US HEALTHCARE: Merck: M&A Rumors

Jan-09 17:06

(MRK; Aa3/A+/NR) #MNI #Healthcare Merck In Talks to Acquire Revolution Medicines per FT - Slight C...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US 10YR FUTURE TECHS: (H6) Bear Cycle Extends

Dec-10 16:58

- RES 4: 113-29+ High Oct 17 and a key resistance

- RES 3: 113-23 High Oct 23

- RES 2: 113-07/22+ High Dec 3 / High Nov 25

- RES 1: 112-10+/112-25+ Low Nov 20 / 20-day EMA

- PRICE: 112-06+ @ 16:57 GMT Dec 10

- SUP 1: 111-29 Low Dec 10

- SUP 2: 111-19 1.236 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 3: 111-11 1.382 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 4: 111-00 Round number support

A bearish theme in Treasuries remains intact and this week’s move down reinforces current conditions. An important short-term support at 112-07, the Nov 5 low and a bear trigger, has been cleared. The breach strengthens a bear theme and signals scope for a move towards 111-19 next a Fibonacci projection. Initial key resistance is seen at 112-25+, the 20-day EMA. A break of this average would signal a possible reversal.

OPTIONS: Larger FX Option Pipeline

Dec-10 16:44

- EUR/USD: Dec12 $1.1550(E1.3bln); Dec15 $1.1600(E2.3bln), $1.1650(E1.2bln), $1.1680(E1.1bln)

- USD/JPY: Dec12 Y155.00($1.2bln); Dec15 Y156.50($1.1bln)

- GBP/USD: Dec12 $1.3240-55(Gbp1.1bln); Dec16 $1.3500(Gbp3.5bln)

- USD/CAD: Dec12 C$1.3780-00($1.6bln)

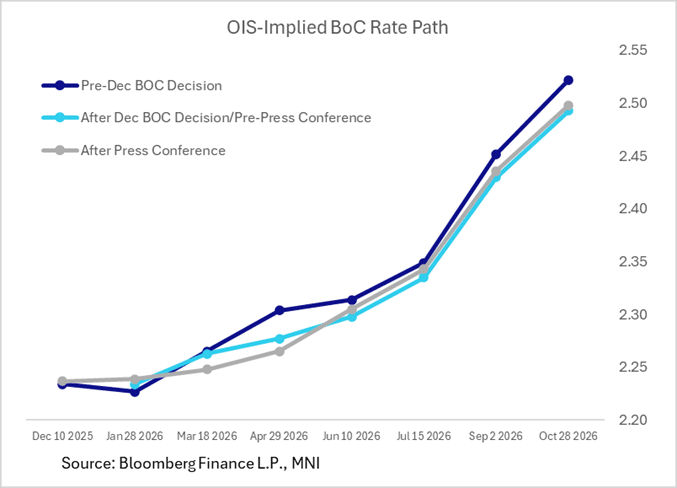

BOC: MNI BoC Review-Dec 2025: Data Seen Solid, But Not Yet Material

Dec-10 16:37

We've just published our review of the December BOC meeting - Download Full Report Here

- As largely expected the BOC produced a fairly neutral appraisal of the economy and rate outlook alongside the unanimously-expected overnight rate hold at 2.25%.

- The market reaction to the decision release was slightly dovish (about 2-3bp of implied hiking taken out of the path over the next 7 meetings), reflecting the Statement's downplaying of recent upside surprises in macro data developments.

- The post-meeting press conference saw little further shift in rate expectations, with Gov Macklem acknowledging the resilience in the Canadian economy evident in the latest data, but highlighting that it “hasn’t fundamentally changed our view”.

- Coming out of the meeting, markets price in 25bp of cumulative hikes through the October 2026 meeting, vs 27bp prior, with the path through H1 2026 almost completely flat.

- Attention turns to two key data releases to round out the year: November CPI (December 15) and October GDP (December 23), with the December labour report (January 9) and CPI (January 19) the key releases ahead of the Bank of Canada’s next decision on January 28 (1bp of cuts priced).

- See PDF report for:

- MNI View

- MNI Instant Answers

- Press Conference Transcript

- BOC Meeting Links

- Policy Statement Changes