MNI ASIA MARKETS ANALYSIS

HIGHLIGHTS

- Treasuries took an early cue from overnight weakness in European and Japanese government bonds, which in turn was triggered by a combination of fiscal/ political/ supply factors.

- The USD index rose as much as 0.9% before stabilising and reversing a small portion of the gains following the ISM manufacturing data release.

- Rebound in Apple, Alphabet shares helped broader equity indexes bounce off session lows.

US TSYS

MNI US TSYS: Bear Steepening As Supply Weighs

The Treasury cash curve bear steepened in the return from the Labor Day weekend Tuesday, taking the lead of global peers and shrugging off soft US data.

- Treasuries took an early cue from overnight weakness in European and Japanese government bonds, which in turn was triggered by a combination of fiscal/ political/ supply factors.

- Europe (including UK) saw a record single day's issuance today per Bloomberg, just under EUR 50B. For good measure, Tuesday will have seen 58 investment-grade corporate bond offerings in the US, roughly $43.3B for a 2025 high (per Bloomberg) and narrowly exceeding last year's post-Labor Day sales.

- With UK and German 30Y yields hitting multi-year highs intraday, 30Y Tsys touched their highest levels since July 18 at a shade under the 5% mark (4.9966% session high).

- That move (around 830ET) would mark the intraday high for yields, with a smaller-than-expected improvement in the ISM Manufacturing index and continued weakness in construction spending (both out at 1000ET) helping keep a lid on yields through the rest of the session.

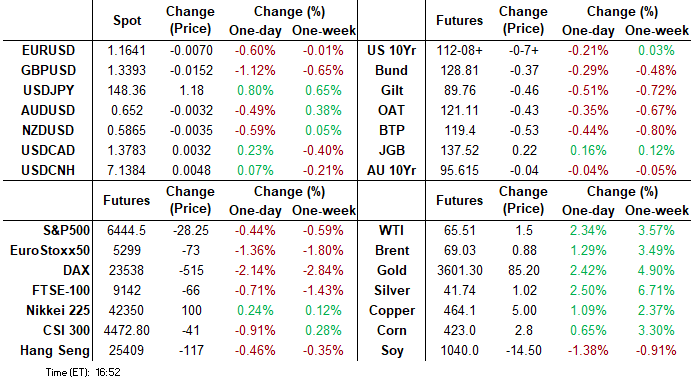

- Latest levels: The 2-Yr yield is up 3.1bps at 3.6474%, 5-Yr is up 3.8bps at 3.7339%, 10-Yr is up 4.5bps at 4.2731%, and 30-Yr is up 4.2bps at 4.9696%. Dec 10-Yr futures (TY) down 10/32 at 112-06 (L: 111-31 / H: 112-16)

- Friday's nonfarm payrolls report is the focus of the week. In the meantime, Wednesday's scheduled highlights include an appearance by St Louis Fed President Musalem (2025 FOMC voter, hawk), factory orders and JOLTS data, and the latest edition of the Fed's Beige Book.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.34% (+0.00), volume: $2.880T

- Broad General Collateral Rate (BGCR): 4.33% (+0.00), volume: $1.129T

- Tri-Party General Collateral Rate (TCR): 4.33% (+0.00), volume: $1.102T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $115B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $224B

FED Reverse Repo Operation

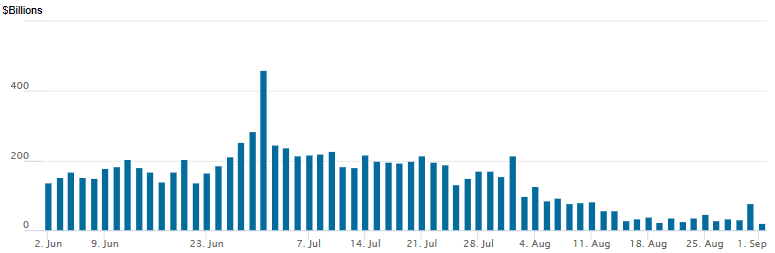

RRP usage retreats to lowest level since early April 2021 today: $21.066B with 17 counterparties this afternoon, from $77.898B last Friday. Compares to prior low of $22.344B on Tuesday, Aug 19 vs. this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options saw mixed flow upon the return from the extended holiday weekend, notable put selling in SOFR options as underlying futures traded weaker in the first half. Treasury futures pared losses slightly after ISM Mfg data. Projected rate cuts cool slightly vs. late Friday (*) levels: Sep'25 at -22.1bp (-22bp), Oct'25 at -35.4bp (-35.6bp), Dec'25 at -54.8bp (-56bp), Jan'26 at -65.9bp (-68.6bp).

