EM LATAM CREDIT: MercadoLibre: New 7 & 10-Year Notes Fair Value

(MELI; Ba1*+/BBB-/BBB-)

IPTs 7Yr: N/A FV 7Yr: T+150bp

IPTs 10Yr: N/A FV 10Yr: T+171bp

• Uruguay based Latin America electronic retailer MercadoLibre registered to sell USD benchmark-sized senior unsecured notes. The notes for up to USD1bn will mature in 2032 and 2035 according to Fitch. We put fair value for the 7-year at T+150bp, similar to quoted levels for Arcos Dorados and wider than IG rated Suzano. From there we add another 21bp of credit curve to derive fair value of T+171bp for a new MELI 10-year.

• MELI Jan 2031s were quoted as g-spread 125bp. We estimate additional credit spread of 13bp to put a new 7-year at T+137bp; however, this is MELI’s only outstanding USD bond which was issued almost five years ago and has been steadily bought back such that only USD535.6mn remain from the original USD700mn. Investment grade rated on positive outlook at all three agencies, Brazil paper company Suzano (SUZANO; Baa3pos/BBB-pos/BBB-pos) 2031s were quoted at g-spread 137bp with a new Suzano 7- year fair value at T+145bp.

• MercadoLibre is geographically diversified as Brazil comprises a little more than half of total revenues with the remainder split mostly between Mexico and Argentina. Uruguay based Latin American fast food retailer Arcos Dorados (ARCO; Ba1/BBB-/BBB-) has a similar credit profile as profitable, low leveraged and a broad Latin American presence with large Brazil exposure. ARCO credit ratings are somewhat limited by the Brazil sovereign ceiling and equal to MELI. ARCO Jan. 2032 notes were quoted at a g-spread of 143bp. Ten months’ extra credit spread of 5bp would put a new ARCO 7-year at T+148bp.

• We also looked at another retailer in the region, Mexican retailer Liverpool (LIVEPL; NR/BBB/BBB+), with Jan. 2032 notes quoted g-spread 125bp and LIVEPL 2037 bonds quoted g-spread 162bp which implies a Treasury spread of about 155bp for a 10Yr.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

