GOLD: Middle East Deal & Profit Taking See Gold Test $4000, Fed’s Powell Later

Gold prices have stabilised today driven by profit taking after they rose 4.7% in the month to 8 October and reached a record of $4059.31/oz. They are down 0.2% to $4034.3 in Thursday’s APAC trading as geopolitical risks in the Middle East eased with the announcement of a Gaza ceasefire deal which is due to take effect from midday Thursday local time. Bullion fell towards $4000 on the news reaching a low of $4001.44. As was the case on Wednesday, gold has traded against its usual correlation with the US dollar lower (BBDXY -0.2%) and yields little changed.

- Bullion will continue to monitor developments in French politics, the US government shutdown and policy changes in Japan under new LDP leader Takaichi. Gauging the Fed outlook has also become more difficult with data delayed due to the shutdown but another cut is expected in October.

- Silver is outperforming rising 0.2% to $48.97 but has been in a narrow range of $48.409 to $49.128. It has benefited from safe-haven flows but also a tight physical market.

- Later Fed Chair Powell speaks as well as Bowman, Goolsbee, Barr and Kashkari, and the ECB’s Lane and BoE’s Mann. The ECB’s September meeting accounts are published and the Eurogroup meeting is also being held. In terms of data, German August trade prints.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Yields Up From Earlier Lows, Q2Data Points To Weak GDP

NZGB benchmark yields are up from earlier lows. The 2yr yield is now up close to 2bps, tracking back towards 2.95%. The 10yr NZGB yield is around 4.31%, still off 1.5bps. Both benchmarks remain close to recent lows. US Tsy yields have drifted a touch higher, led by the front end, which may have spilled over to NZ at the margins.

- The NZ 2/10s curve remains flatter last near +136.5bps. The NZ 2yr swap rate has edged up to 2.735%, against earlier lows near 2.705%, so mirroring the movement in NZGB front end yields.

- On the data front, Q2 NZ business sales values rose 2.1% q/q with profits up 4.2%. Salaries and wages rose only 1.2% q/q. Manufacturing volumes fell 2.9% q/q after rising 2.4%. Q2 GDP is released on September 18 and the RBNZ is forecasting it to fall 0.3% q/q. Data has shown weak building, goods exports and manufacturing volumes. The RBNZ is expected to cut rates at its October and November meetings.