SOFR Options:

-7,500 SFRV5 95.81/96.00/96.18 put flys, 5.0 ref 96.21

-3,000 SFRH6 96.12/96.00 put spds, 3.0

+10,000 SFRZ5 96.18/96.43 1x2 call spds 1.75 ref 96.215

15,000 SFRU5 95.93/96.06 call spds ref 95.9025

-10,000 SFRX5 96.06 put vs. 96.25/96.43 call spds, 0.0 net ref

3,800 SFRV5 96.25/96.37/96.50 call flys ref 96.215

2,100 SFRX5 95.93/96.06/96.18 put flys

5,500 SFRU5 95.81 puts ref 95.9025

2,000 0QV5 96.50 puts ref 96.98

2,00 0QH6 96.62/96.75/96.75 put trees ref 97.01

Treasury Options:

+6,400 TYX115/116 call spds, 5

3,000 FVX5 108.25/108.5/108.75/109 put condors ref 109-08.75

10,000 TYV5 108/109 put spds

3,200 USX5 106/111 put spds ref 113-21

2,500 TYV5 110.25/110.5/111.25 broken put flys ref 112-08.5

-8,000 TYV5 112 straddles, 118-117

5,000 FVV5 109 puts ref 109-08

5,000 TYV5 113 calls ref 112-12

4,450 TUV5 103.87 puts, 3 ref 104-08

MNI BONDS: EGBs-GILTS CASH CLOSE: Fiscal Concerns Apply Bear Steepening Pressure

European long-end instruments remained under pressure Tuesday.

- Fiscal and political concerns were at the forefront globally, starting with Japan overnight pushing long-end JGB yields up, a move that spilled over into European morning trade. Gilts underperformed amid continued UK fiscal uncertainty, which also saw GBP underperform peers.

- Supply was a constant pressure as well. with Bloomberg noting a record one-day corporate/govvy supply total of just under E50B, including UK and Italian sovereign syndications.

- ECB talk was plentiful: Schnabel noted upside inflation risks from tariffs and Muller reiterated his previous patient stance, while Villeroy said that inflation allowed for "favourable" interest rates and Simkus suggested a rate cut toward the end of year is plausible.

- European data was less impactful, with Eurozone flash August inflation slightly above-expected. Somewhat weak US ISM Manufacturing data helped global FI recover from its weakest levels of the day, however.

- The UK and German curves bear steepened. Multiple landmarks were reached, with a 14-year / 27-year highs reached in 30Y German / UK yields, respectively.

- Periphery/semi-core EGB spreads widened, with Portugal outperforming after Friday's ratings upgrade from S&P.

- Wednesday brings BOE TSC testimony, along with August final PMIs.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.9bps at 1.974%, 5-Yr is up 3.4bps at 2.313%, 10-Yr is up 3.8bps at 2.786%, and 30-Yr is up 4.6bps at 3.406%.

- UK: The 2-Yr yield is up 1.7bps at 3.982%, 5-Yr is up 3.9bps at 4.171%, 10-Yr is up 5bps at 4.8%, and 30-Yr is up 5.3bps at 5.693%.

- Italian BTP spread up 2.9bps at 89bps / Portuguese PGB up 0.4bps at 44.8bps

MNI EGB OPTIONS: Euribor Call Spread Buying Continues

Tuesday's Europe rates/bonds options flow included:

- DUV5 107.20/107.10/106.90p ladder, sold at 3 in 4k

- DUX5 107.50c, bought for 5 in 3k

- ERH6 98.12/98.25/98.4375/98.5625c condor, bought for 3.25 in 5k

- ERM6 98.31/98.43cs, bought for 2.5 in 10k (40k all week)

- SFIU6 97.40/97.50cs, bought for 0.75 in 20k

MNI FOREX: USD Off Best Levels Following ISM Manufacturing, GBP Weakness Stands Out

- Tuesday’s session was characterised by a sharp move higher for the US dollar across the European morning. Acute pressure on the longer-end of the UK, US and European yield curves drove risk-off sentiment, echoed by weakness for the major equity benchmarks. The USD index rose as much as 0.9% before stabilising and reversing a small portion of the gains following the ISM manufacturing data release.

- August's ISM Manufacturing report was weaker than expected on the headline figure, with some sub-components telling a slightly more mixed story, and price pressures unexpectedly diminished. This may have led participants to question the outright bullish dollar bias from earlier in the day, especially ahead of the crucial US labour market report on Friday.

- GBP weakness has been most notable Tuesday, with cable remaining 1.2% lower as a window-dressing UK reshuffle (not expected to resolve Starmer's popularity crisis in the near-term) was looked at unfavourably by investors. Cable had a punchy 208 pip range, printing a near 4-week low of 1.3341. Immediate focus will be on trendline support, drawn from the years lows. This level intersects around the 1.33 handle. Below here, 1.3249 is another notable chart level, the 76.4% retracement of the Aug 1 - 14 bull leg.

