.35% at today’s 154.06 low.

- All focus turns to tomorrow’s US employment data. The report will need to be assessed holistically rather than focusing on any single number, although the unemployment rate should offer the cleanest single take.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.63% (-0.01), volume: $3.132T

- Broad General Collateral Rate (BGCR): 3.61% (-0.01), volume: $1.322T

- Tri-Party General Collateral Rate (TCR): 3.61% (-0.01), volume: $1.299T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $92B

- Daily Overnight Bank Funding Rate: 3.63% (+0.00), volume: $207B

FED Reverse Repo Operation

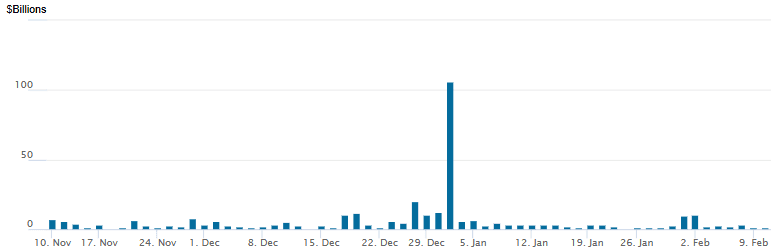

RRP usage inches up to $1.447B with 5 counterparties this afternoon vs. $1.306B Monday. Compares to December 12 low of $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option flow continued to revolve around low delta put structures Tuesday, buying cheaper downside insurance with underlying futures climbing higher (TYH6 resistance at 112-22), curves bull flattening (2s10s currently -2.608 at 68.674). Projected rate cut pricing slightly higher vs. late Monday levels (*): Mar'26 at -5bp (-4.7bp), Apr'26 at -11.6bp (-10.1bp), Jun'26 at -26.3bp (-24.8bp), Jul'26 at -35.6bp (-34.1bp).

SOFR Options:

3,000 SFRH6 96.37/96.43/96.50 put flys ref 96.395

+11,500 SFRM6/SFRZ6 96.31/96.43 put spd spd, 0.5 - flattener

8,000 SFRG6 96.43/96.50 call spds ref 96.40

4,000 0QM6 96.37/96.50 put spds

-5,000 SFRH6 96.37/96.50 put spds, 9.75 ref 96.40

-2,000 0QG6 96.62/96.87/97.12 2x3x1 put flys, 11.0 ref 96.885

+2,000 SFRZ6 97.00/97.25 call spds vs. 96.37 put, 3.0 ref 96.885

0qm6 96.50/96.375 ps vs 96.83 7% seller 2s 4k 644am

Treasury Options:

3,700 FVH6 109.25/109.5 call spds

-5,000 TYK6 112/113 strangles, 120 ref 112-10

8,000 FVH6 108.25/108.5/108.75 put flys ref 109-09

6,000 Wednesday wkly 109 puts, 4 ref 109-07.25

3,000 FVH6 109/109.25 call spds, 8 ref 109-06.75

over +33,500 FVH6 109 puts, 8.5 ref 109-06.25

3,500 FVH6 109.25 calls, 13 ref 109-06.5

-3,000 TUJ6 104.37 puts, 10 vs 104-13.75/0.46%

+2,000 TYH6 111/112 put spds, 11 ref 112-09.5

+2,000 TYH6 112.5/112.75/113.25 broken call trees, 1.0 ref 112-04.5

+3,000 TYH6 112.25 straddles, 40 ref 112-10.5

-1,500 USK6 110 puts, 25 ref 115-11

-2,000 TYK6 113.5 calls, 26

over 7,800 TYH6 112 puts, 12 ref 112-08.5

over +10,000 USJ6 118/119 call spds, 11 vs. 115-31 to -22/0.06%

over 4,900 wk2 TY 111.75 puts, 4

over 6,900 wk2 TY 112.25 puts, 17-15

2,000 wk2 TY 112.25 calls, 16

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Strengthen, But Continue To Lag Peers

Gilts once again underperformed Bunds, within a broad curve flattening move across European FI Tuesday.

