STIR: Market Wary The RBA May Disappoint Again

RBA-dated OIS pricing is slightly firmer across meetings today.

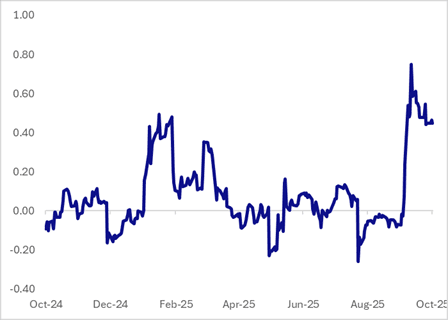

- A 25bp rate cut in November is assigned a 64% probability (peak 80%, pre-data 38%), with a cumulative 23bps of easing (peak 25bps, pre-data 13bps) priced by year-end.

- Compared with the lead-up to previous potential cuts in this easing cycle, the market appears less certain than usual about a November 4 move.

- This caution aligns with the RBA’s pattern over the past year of easing less than what 6-month forward expectations had implied.

- Those expectations currently sit around 3.20%, compared with the cash rate of 3.60%.

Figure 1: RBA Cash Rate Vs. OIS 6M1M (6M Ago)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Weaker & At Cheaps After RBA Gov Testimony

ACGBs (YM -3.5 & XM -5.0) are weaker and at cheaps.

- In today’s testimony to the House of Representatives Standing Committee on Economics, RBA Governor Bullock stated that the RBA expects recent interest rate cuts to support household and business spending. Labour market conditions are near full employment, though unemployment has risen slightly since the last meeting, with some tightness remaining. Household consumption growth is expected to continue as real incomes rise. Since the August meeting, domestic data have been broadly in line with or slightly stronger than expectations. The overall economic outlook remains clouded by uncertainty.

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session after Friday’s modest sell-off.

- Cash ACGBs are 3-4bps cheaper with the AU-US 10-year yield differential at +14bps.

- The bills strip is -3 to -4 across contracts.

- RBA-dated OIS pricing is giving a 25bp rate cut in September a 5% probability, with a cumulative 27bps of easing priced by year-end.

- August CPI data is due on Wednesday.

- This week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Tuesday, A$1000mn of the 3.00% 21 November 2033 bond on Wednesday and A$900mn of the 2.75% 21 November 2029 bond on Friday.

BOJ: MNI BoJ Review – September 2025: Cautious But Signals Progress

Executive Summary

- Policy Decision & Dissents: The BOJ kept rates at 0.5%, but two members dissented in favour of a 25bp hike, arguing the price target is “more or less achieved” and rates should move “closer to neutral,” highlighting stronger hawkish voices within the board.

- Governor Ueda’s Tone: Ueda remained balanced, noting “underlying inflation is approaching 2%, but the 2% level has not yet been reached” and that there is “little sign of tariff having impact on Japan’s economy,” while emphasising ongoing global uncertainty and data dependency.

- Inflation & Growth Outlook: Core inflation remains above 3% with wage growth expected to keep inflation “floating above 2%.” Risks from tariffs are seen as contained, and potential supports include “Fed rate cuts,” “AI-related investment,” and “deregulation.”

- Rate Hike Timing & Risks: Views diverge—some expect a hike in October following the Tankan Survey and LDP leadership election, while others see January 2026 as the base case. Political risks (e.g., dovish LDP candidates) and Fed-driven yen appreciation could delay tightening.

- Asset Sales: The BOJ will gradually sell ¥330bn of ETFs and ¥5bn of J-REITs annually, a pace that would take “more than 100 years” to unwind holdings. The Bank aims to “avoid losses as much as possible” and limit market disruption, though acceleration remains possible.

- See full MNI BoJ Review here

CHINA PRESS: Listed Companies To Cut Deposits For Wealth Management Products

Listed companies will likely continue to move their deposits into wealth management products, with the scale reaching hundreds of billions of yuan in the next year, Yicai.com reported citing analysts. In the past year as of Sept 21, listed companies have announced a total CNY373.4 billion of entrusted wealth management, according to data by Choice Terminal. Currently, the one-year fixed deposit interest rate has dropped to 0.95%, while the average annualised yield of bank wealth management products has reached 2.12%, coupled with the general rise in major stock market indices, the newspaper said noting the significant yield gap. Investors are also increasingly adopting overseas wealth management through QDII and Southbound Connect, the newspaper added.