US STOCKS: Midday Equities Roundup: Risk-Off Unwind Loses Momentum

- Comments from President Trump over the sustainability of tariffs on China helped stock indexes bounce off early session lows in an apparent risk-off unwind following Thursday's late rout.

- Support was short-lived, however, with stocks weaker ahead midday. Currently, the DJIA trades down 62.41 points (0.14%) at 46,028.3, S&P E-Mini Future down 9 points (-0.14%) at 6,661.5, Nasdaq down 84.9 points (-0.4%) at 22,484.33.

- A mix Information Technology, Utility and Materials/Industrials sector shares underperformed in the first half: Oracle -7.16%, Newmont -6.77% (Gold -73.5 at 4243.0), Vistra -3.86%, State Street -3.80%, Arista Networks -3.21%, Robinhood Markets -3.04% and Broadcom -2.99%.

- On the positive side, Financials, Consumer Staples and Energy led gainers in the first half, the former rebounding after some heavy selling in regional banks yesterday weighed on the Financials sector: American Express +5.28%, Truist Financial +3.58% and Capital One Financial +3.45%.

- Consumer Staples buoyed by: Kenvue Inc +8.86%, Estee Lauder +1.85%, Philip Morris In +1.58%, General Mills +1.55%; while the Energy sector supported by Expand Energy +1.41%, Marathon Petroleum +1.10%, Exxon Mobil +1.05% and Chevron +0.89%.

- Reminder, corporate earning resume in earnest next week, some highlights: Zions Bancorp that took a hit yesterday reports late Monday, Halliburton, PulteGroup, Lockheed Martin, Northrop Grumman, GM, Netflix, Capital One, Texas Inst, AT&T, Alcoa, American Airlines, Valero, Ford, Intel, General Dynamics, Baker Hughes and Procter & Gamble.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR OPTIONS: Midcurve SOFR BLOCK Update, Separate Oct'25 calls

Two-way call flow ahead midday as underlying futures inching lower. Projected rate cut pricing cools slightly vs. early morning levels (*): Sep'25 at -25.8bp (-27.1bp), Oct'25 at -45.1bp (-46.4bp), Dec'25 at -67.2bp (-69.1bp), Jan'26 at -80.6bp (-82.9bp).

- +20,000 SFRV5 96.50 calls, 2.25 vs. 96.345/0.20%

- Block/screen -75,000 0QZ5 97.00/97.25 call spds, 10.0

FED: US TSY 17W BILL AUCTION: HIGH 3.815%(ALLOT 32.31%)

- US TSY 17W BILL AUCTION: HIGH 3.815%(ALLOT 32.31%)

- US TSY 17W BILL AUCTION: DEALERS TAKE 32.12% OF COMPETITIVES

- US TSY 17W BILL AUCTION: DIRECTS TAKE 7.22% OF COMPETITIVES

- US TSY 17W BILL AUCTION: INDIRECTS TAKE 60.66% OF COMPETITIVES

- US TSY 17W BILL AUCTION: BID/CVR 3.06

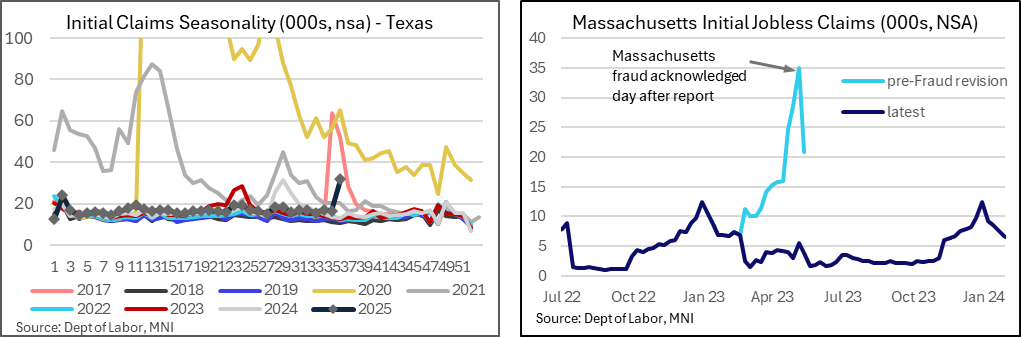

US LABOR MARKET: Massachusetts Lessons For Texas Jobless Claims Fraud

With the rise in Texas initial jobless claims directly linked to ID fraud, we revisit the Massachusetts example from back in May 2023 which saw subsequent revisions to the series two weeks after being first officially recognized. These revisions came outside of the regular claims publication (albeit only by a few minutes) which makes it hard to predict when we might hear something for Texas. Tomorrow’s claims report will no doubt see particular focus on this front but the issue could remain outstanding.

- As noted yesterday, the Texas Workforce Commission indicated that the rise in initial claims was “directly related to an increased volume of fraudulent claim attempts… Since Labor Day, we’ve observed an uptick in ID fraud claim attempts” (cited by Axios, link).

- Recall that last week’s jobless claims release surprisingly jumped to a seasonally adjusted 263k (cons 235k) as the non-seasonally level of claims in Texas increased 15.3k vs 7.9k nationally.

- Axios added that: "The Labor Department did not respond to questions about whether Texas communicated that the fraud issue inflated its claims - and if so, why it was not flagged in the public release." We aren’t surprised by the latter, with it taking some time for fraud in Massachusetts in 2023 to first be acknowledged and then corrected.

- Back in May 2023, national initial jobless claims surprisingly jumped to a seasonally adjusted 264k (cons 245k) in the week to May 6, with Massachusetts accounting for 6.4k of the 14k increase in the national non-seasonally adjusted level as MA continued some sizeable weekly increases. It saw the outright level increase to 34.9k (second only to California’s 46k despite a population less than a fifth of its size).

- The next day (May 12 after the May 11 publication), MA said that the increase was due to fraud attempts.

- However, it wasn’t until May 25 that MA released significant revisions just a few minutes before the publication of the regular claims release. What was seen as the peak 35k initially (before a 14k drop to 21k the week after) was subsequently revised down to 5.5k (and 3.8k).

- Sizeable revisions went back almost three months, although when it comes to Texas, the explicit reference to Labor Day suggests a more limited lookback to the roughly three weeks to Sep 1. Another difference this time is the sudden pop higher for Texas vs the more concerted build in MA.