US STOCKS: Midday Equities Roundup: IT Sector Leads Advances, Micron Beats Est's

Dec-18 16:51

- Stocks surged higher following the softer-than-expected CPI inflation data, maintaining support ahead midday Thursday despite the lack of details within the data (The number of M/M categories included for October is very limited: Gasoline, New and Used vehicles).

- The DJIA bounced off December 10 lows this morning, are currently up 389.8 points (0.81%) at 48274.68, while SPX eminis and the tech-heavy Nasdaq bounced off late November lows: S&P E-Mini Futures up 86 points (1.27%) at 6864.75, Nasdaq up 445.8 points (2%) at 23139.13.

- Information Technology and Consumer Discretionary sector shares led advances in the first half, tech stocks reversing midweek losses: Micron Technology +11.21% after reporting better than expected fiscal Q1 results late Wednesday: late Wednesday of $4.78 per diluted share, up from $1.79 a year earlier.

- Additional tech stocks leaders included: Sandisk Corp +9.42%, Western Digital +6.73%, Lam Research +5.94%, Seagate Technology +5.59% and Palantir Technologies +5.29%.

- Meanwhile, the Consumer Discretionary sector was buoyed by Lululemon Athletica +5.86%, Starbucks +5.72%, Williams-Sonoma +5.55%, DoorDash +4.80% and Tesla +4.63%.

- Conversely, a mix of Financial, Industrials and Energy sector shares declined in the first half: FactSet Research Systems -5.65%, Generac Holdings -3.69%, ServiceNow -2.54%, Marathon Petroleum -2.23%, Tractor Supply -2.19%, Solstice Advanced Materials -2.07%, Diamondback Energy and Devon Energy both down by appr 2%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Treasuries Extend Session Lows

Nov-18 16:48

- No particular driver for Treasuries paring back midmorning support, German Bunds following suit.

- Larger volumes buoyed by surge in Dec'25/Mar'26 roll efforts today.

- No particular headline driver, however, US$ did rebound off lows as US equities bounce off lows.

- Earlier selling in stocks tied to ongoing unwinds of longs in tech shares ahead of Nvidia's earnings expected tomorrow after the close.

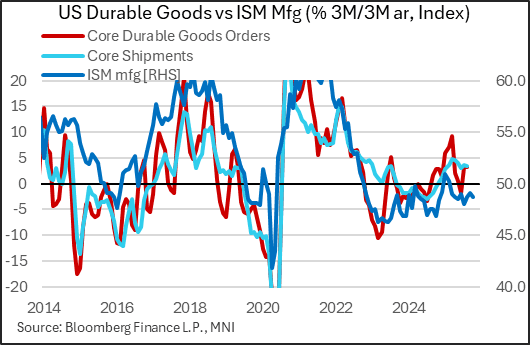

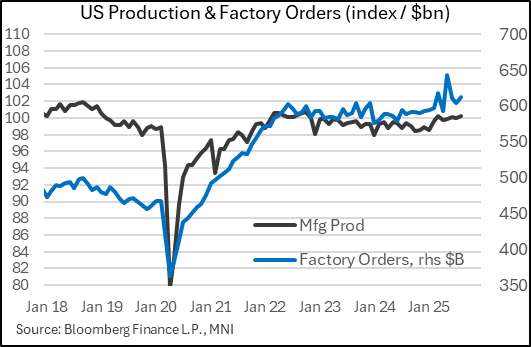

US DATA: Durable / Factory Orders Show Steady Momentum Pickup Through Q3

Nov-18 16:41

The 6-week delayed August Factory Orders data largely confirmed our tracking of a slight pickup in manufacturing and business investment momentum through the middle of Q3, as indicated in the prelim durables report out way back on September 26.

- Factory orders showed an in-line headline growth reading of 1.4% M/M in August, with prior unrevised at -1.3%. Ex-transportation factory orders were slightly weaker than anticipated, at 0.1% (0.3% consensus, 0.5% prior rev down 0.1pp).

- There were slight revisions in the final core durable goods numbers, with capital goods (nondefense/ex-aircraft) shown to rise 0.4% M/M (0.6% prev est, 0.7% prior rev down 0.1pp), with capital goods shipments rev down 0.1pp to -0.4% (prior 0.6%, no revision).

- After pulling back over the summer, momentum is starting to slowly rebuild for core capital capital goods orders and ex-transport factory orders alike: the 3M/3M annualized rate of growth for both 3.1% in August, vs flat/contractionary in May/June and the fastest since Q1's tariff front-loaded activity. Ex-Q1 (which looked tariff-impacted) this is some of the strongest momentum since 2023.

- We still don't know when we will get September / October manufacturing / industrial production data from the Federal Reserve or corresponding months' durable goods orders (September's has already been postponed, and we assume October's prelim will not come out on time later this month). These series looked to be on a slight upswing as of late summer.

- However ISM Manufacturing surveys have consistently shown <50 readings in the interim, suggesting momentum isn't picking up much further into Q4.

BUNDS: /SWAPS: TDS Go Short RX ASWs

Nov-18 16:31

Bund ASWs (vs 6-month Euribor) registered a fresh multi-month high of 5bps today. TD Securities recommend fading this move, opening a short RX spread with a target of -2bps and a stop-loss of 9bp. Their horizon for the trade is one-month, with year-end liquidity presenting the key risk.

- TD believe recent widening in spreads has been driven by the increased pay-side demand in the EUR swaps space.

- They note that pre-positioning ahead of the Dutch pension fund transition in Jan 26 has likely played a role in the recent move, but caution that “pension fund risk is hard to quantify” and “de-risking is expected to occur gradually over 6–12 months rather than all at once.”

- Meanwhile, they suggest “incoming Bund issuance argues for tighter spreads”.