FED: Minneapolis's Kashkari: Would Have Held Rates In Oct, Wait And See For Dec

Minneapolis Fed President Kashkari (a 2026 FOMC voter) has made a hawkish shift in his views on rates over the last couple of months, based on comments in a Bloomberg interview Thursday.

- He told Bloomberg that the data argued for a pause at the October FOMC meeting: “The anecdotal evidence and the data we got just implied to me underlying resilience in economic activity, more than I had expected".

- Since the October meeting, data point to "more of the same", and thus for the December FOMC, “I can make a case depending on how the data goes to cut, I can make a case to hold, and we’ll have to see.”

- This is definitely a more hawkish view for Kashkari vs an essay he wrote after September's meeting that he not only supported the cut at that meeting but also penciled in 25bp cuts in October and December.

- It also means the roster of 2026 rotating presidential voters sounds increasingly hawkish: it also includes Cleveland's Hammack (arguably the most hawkish on the Committee), Dallas's Logan (Philadelphia's Paulson appears to be more dovish-leaning.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Boston's Collins One Of 5 (of 12) Holdouts To Oct+Dec Cuts

As we noted earlier, Boston Fed President Collins (who votes in the next 2 meetings) is likely one of the 2 FOMC members who only saw 1 more cut this year in her September Dot Plot submission - she confirms it in Q&A: "a bit more easing, perhaps another 25 basis points of easing might be appropriate."

- And it sounds like she might support a cut in October, before seeing a pause thereafter: "having changed in September, if we were to make an additional change, I could also see scenarios where it would then be appropriate to hold over time."

- As such back-to-back October / December cuts look to be supported by 7 of 12 2025 FOMC members, with all four regional presidents eyeing either one or no more cuts. The core of the Committee including all on the Board except for Barr will support cuts though as it stands, and we think the bar is fairly high for the holdouts to dissent.

- Below is where we see the 19 end-2025 Fed funds rate dots:

