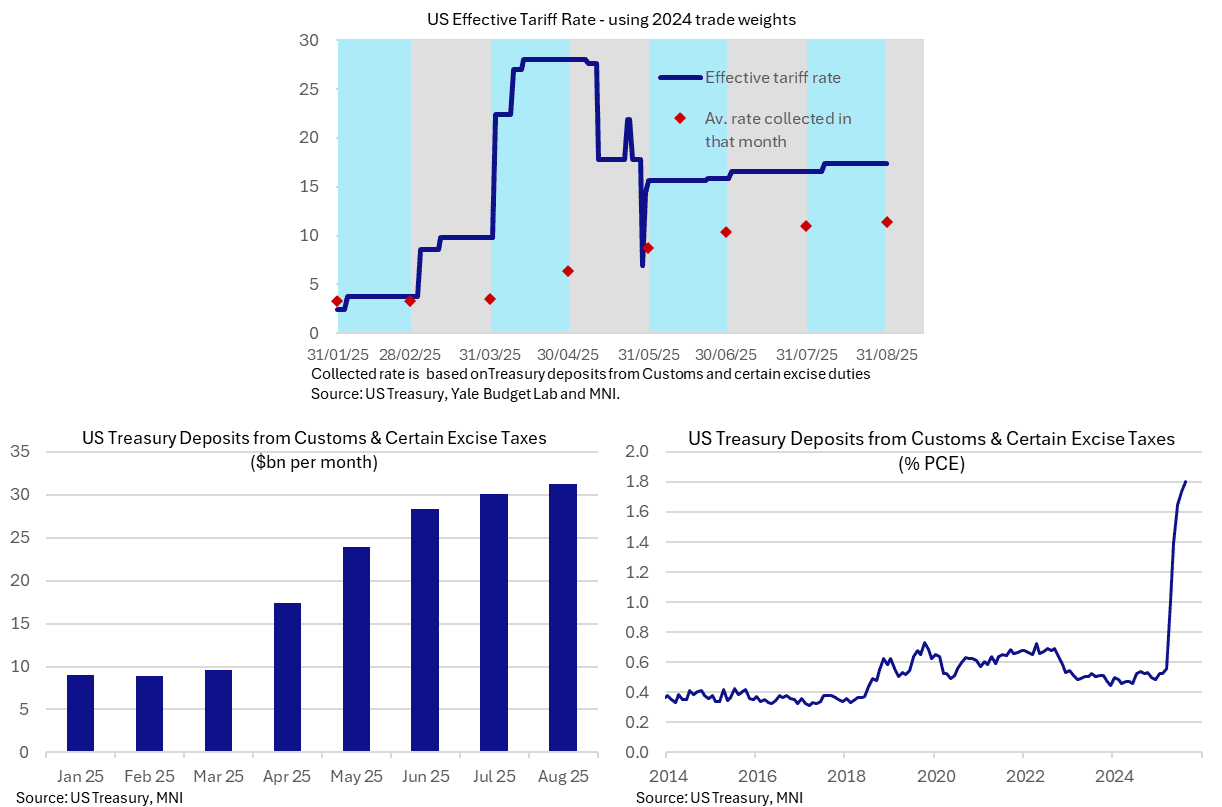

US OUTLOOK/OPINION: Mixed Implications For CPI Hit From Tariff Revenues

Core goods inflation is expected to accelerate a little further in August on a M/M basis and tariff revenues still point to further solid increases ahead, but the pace at which tariff revenues have been closing the gap with implied tariff rates has slowed in recent months.

- Monthly core goods CPI inflation is expected to accelerate in tomorrow’s August release, with analyst expectations averaging 0.3% M/M after two months at 0.2% M/M (including July’s undershooting of then expectations of a 0.4% increase).

- It comes as tariff-driven price increases are generally seen to be getting towards the largest for the year. There’s a rough consensus of a three-month lag from tariff implementation to more notable consumer price increases. That factors in the time taken for shipments, a front-loading of imports that built up inventories and points including importers using the automatic payment transfer system being able to delay their tariff payments for up to 1.5 months.

- On a similar note, the July Beige Book noted that “Contacts that plan to pass along tariff-related costs expect to do so within three months” whilst the August Beige Book, published Sep 3, noted that “Nearly all Districts noted tariff-related price increases, with contacts from many Districts reporting that tariffs were especially impactful on the prices of inputs.”

- Latest tariff revenue meanwhile suggests we’re still a little way off seeing the full impact from tariffs on prices. The effective tariff rate currently stands at 17.4% according to Yale Budget Lab calculations (pre-substitution, i.e. keeping trade shares constant) whereas the $31bn of Treasury deposits from customs and certain excise duties in August was worth 11-11.5% of goods imports depending on whether you take 2024 levels for a similar static approach or annualized July data.

- The speed at which the tariff collection rate is increasing has slowed notably in recent months, suggesting it could take a while for this gap to the effective rate to be closed. Indeed, the $31.3bn of tariff revenues is vs $30.1bn in July and $28.4bn in June, after larger increases from $24.0bn in May, $17.4bn in April and $9.6bn in March.

