FED: Minneapolis's Kashkari: 2 More Cuts In 2025, But Longer-Run Dot Rising

Sep-19 12:50

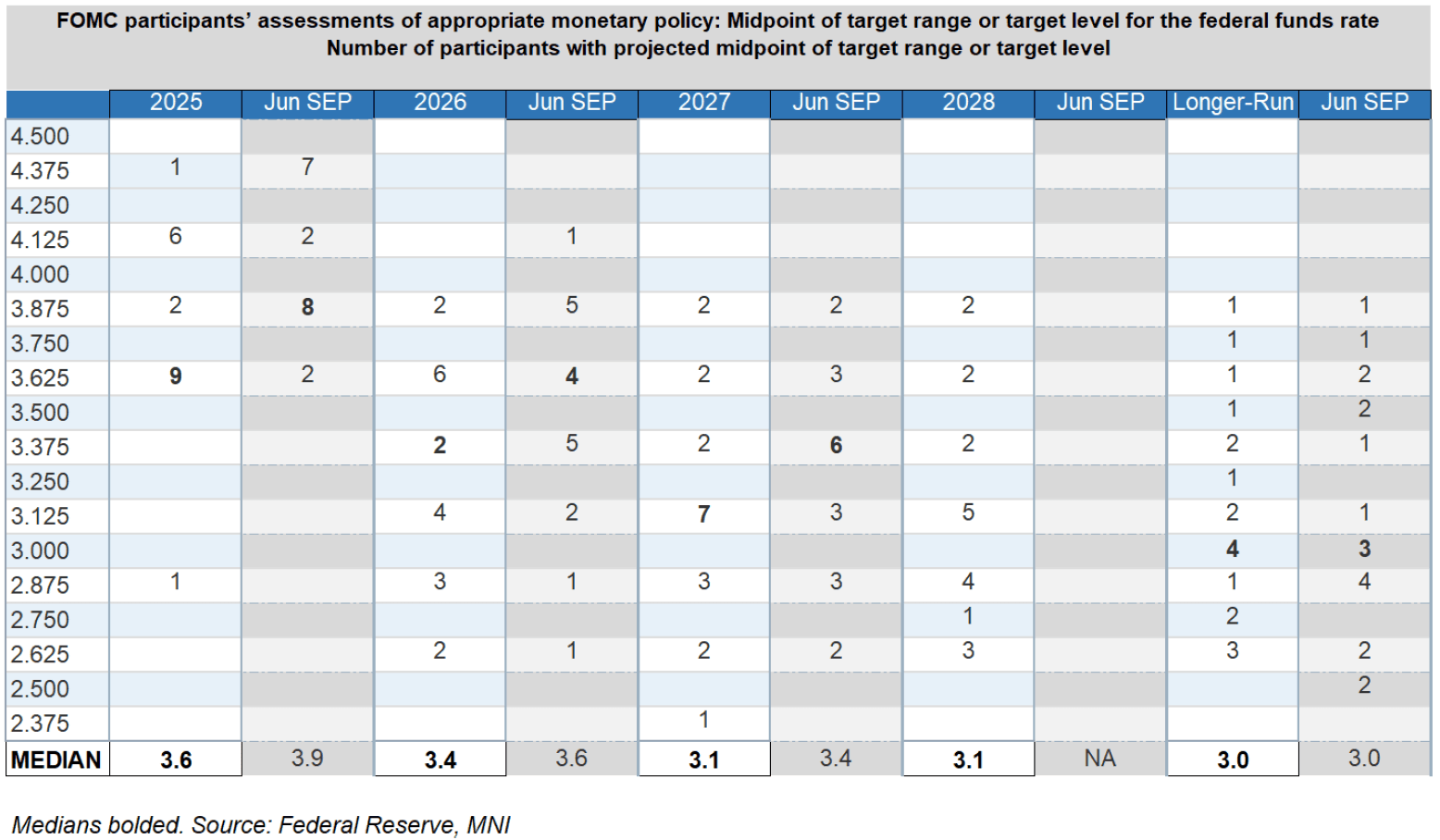

Minneapolis Fed President Kashkari (leans dovish, 2026 FOMC voter) wrote in an essay out Friday ("Three Questions" - link) that he not only supported the FOMC's 25bp cut at the September meeting, but he also penciled in a further two more through year-end, in line with the new Dot Plot median. That implies he would support cuts in October and December, representing one more cut than he had envisaged in his June Dot Plot submission for end-2025.

