EM ASIA CREDIT: Mineral Resources: Sells lithium stake

(MINAU, Ba3-neg/NR/BB-neg)

"*MINRES GAINS 11% AFTER SELLING STAKE IN LITHIUM OPS TO POSCO" - BBG

MinRes monetises lithium assets, will reduce debt, positive for credit.

MinRes has sold a 30% stake in a newly incorporated joint venture, housing its existing 50% ownership of the Wodgina and Mt Marion lithium mines, to Korea’s Posco Holdings for USD 765m (c. AUD1.2bn). This values MinRes’s lithium holdings at USD3.9bn. The proceeds, upon completion (expected 1H26 pending regulatory approvals), will be used to repay external debt and strengthen the balance sheet. Supportive for valuations.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

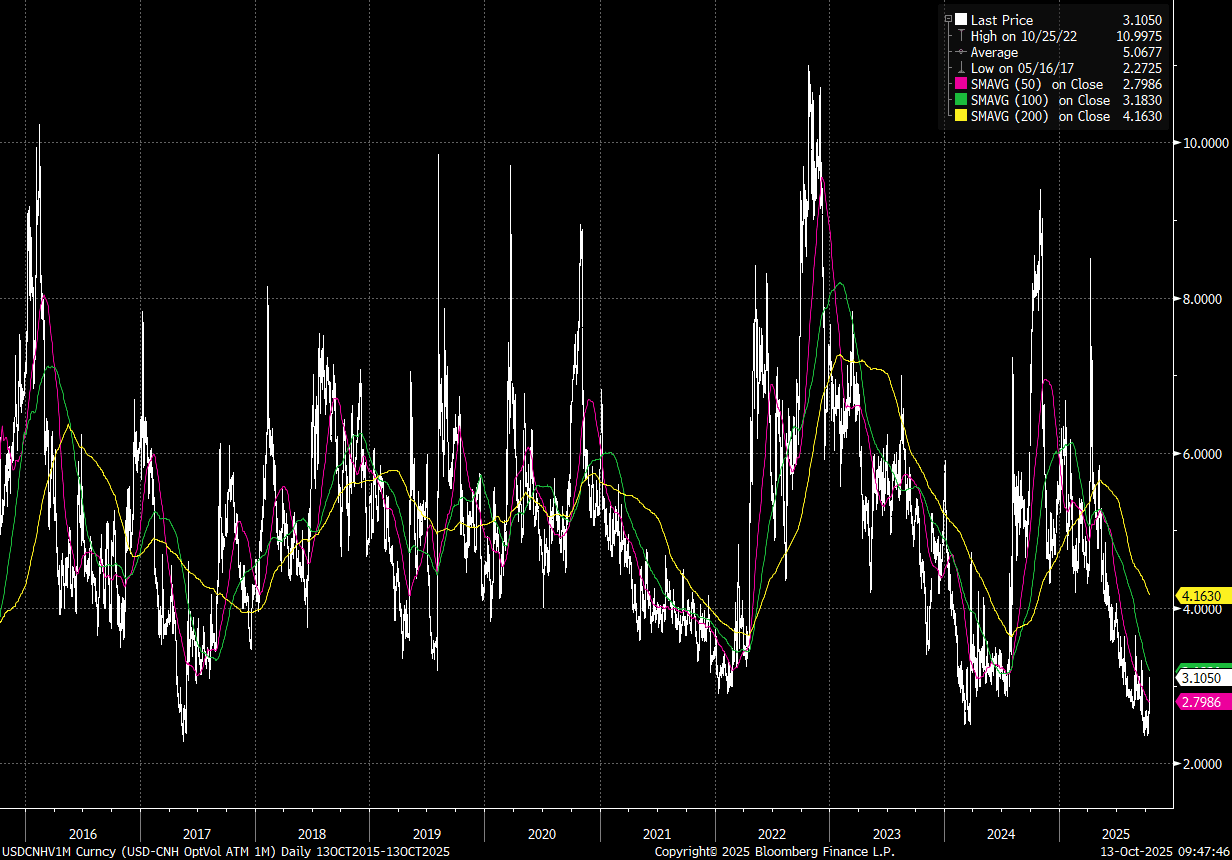

CNH: Implied Vols Still Low By Historical Standards, USD/CNH Under Key EMAs

USD/CNH tracks near 7.1410 in latest dealings, around slightly from end Friday levels. Even with the 100% tariff threat from US President Trump on Friday (to be implemented on Nov 1), USD/CNH couldn't get above 7.1500. Note the 50-day EMA is at 7.1450, so close by, while the 100-day is higher near 7.1660. For now resistance is around the 7.1500 region. On the downside, recent lows rest at 7.1240.

- Remarks by both the US President and Vice President over the weekend appeared to soften the US rhetoric and leave the door open for negotiations. In remarks this morning Trump noted: “You know for me, you know what November 1 is? It’s an eternity. November 1 is an eternity for me.”(via BBG).

- Per Polymarket, odds of a 100% tariff rate being imposed are around 15% this morning, well off earlier highs above 50% (when this market first started trading).

- For USD/CNH, eyes will be on the USD/CNY fix to gauge China's response, although the broader sense is that recent ranges for USD/CNH will continue to prevail. 1 month implied USD/CNH vol is higher, last near 3.10%, but from an historical standpoint is still very low (see the chart below). The 1 month risk reversal is higher as well, but well off earlier 2025 highs, last at -0.2050. The market may also feel other markets, like equities, may be better expressions of renewed US-China trade tensions.

- China's response to higher tariff levels is likely to be after that fact, i.e. signal comfort around weaker yuan levels after the US imposes higher tariff rates, rather than before. A sharp weaker yuan ahead of the Nov 1 deadline may disrupt US-China negotiations.

- On the data front today we have China Sep trade figures.

Fig 1: USD/CNH 1mth Implied Vol Firmer, But Still Low From An Historical Standpoint