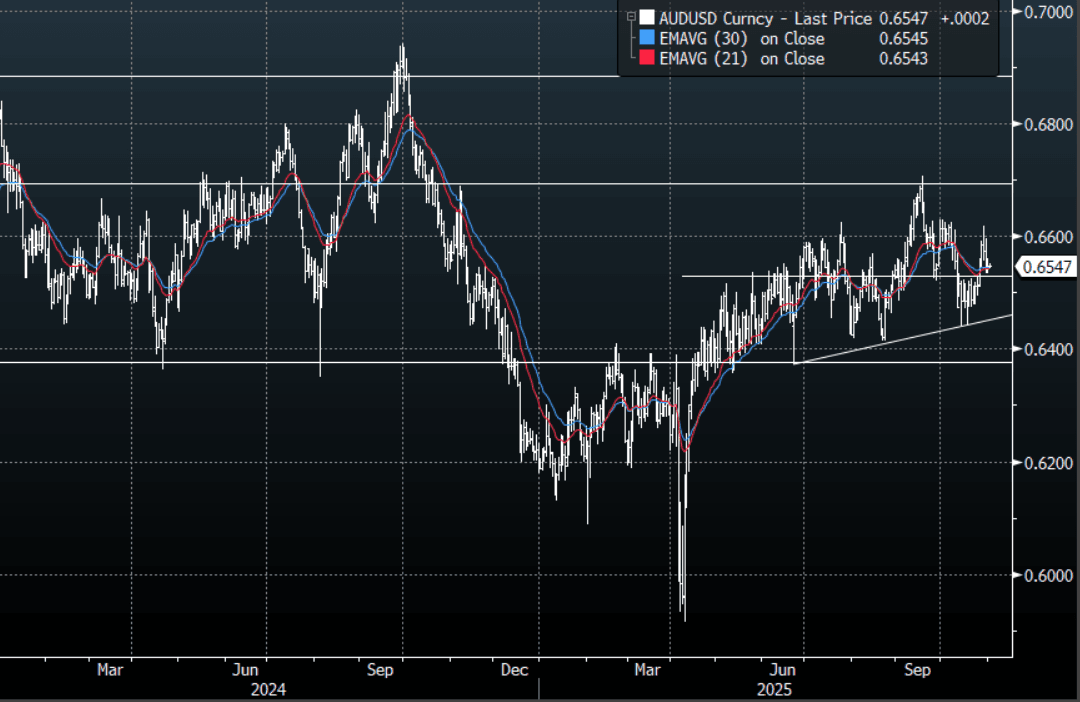

AUD: AUD/USD - Consolidates Around 0.6550 Ahead Of RBA Tomorrow

The AUD/USD had a range Friday night of 0.6533-0.6553, Asia is trading around 0.6545. US yields retraced on Friday night but the USD continues to grind higher challenging levels last seen in July/August. The AUD/USD is back within its recent 0.6400-0.6650 range with the pivot being around 0.6500-0.6550 where I would expect some demand first up, RBA tomorrow but the market is not expecting them to move.

- MNI Policy: RBA Board To Hold, Push Out Midpoint Return. The Reserve Bank of Australia Board is expected to keep the cash rate at 3.6% next Tuesday following stronger-than-expected Q3 inflation and is likely to push back the anticipated return of inflation to the midpoint in updated forecasts released alongside the decision.

- Bloomberg reports Australian home prices climbed at the fastest pace in more than two years in October, underscoring how a resurgent property market threatens to complicate the RBA’s efforts to cool inflation in this week’s rate decision.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD 338m). Upcoming Close Strikes : 0.6625(AUD944m Nov 4), 0.6300(AUD600m Nov 4) - BBG

- Data/Event: Melbourne Institute Inflation, ANZ-Indeed Job Advertisements, Building Approvals, Household Spending

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

NEW ZEALAND: Unemployment Rate Forecast To Rise Again, Nov Easing Likely

The key event in NZ this week is the Q3 labour market and wages data released on Wednesday. Filled jobs for the quarter signal a stabilization but employment is likely to have remained weak with consensus forecasting it to rise only 0.1% q/q to be still down 0.2% y/y. The unemployment rate is expected to rise 0.1pp to 5.3%, in line with the RBNZ’s August projections. Soft labour demand is likely to weigh on private wage growth which is forecast to rise around 0.4% q/q after 0.6%.

- The RBNZ’s biannual financial stability report is also published on Wednesday. It is likely to be concerning if it shows an increase in mortgage arrears despite recent easing.

- In terms of housing data, October Cotality home values and September building permits are released Monday. The construction sector has lagged the rest of the economy but the ANZ business survey is showing some recovery.

- October ANZ commodity prices are released on Wednesday. They fell 1.1% m/m in September.

AUSSIE 10-YEAR TECHS: (Z5) Returns Lower

- RES 3: 95.982 - 76.4% retracement Sep’24 - Nov’24 downleg

- RES 2: 95.960 - High Apr 7 (cont.)

- RES 1: 95.900 - High Oct 17

- PRICE: 95.670 @ 16:16 GMT Oct 31

- SUP 1: 95.510 - Low Sep 3

- SUP 2: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 3: 95.275 - Low Nov 14 (cont) and a key support

Aussie 10-yr futures slipped lower Wednesday on the back of hotter-than-expected Australian inflation. This returned prices lower despite nascent signs of a technical recovery as recently as last week. The sustainability of the pullback will be dependent on prices holding above key short-term support at 95.510, the Sep 3 low. Near-term resistance remains 95.780, the Sep 12 high. A clear break of this level signals scope for a continuation higher and opens 95.960, the 76.4% retracement level for the Sep’24 - Nov’24 downleg.