- Today’s EURGBP price action has resulted in a breach of resistance at 0.8674, the Aug 25 and 29 high. The break signals a stronger reversal and suggests scope for climb towards 0.8744, the Aug 7 high. Key resistance and the bull trigger is at 0.8769, the Jul 28 high. A break of this level would place the cross at the highest level since May 2023.

- The dynamic of widening yield differentials and heightened political uncertainty in Japan underpinned an impressive USDJPY rally to highs of 148.94 ahead of the US data. Fibonacci resistance at 149.12 has held for now, with the late reversal taking the pair back to 148.30 ahead of the APAC crossover.

- Australian Q2 GDP headlines the calendar on Wednesday, before final Eurozone services PMIs and US JOLTS data.

MNI OPTIONS: Expiries for Sep03 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1455(E2.2bln), $1.1525(E919mln), $1.1575-95(E1.5bln), $1.1600(E825mln), $1.1645-50(E792mln), $1.1675-80(E1.1bln), $1.1700(E1.1bln)

- USD/JPY: Y145.00($865mln), Y145.50($976mln), Y146.50($1.4bln), Y147.15-30($1.6bln), Y148.00($595mln), Y149.00($508mln)

- GBP/USD: $1.3500(Gbp507mln)

- AUD/USD: $0.6475(A$570mln)

MNI EQUITY TECHS: E-MINI S&P: (U5) Retracement Mode

- RES 4: 6600.00 Round number resistance

- RES 3: 6590.30 2.0% 10-dma envelope

- RES 2: 6543.75 2.00 proj of the Apr 7 - 10 - 21 price swing

- RES 1: 6523.00 High Aug 28 and the bull trigger

- PRICE: 6385.50 @ 1220 ET Sep 2

- SUP 1: 6371.75 Intraday low

- SUP 2: 6332.30 50-day EMA

- SUP 3: 6313.25 Low Aug 6

- SUP 4: 6239.50 Low Aug 1 and a key support

A bull cycle in S&P E-Minis remains intact and the latest pullback is - considered corrective. Price has traded through the 20-day EMA, at 6439.95. The key support to watch lies at the 50-day EMA, at 6332.30. A clear break of this EMA is required to signal scope for a deeper retracement. This would open 6239.50, the Aug 1 low and also a key support. Moving average studies still highlight a dominant uptrend. The bull trigger is 6523.00, the Aug 28 high.

MNI COMMODITIES: Crude Rises, Gold Hits Fresh Record High

- Crude has seen support today from continued Russian supply fears, recent strikes on energy infrastructure, and oil product strength, offsetting pressure from a stronger dollar.

- WTI Oct 25 is up by 2.5% at $65.6/bbl.

- Recent Ukrainian drone attacks shut down facilities accounting for at least 17% of Russia's oil processing capacity, or 1.1mn bpd, according to Reuters' calculations.

- OPEC+ will hold a meeting this weekend to decide on output for October.

- Despite today’s move, a bear cycle in WTI futures remains intact and recent gains are considered corrective.

- Initial resistance to watch is $66.56, the Aug 4 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A resumption of weakness would pave the way for a move towards $57.71, the May 30 low.

- Meanwhile, spot gold has also rallied by 1.5% to $3,529/oz, taking the yellow metal to a fresh all-time high.

- UBS said that investors are adding to gold allocations as Fed rate cuts loom, and they see gold making new highs in the coming quarters.

- Today’s gains in gold have resulted in a breach of key resistance at $3,500.1, the Apr 22 high, confirming a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows.

- The next objective is $3,547.9, a Fibonacci projection.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 03/09/2025 | 0700/0300 | * | Turkey CPI | |

| 03/09/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0730/0930 | ECB Lagarde Speaks at ESRB Conference | ||

| 03/09/2025 | 0730/0830 | BOE Mann at Signum's London Westminster Day roundtable | ||

| 03/09/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0815/0915 | BOE Breeden at Innovation in Money and Payments Conference | ||

| 03/09/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 03/09/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 03/09/2025 | 0900/1100 | ** | EZ PPI | |

| 03/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 03/09/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 03/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 03/09/2025 | 1300/0900 | St. Louis Fed's Alberto Musalem | ||

| 03/09/2025 | 1315/1415 | BOE testify at TSC: Bailey, Greene, Lombardelli, Taylor | ||

| 03/09/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/09/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 03/09/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 03/09/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/09/2025 | 1730/1330 | Minneapolis Fed's Neel Kashkari | ||

| 03/09/2025 | 1800/1400 | Fed Beige Book | ||

| 04/09/2025 | 0130/1130 | ** | Trade Balance |