FED: Boston's Collins Still Sees "A Bit" More Easing This Year

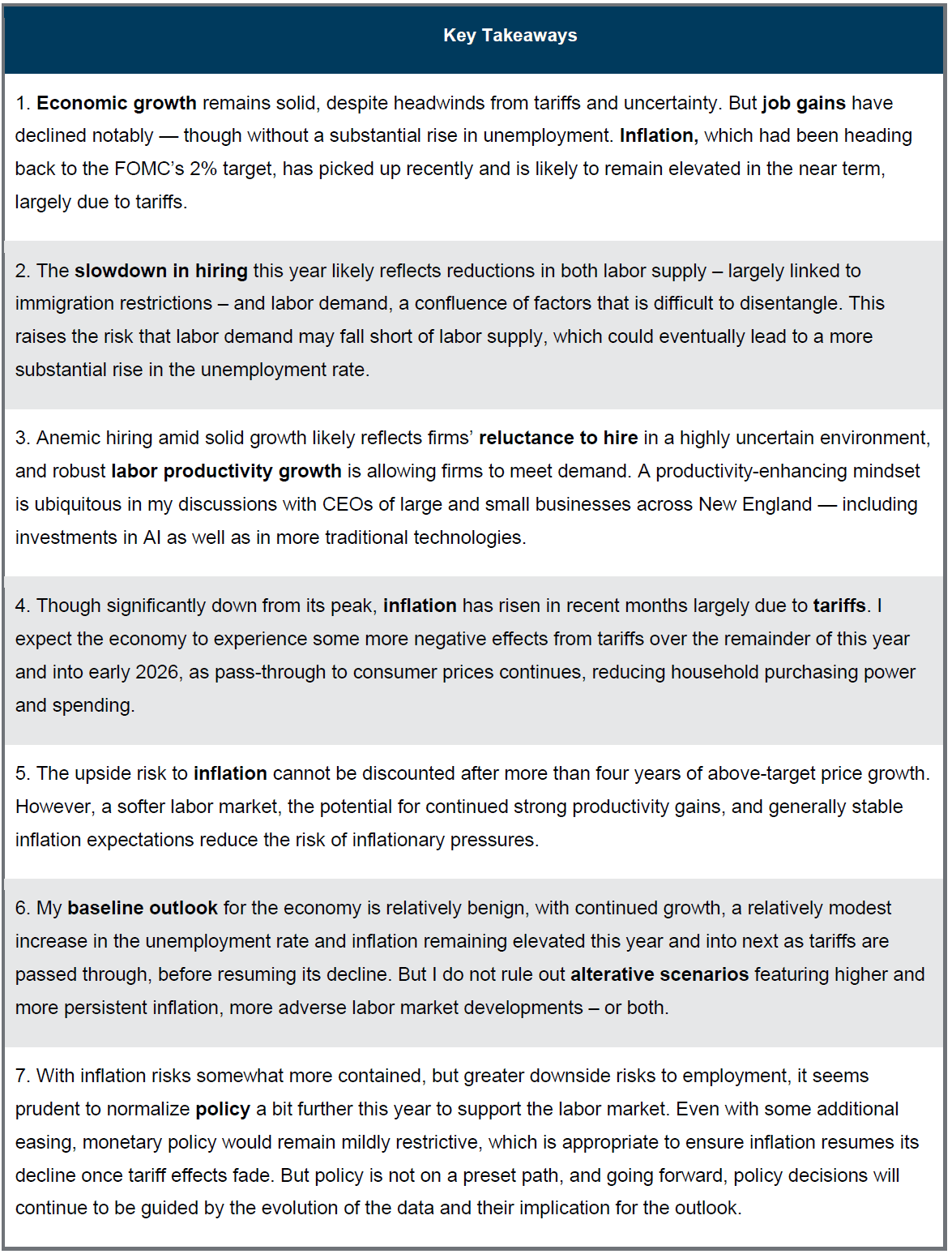

The key takeaways from Boston Fed President Collins's (2025 FOMC voter) speech on "Assessing The Balance Of Risks In The Economy" Tuesday (link) are in the image below, very similar to her speech on September 29 but with greater depth to her arguments.

- We still peg Collins as a "one more cut" submission in the September SEP, though there is an argument she is one of the median 9 (of 19 members) who sees 2 more cuts. In particular, she again notes scope for normalizing policy "a bit further" this year; having previously described the September 25bp cut as "a bit of easing", it would stand to reason she is referring to 25bp moves in both instances. Additionally she says she could envisage a scenario where no further cuts this year are warranted.

- The key passage on monetary policy: "with inflation risks somewhat more contained, but greater downside risks to employment, it seems prudent to normalize policy a bit further this year to support the labor market. Importantly, even with some additional easing, monetary policy would remain mildly restrictive, which is appropriate for ensuring that inflation resumes its decline once tariff effects filter through the economy. But policy is not on a pre-set path, and I can envision scenarios where appropriate policy calls for holding rates steady later this year and into next, as we assess effects of the recent policy actions and get more information. Going forward, my policy decisions will continue to be guided by my best assessment of all available data, their implications for the outlook, and the evolving risks."

- Similar to her previous appearance, Collins says Tuesday "While I see inflation risks as somewhat more contained than I previously thought, downside risks to the labor market have likely risen."

- She again highlights the slower growth in both labor supply and demand, pointing to a 40k "breakeven" rate of payrolls growth. She says however that the "broad-based slowdown in hiring raises the risk that labor demand may fall short of supply, which could eventually lead to a more substantial increase in the unemployment rate than we have seen so far this year."

- She notes "a few reasons to expect further price pressures from tariffs going forward", while "Overall, my baseline economic outlook is relatively benign. I see continued growth in activity, little further rise in the unemployment rate, and inflation remaining elevated this year and into early 2026 as tariffs are passed through more fully, before resuming its decline".

- "while that is my baseline view, I do not rule out scenarios featuring higher and more persistent inflation, more adverse labor market developments, or both."

- She sees inflation expectations as "relatively stable". And "a softer labor market with strong productivity growth reduces the risk of inflationary pressures from wage growth." "But all of this warrants careful attention, and a lack of comprehensive price data (given the government shutdown) will complicate assessing the inflation environment."

USDCAD TECHS: Bullish Trend Structure

- RES 4: 1.4200 Round number resistance

- RES 3: 1.4167 50.0% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.4111 High Apr 10

- RES 1: 1.4080 Intraday high

- PRICE: 1.4042 @ 17:20 BST Oct 14

- SUP 1: 1.3928/3863 20- and 50-day EMA values

- SUP 2: 1.3799 Bull channel base drawn from the Jul 23 low

- SUP 3: 1.3727 Low Aug 29 and a bear trigger

- SUP 4: 1.3689 Low Jul 28

A bull cycle in USDCAD remains intact and this week’s firm start reinforces current conditions. Last Thursday’s rally confirmed a recent bull flag on the daily chart and a resumption of the current uptrend. MA studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 1.4111 next, the Apr 10 high, and further out scope is seen for an extension towards 1.4167, a Fibonacci retracement. First key support is 1.3863, 50-day EMA.