EM LATAM CREDIT: MercadoLibre: New 7-Year Fair Value

(MELI; Ba1*+/BBB-/BBB-)

IPTs 7Yr: T+160bp FV 7Yr: T+135bp

• Uruguay based Latin America electronic retailer MercadoLibre proposed USD benchmark-sized senior unsecured 7-year registered notes that will be rated BBB-/BBB-. We put fair value for the 7-year at T+150bp, similar to quoted levels for Arcos Dorados and wider than IG rated Suzano.

• MELI Jan 2031s were quoted as g-spread 121bp. We estimate additional credit spread of 13bp to put a new 7-year at T+134bp.

• Mercado Libre has a strong credit profile as a consistent free cash flow generator with low debt leverage of 1.19x as of Q3 2025 and strong growth in both revenues and EBITDA. MercadoLibre is geographically diversified as Brazil comprises a little more than half of total revenues with the remainder split mostly between Mexico and Argentina.

• Uruguay based Latin American fast food retailer Arcos Dorados (ARCO; Ba1/BBB-/BBB-) has a similar credit profile as profitable, low leveraged and a broad Latin American presence with large Brazil exposure. ARCO credit ratings are somewhat limited by the Brazil sovereign ceiling and equal to MELI. ARCO Jan. 2032 notes were quoted at a g-spread of 143bp. Ten months’ extra credit spread of 5bp would put a new ARCO 7-year at T+148bp.

• We also looked at another retailer in the region, Mexican retailer Liverpool (LIVEPL; NR/BBB/BBB+), with Jan. 2032 notes quoted g-spread 125bp.

• Investment grade rated on positive outlook at all three agencies, Brazil paper company Suzano (SUZANO; Baa3pos/BBB-pos/BBB-pos) 2031s were quoted at g-spread 137bp and 2032s at 140bp.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUR: FX Exchange traded Call Buyer

EURUSD (6th Mar) 1.1800c, bought for 0.008 in ~4.6k.

EFSF ISSUANCE: New 5-year Nov-30 / 2.875% Jan-2035 tap: Priced

- Reoffer: 99.629 / 2.580%

- Spread set earlier at MS+22bps (guidance was MS+24 bps area)

- Size: E3.0bln (E2.5-3.5bln)

- Final books in excess of E23.5bln (ex JLM interest)

- Maturity: 11 November 2030

- Coupon: 2.50%

- Hedge ratio: 100% vs 2.20% Oct-30 Bobl (Spot ref 99.755 +33.0bp)

- ISIN: EU000A2SCAV2

- Timing: TOE 13:37GMT / 14:37CET. FTT immediately.

- Reoffer: 98.928 / 3.009%

- Spread set earlier at MS+39bps (guidance was MS+42 bps area)

- Size: E1.5bln (middle of MNI's expected E1.0-2.0bln)

- Final books in excess of E22.5bln (ex JLM interest)

- Hedge ratio: 98% vs 2.50% Feb-35 Bund (Spot ref 99.064 + 39.5bp)

- ISIN: EU000A2SCAS8

- Timing: TOE 13:38GMT / 14:38CET. FTT immediately.

- Settlement: 11 November 2025 (T+5)

- Bookrunners: BNPP / BofA (DM/B&D) / NATWEST

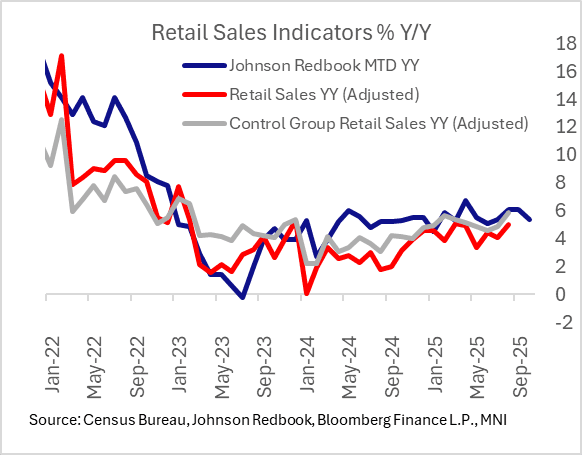

US DATA: Redbook Retail Sales Close Out October On Solid Footing

Retail sales growth picked up in the final week of October to 5.7% Y/Y from 5.2% prior, per the Johnson Redbook index. This kept October's sales at +5.4% Y/Y, same as the month-to-date figure estimated for the prior week albeit slightly below retailers' targeted 5.6% gain.

- The report notes that "the past week saw an increase in customer traffic and sales, primarily driven by demand for Halloween merchandise. However, the holiday may have negatively impacted shopping patterns on Friday, a key day for retailers, by diverting customers away from stores while boosting sales at those catering to Halloween shoppers."

- There will be more detail on October sales out this Thursday with the Johnson Redbook Same-store Flash Report based on stores' reported sales for the month that are out that day. For now Johnson Redbook is targeting 6.2% Y/Y sales growth in November, noting " This month features several significant shopping promotions, including those around Election Day, Veterans Day, and Thanksgiving."

- Overall October retail data look to have been solid, between Redbook's figures and Chicago CARTS' preliminary estimate of ex-auto sales equivalent to a 4.3% Y/Y rise in ex-auto sales gains for a 2nd consecutive month (though of course we don't yet have official September data let alone October due to the federal government shutdown).