- Long-end Gilts continued their recovery following vocal support in Monday's session by government ministers for PM Starmer, thereby alleviating near-term fiscal concerns.

- Despite being apparently weighed down by heavy sovereign and corporate supply, Bunds continued to track global peers and outperformed Gilts.

- Indeed, EGBs and Gilts tracked a Treasury rally in afternoon trade, with US data including retail sales and labour costs coming in softer-than-expected.

- On the day, the German curve bull flattened, with the UK's twist flattening.

- Periphery/semi-core EGB spreads were little changed.

- Wednesday's global focus will be the US employment report, though we also get the ECB's latest wage tracker and plenty of sovereign supply including a French syndication.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.9bps at 2.069%, 5-Yr is down 2.3bps at 2.383%, 10-Yr is down 3.2bps at 2.808%, and 30-Yr is down 3.7bps at 3.49%.

- UK: The 2-Yr yield is up 1.7bps at 3.643%, 5-Yr is down 0.6bps at 3.894%, 10-Yr is down 2.1bps at 4.506%, and 30-Yr is down 2.1bps at 5.325%.

- Italian BTP spread down 0.6bps at 60.5bps / French OAT down 0.8bps at 59.8bps

MNI OPTIONS: Sizeable Call Structures Cross Again, Including Euribor CFly

Tuesday's Europe rates/bond options flow included:

- DUH6 106.90/107.00cs 1x2, bought for 1 in 2.4k

- OEH6 116.75/117.5/117.75/119.25 call condor v 116/115.25 put spread, sells the condor at 15-13.5 in 14.9k

- ERH6 98.00/98.0625/98.12c fly, bought for 0.25 in 20k

- SFIM6 96.65/96.75/96.85/96.95c condor, bought for 2.75 in 5k

- SFIU6 96.75/0/96.50ps 1x2, sold at 6.5 in 19.5k (19.5kx39k)

- SFIZ6 96.60 puts 12K sold at 10.0

MNI FOREX: Japanese Yen Extends Post-Election Rally, NOK Firms Following CPI

- Japanese assets have firmed on Tuesday, bolstered by comments from Finance Minister Katayama, who appears to have successfully calmed the markets on the timing and financing of the sales tax cut. Stabilisation across the JGB curve has facilitated an extension of the Japanese yen rebound, with the USDJPY pullback from yesterday’s post-election high reaching 2.35% at today’s 154.06 low.

- Softer-than-expected US retail sales data appeared to have exacerbated the USDJPY decline, although the dollar has shown much broader stability against other G10 currencies. This dynamic has allowed cross/JPY to fall sharply, with the likes of GBPJPY and AUDJPY leading the declines.

- The sharp downswing for the GBPJPY today has seen spot narrow the gap substantially to the 50-day EMA, which intersects at 210.58. This average is notable given the fact we have not posted a daily close below it since October, and it acted as perfect support on Jan 26.

- The lack of any meaningful bounce for USDJPY following the US data despite broader greenback stability may leave the pair vulnerable to a further acceleration as we approach tomorrow’s US employment report. The next support of note is at 152.10, the Jan 27 low.

- In Norway, the January acceleration in CPI-ATE looks broad-based, with start-of-year price resets in the likes of rents and insurance highlighted. Any scope for payback in February won't be enough to ease Norges Bank concerns around inflation persistence, which leads EURNOK 0.65% lower on the session to fresh lows for 2026, narrowing the gap to support at the 2025 lows of 11.2614.

- Gradual downside momentum for EURCHF has been building in recent sessions. Session lows of 0.9095 represent the first test below 0.9100 since the removal of the peg in 2015.

- All focus turns to tomorrow’s US employment data. The report will need to be assessed holistically rather than focusing on any single number, although the unemployment rate should offer the cleanest single take.