- Alternatively, whilst these tariff revenues are still on the small side compared to what effective rates might suggest, they were still worth a sizeable ~1.8% of overall personal consumption expenditure. That’s an increase of ~1.3pp under the Trump administration so far, but of course doesn’t give insight into burden sharing across importers, businesses and consumers.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

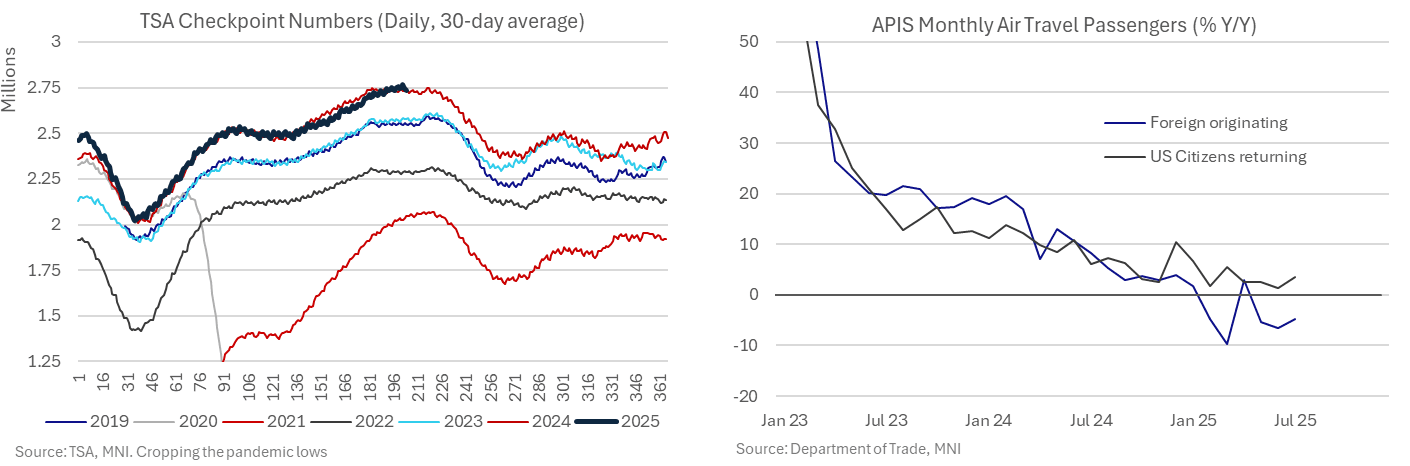

US OUTLOOK/OPINION: Travel CPI Categories Perhaps Less Sequentially Soft In July

[The below is a small section on latest travel demand in the US from the MNI US CPI Preview ahead of Tuesday's CPI report for July]

- Travel-related prices have been a source of generally larger than expected disinflationary pressure in recent months, although some travel data crudely suggest we might have seen the peak for this sequentially.

- TSA checkpoint numbers have returned closer to last year’s seasonal pattern after some weakness in prior months.

- APIS data meanwhile have stabilized at low Y/Y rates with US citizens returning rising 3.6% Y/Y in July (after 1.4% Y/Y in June or 3% Y/Y averaged since February) and foreign originating flights -4.9% Y/Y (after -6.6% Y/Y in June or -5% Y/Y since February).

EURJPY TECHS: Trend Structure Remains Bullish

- RES 4: 177.08 2.000 proj of the Feb 28 - Mar 18 - Apr 7 price swing

- RES 3: 175.43 High Jul 11 ‘24 and a key medium-term resistance

- RES 2: 174.86 1.764 proj of the Feb 28 - Mar 18 - Apr 7 price swing

- RES 1: 173.97 High Jul 28 and the bull trigger

- PRICE: 171.70 @ 15:31 BST Aug 11

- SUP 1: 169.73/45 Low Jul 31 / 23.6% of the Feb 28 - Jul 28 bull leg

- SUP 2: 169.62 50-day EMA

- SUP 3: 168.46 Low Jul 1

- SUP 4: 167.46 Low Jun 23

A bullish trend condition in EURJPY remains intact and for now the recent move down is considered corrective. Key support to watch lies at the 50-day EMA at 169.62. A clear break of the EMA is required to highlight a stronger short-term bearish threat. Moving average studies remain in a bull-mode position highlighting an uptrend. A break of the Jul 28 high of 173.97, would resume the bull cycle.

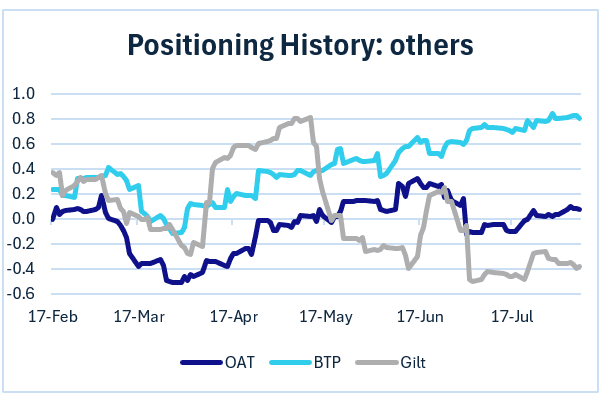

BONDS: Europe Pi: BTPs Stay Long, Gilts Short, OATs Flat (2/2)

Elsewhere in Europe Pi:

- OAT remains in flat territory, where it has been almost the entire year. Last week's trade was indicative of reduced longs.

- Gilt structural positioning remains in short territory. There were some longs set last week, however.

- BTP continues to edge further into "very long" territory. Indeed, trade indicative of further long-setting was seen in the most recent week.