Source: Bloomberg Finance L.P./MNI

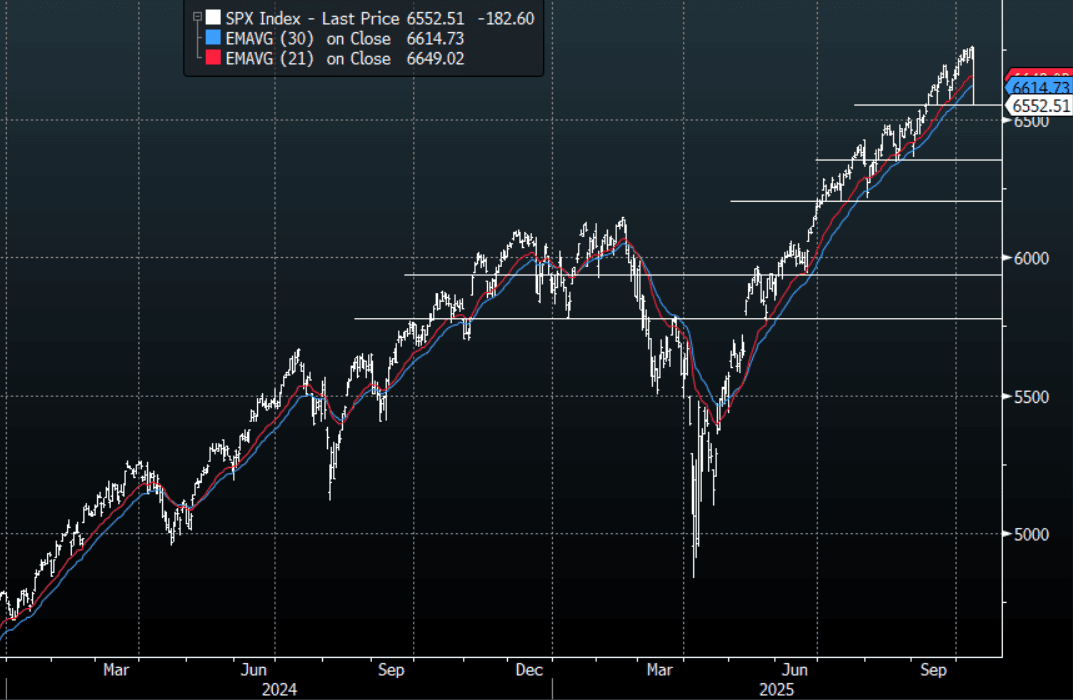

US STOCKS: S&P(ESZ5)- Gaps Higher On The Open On Attempts To Calm Market Worries

The S&P(ESZ5) overnight range was 6540.25 - 6806.50, SPX closed -2.71%, Asia is currently trading around 6665. The E-Mini’s have gapped higher on the open as the US attempts to lower the temperature and looks to set a more conciliatory tone as China played down the impact of its new controls, E-minis(S&P) +1.05%, NQZ5 +1.50%. The stock market looks to have put in a short-term top for now, we might see further retracement from Fridays lows around the 6500/6550 support as the market tries to latch onto anything positive. I feel that the damage done to leveraged accounts on Friday would make it difficult for the market to just move on from this and start making new all-time highs again. Personally I see very little chance of China changing its stance so I suspect those still very overweight will probably use any bounce to just lighten up positioning. Levels back toward 6700 and above are likely to be faded first up.

- Rush Doshi believes China will not back down on X, but they are at pains to stress the move is not a ban: “1 They're worried about the global reaction to their moves. So they stressed (twice) verbatim that these export control measures on rare earths are not prohibitions/bans. 2 They do not want to withdraw the controls. They also stressed these controls are their sovereign right. 3 They haven't announced a response to Trump's threats. They say only the boilerplate "they do not want to fight, but aren't afraid of fighting." Suggests they may not want to see further escalation.”

- “Bottom Line: Trump wants this regime withdrawn. Beijing won't do that, but is trying to reassure it won't implement it punitively. Obviously, that is not a credible promise on Beijing's part, and US and PRC positions are at odds.”

Fig 1: S&P 500 Index Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

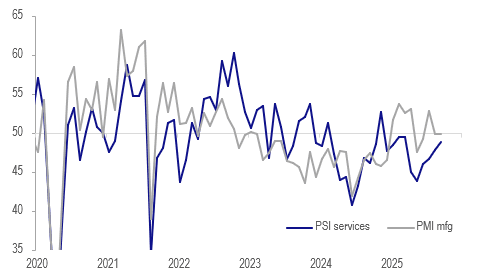

NEW ZEALAND: Services & Manufacturing Indices Signal Ongoing Weak Q3 Activity

The BNZ services and manufacturing PMIs for September were consistent with the RBNZ’s assessment in its October statement that “economic activity recovered modestly in the September quarter”. The manufacturing sector stagnated in August/September, while services continued to contract but at a slower rate with September up one point to 48.8, highest since March. Continued weak activity, including employment, at the end of the quarter is consistent with further RBNZ easing with policy likely to become stimulatory.

- The Q3 averages of the PMI and PSI show that there was some improvement in the quarter compared to Q2. Manufacturing rose 1 point to 50.9, slight growth, and services almost 3 points to 47.7, ongoing contraction.

- Forward-looking services orders rose to 51.4 from 47.8, the highest since November 2024. They continued to contract in Q3 overall at 48.6 but at a slower pace than Q2’s 45.5. Manufacturing saw an increase in orders in Q3 at 53.1 up from 49.5.

- Labour demand remained soft consistent with other data signaling a weak Q3 print on 5 November. September services employment fell to 47.8 from 48.7 with Q3 showing a further contraction in staffing at 47.6 (Q2 46.4). Manufacturing employment contracted too in the quarter.

NZ BNZ services vs manufacturing indices

Source: MNI - Market News/LSEG