MNI FX OPTIONS: Expiries for Feb11 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1820-30(E1.4bln), $1.1850(E742mln), $1.1900(E535mln), $1.2000(E1.8bln)

- USD/JPY: Y156.45-60($2.2bln)

- GBP/USD: $1.3575(Gbp537mln)

- EUR/GBP: Gbp0.8660(E821mln)

- USD/CAD: C$1.3700($874mln)

MNI US STOCKS: Late Equities Roundup: Late Session Consolidation

- First half support that saw DJIA rise to a new record high of 50,512.79 Tuesday, is consolidating late Tuesday as accounts squared up or took profits ahead of tomorrow's January employment report. Stocks drew some decent selling in the first half after Peter Navarro, counselor to Pres Trump, expressed the "need to revise expectations on monthly job numbers".

- Currently, the DJIA trades up 130.24 points (0.26%) at 50267.06, S&P E-Minis down 4.75 points (-0.07%) at 6978.25, Nasdaq down 66.4 points (-0.3%) at 23173.5.

- Utilities and Consumer Discretionary sector shares continued to lead advances in late trade: Vistra Corp gained +4.5% after upgrades from Goldman Sachs and Jefferies, Dominion Energy +3.29%, Eversource Energy +2.85% and Sempra +2.71%.

- Mostly travel related shares buoyed the Consumer Discretionary sector in the first half: Marriott International +9.19%, Hasbro Inc +7.42%, Norwegian Cruise Line +4.16%, PulteGroup +3.71% and Expedia Group +2.92%.

- Meanwhile, a mix of IT & Financial Services sector shares underperformed: S&P Global -9.12%, Raymond James Financial -8.20%, Western Digital -7.69%, Charles Schwab -7.69%, Ameriprise Financial -7.13%, Moody's -6.97%, Intel Corp -6.52%, Seagate Technology -6.40% and Sandisk Corp-5.51%.

MNI COMMODITIES: Crude Lower, Precious Metals Decline

- Crude has edged lower on Tuesday as the next development in US-Iran nuclear negotiations is awaited.

- WTI Mar 26 is down 0.3% at $64.2/bbl.

- President Trump is meeting the Israeli PM tomorrow, with the date for the next US Iran meeting yet to be finalised. Meanwhile, Axios reports that the US might send a second carrier group to the Middle East to prepare for military action if negotiations with Iran fail.

- A bull cycle in WTI futures remains intact, although the reversal from the Jan 29 high continues to highlight a corrective cycle.

- Attention is on support at the 20-day EMA, at $62.16. Key resistance has been defined at $66.48, the Jan 30 high.

- Elsewhere, precious metals have declined today, despite much broader stability in the US dollar, with gold down by 0.6% at $5,028/oz and silver falling by 2.6% to $81.2/oz.

- For gold, a continuation lower would refocus attention on $4,661.0 initially, the Feb 3 low. On the upside, initial resistance is at $5,091.6, the Feb 4 high, followed by $5,139.9, a Fibonacci retracement level.

- For silver, a sharp sell-off last week confirms a resumption of the bear leg that started on Jan 29. The metal has traded through both the 20- and 50-day EMAs, signalling scope for a deeper retracement.

- Sights are on $61.136 next, a Fibonacci projection. Initial resistance is at 87.255, the 20-day EMA.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 11/02/2026 | 0900/1000 | * | Industrial Production | |

| 11/02/2026 | 1020/1120 | ECB's Cipollone In Digital Finance Conference Fireside Chat | ||

| 11/02/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 11/02/2026 | 1330/0830 | * | Building Permits | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | ** | Final CES Benchmark Revision | |

| 11/02/2026 | 1330/0830 | ** | Final CES Benchmark Revision | |

| 11/02/2026 | 1510/1010 | Kansas City Fed's Jeff Schmid | ||

| 11/02/2026 | 1515/1015 | Fed Vice Chair Michelle Bowman | ||

| 11/02/2026 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 11/02/2026 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 11/02/2026 | 1700/1800 | ECB's Schnabel Lecture At Austrian Academy of Sciences | ||

| 11/02/2026 | 1800/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 11/02/2026 | 1830/1330 | Bank of Canada meeting minutes | ||

| 11/02/2026 | 1900/1400 | ** | Treasury Budget | |

| 11/02/2026 | 2100/1600 | Cleveland Fed's Beth Hammack |