- In short, "I believe the risk of a sharp increase in unemployment warrants the committee taking some action to support the labor market", basically echoing September's Statement and Chair Powell's message at the press conference.

- Kashkari's essay points out that longer-run inflation expectations haven't de-anchored, and that it's possible to reconcile the stronger performance of financial markets alongside weaker labor conditions. Overall though: "For me the more likely risk is a rapid further weakening of the labor market. We know from past economic cycles that when labor markets weaken, they can weaken quickly and non-linearly." He underlines his staff's estimate that "lower immigration can only explain one-third to at most one-half of the observed decline in job creation", suggesting weaker demand for labor, and not just weaker supply, is the driving force of softer NFPs.

- And on inflation, "unless there is some large increase in tariff rates from here or some other supply side shock, it is hard for me to see inflation climbing much higher than 3 percent given announced tariff rates and the relatively small share of imported goods in overall U.S. consumption."

- Later Friday morning in a CNBC interview he said "it's somewhat of a fragile labor market, is how I would look at it. And so I think the cut that we did this week, and that the cuts that we could do for the balance of this year, I look at them more as insurance to just keep the labor market from falling dramatically while it takes time for the underlying inflationary dynamics to play out over the course of the next year or so. So I think it's a it's not a bad labor market, but it's one that I think we need to pay a lot of attention to."

- It's not clear he would support many cuts in 2026 at this stage. He was one of the participants who raised their longer-run dots at the latest meeting - his went up 25bp to 3.125%. "Over the past few years, I have continued to increase my assessment of the neutral rate of interest. The implication of this reassessment is that monetary policy has likely not been as tight as I previously understood." He could be one of the 4 members that see policy reaching that level at end-2026, implying he has penciled in 2 more cuts to that point. (One signal he points to in his essay for a rising neutral rate is continued elevation in 10Y TIPS yields, which have moved sideways as the Fed has cut 100bp).

- It's not totally clear (in part because of a change in members since the June meeting) but the number of longer-run dots at 3.125% went from 1 to 2, while it appears his view that the median is higher than 2.875% was shared by at least a couple of colleagues. The longer-run rate median has remained at 3.00% since March but would only take 1 of the 10 members at 3.00% or below moving above 3.00% to raise the median, something that looks likely to happen as soon as December.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB SYNDICATION: Finland New 7-year Apr-32 RFGB: Priced

Aug-20 12:42

- Re-offer: 99.254 to yield 2.751%

From market source

More details to follow - Spread set earlier at MS + 29bp (guidance was MS + 31bps area)

- Size: E4bln (MNI expected E3bln but noted upsizing to E4bln was possible)

- Books in excess of E33bln (inc E2.25bln JLM interest)

- Maturity: 15 April 2032

- Coupon: 2.625%. Short first

- Settlement: 28 August 2025 (T+6)

- Hedge ratio: 110% vs 0% Feb-32 Bund. Spot ref: 85.71 / +34.5bp

- ISIN: FI4000591862

- Bookrunners: Barclays (DM/B&D) / Bofa Securities / Danske Bank / Deutsche Bank / J.P. Morgan

- Timing: TOE 13:29BST / 14:29CET. FTT immediately

From market source / MNI colour

PIPELINE: Corporate Bond Roundup: $3B British Columbia 5Y SOFR Launched

Aug-20 12:38

- Date $MM Issuer (Priced *, Launch #)

- 08/20 $3B #ADB 5Y SOFR+39

- 08/20 $3B #British Colombia 5Y SOFR+53 (books were over $8.7B)

- 08/20 $1B Nordic Investment Bank WNG 3Y SOFR+34

- 08/20 $Benchmark Nordea Bank 5Y +75a, 5Y SOFR

- 08/20 $Benchmark Athene Global 10Y +150a

- $15.9B Priced Tuesday

EURIBOR OPTIONS: Midcurve Call Spread

Aug-20 12:36

0RX5 98.25/98.375cs, bought for 2 in 4k.