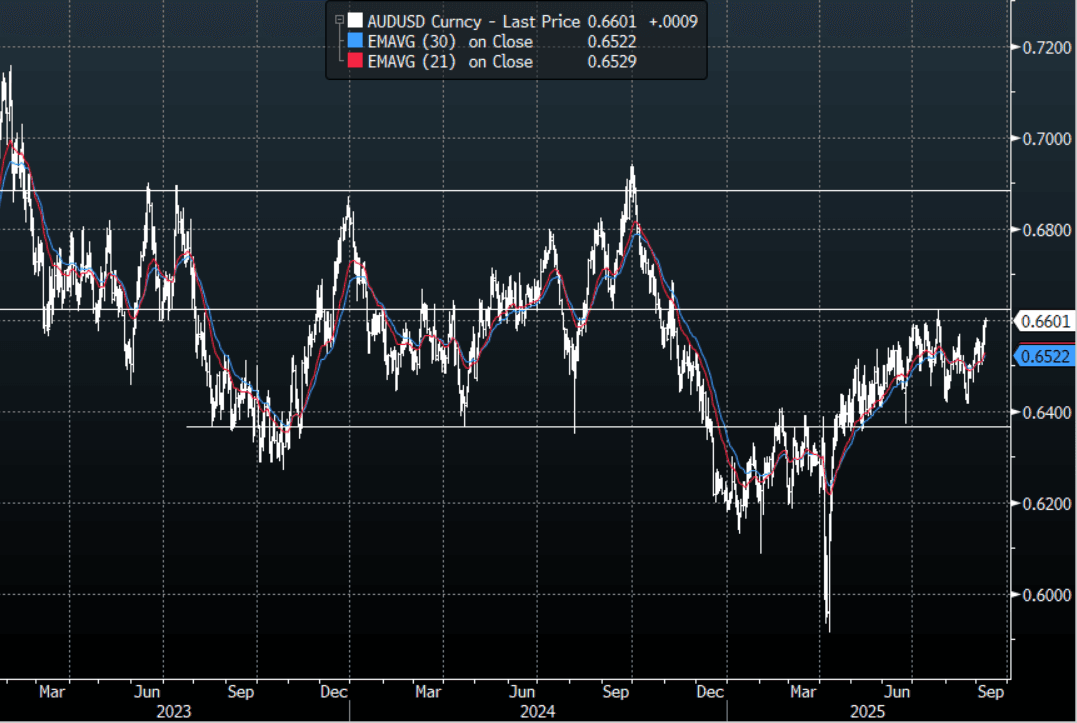

AUD: Asia Wrap - AUD/USD Probes Above 0.6600

The AUD/USD has had a range of 0.6588 - 0.6604 in the Asia- Pac session, it is currently trading around 0.6600, +0.12%. US rates extended lower again and the USD traded soft, the headwinds for the USD seem to be compounding which points to a potential look below its support. The AUD has drifted higher and is looking to test the top-end of its recent range. The AUD remains in its recent multi-month range of 0.6350-0.6650, should the USD break and extend lower we could potentially see the AUD break back above 0.6650. Should this occur it could provide the upward momentum to target levels back towards 0.6900/0.7000. Although still in the range the bias is for dips back to 0.6500 to be supported now.

- Growth Recovery Continued In Q3, August Costs/Prices Moderated. August NAB business confidence fell to +4 from +8 but conditions improved to +7 from +5. Both have improved in Q3 to date by around 3 points signaling that GDP growth should continue to recover. The price/cost components were lower in August with purchase cost and retail price increases at multi-year lows, which should reassure the RBA. However, the Q3 average of final product prices is still around where it was in H1 signaling some stabilisation in disinflation. Labour demand also appears to have steadied.

- Consumer Sentiment Weaker But Series Is Volatile: Westpac consumer sentiment fell 3.1% m/m to 95.4 in September after August’s robust +5.7% m/m to 98.5. It remains in pessimistic territory but above the 2025 average helped by 75bp of monetary easing and lower inflation.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6515(AUD429m), 0.6600(AUD420m). Upcoming Close Strikes : 0.6550(AUD777m Sept 10) - BBG

- CFTC Data last week shows Asset managers reduced their shorts for the first time in a while -66025(Last -78758), the Leveraged community though look to be rebuilding their own shorts after winding them down -11860(Last -6447).

- AUD/JPY - Asia-Pac range 97.12 - 97.28, Asia is trading around 97.20. The pair topped out towards 97.50 but has held onto most of its gains on the gap higher yesterday unlike USD/JPY. A sustained break above 97.50/98.00 is needed to reignite the upward trend.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

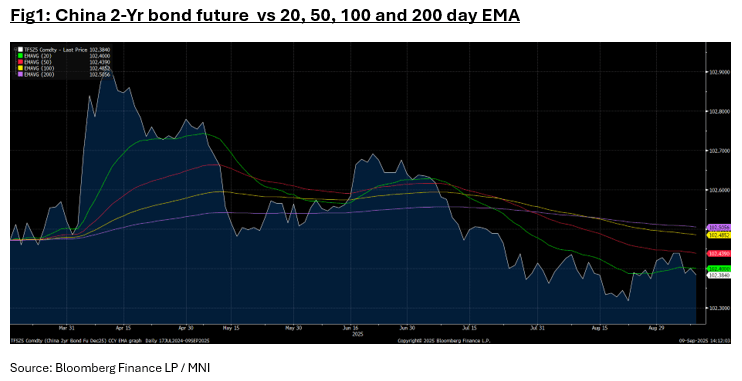

CHINA: Bond Futures Fall Tuesday

- China's major bond futures are all lower today for a third consecutive day of falls.

- The 10-Yr is lower by -0.05 at 107.790 to move further below all major moving averages.

- The 2-Yr is lower by -0.01 at 102.38 to move away from the 20-day EMA of 102.38.

- Government bond yields are marginally lower with the CGB 10-Yr at 1.78%.