STIR: Market Still Prices Over 90% Odds Of Dec Cut, No Reaction To ISM

Little net reaction in the USD short end following the mixed ISM services report, which won’t have changed the picture for the Fed (with elevated inflation and questions surrounding the health of the labor market remaining intact).

- To recap, while the headline index and was firmer-than-expected, the prices paid component (while still elevated at 65.4) came in on the softer side of expectations. Meanwhile, the new orders subindex showed a slower rate of expansion and the employment subindex showed a slightly reduced rate of contraction.

- Fed Funds continue to indicate 23.5bp of easing for this month, 32bp through January, 40bp through March, 48bp through April and 62.5bp through June.

- SOFR futures 0.25-3.0 firmer on the day vs. 0.25-3.5 firmer heading into the ISM release.

- Implied terminal rare pricing 3.025% after threatening to break below 3.00% earlier.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Fed Pricing Little Changed Over ISM

Modest dovish reaction in Fed pricing as the headline ISM manufacturing survey reading prints below the wider consensus and the prices paid component is softer than expected (albeit still comfortably in expansionary territory at 58.0).

- The move lacks any real traction.

- FOMC-dated OIS pricing 17.5bp of easing for December, 26bp through January, 35bp through Match and 55.5bp through June, little changed to 0.5bp more dovish vs. pre-data levels.

- SOFR-implied terminal rate pricing last 3.10% vs. 3.105% heading into the data and the ~2.83% dovish extreme seen in October.

- Note that some weakness in e-minis through the cash open provided dovish impetus ahead of the data.

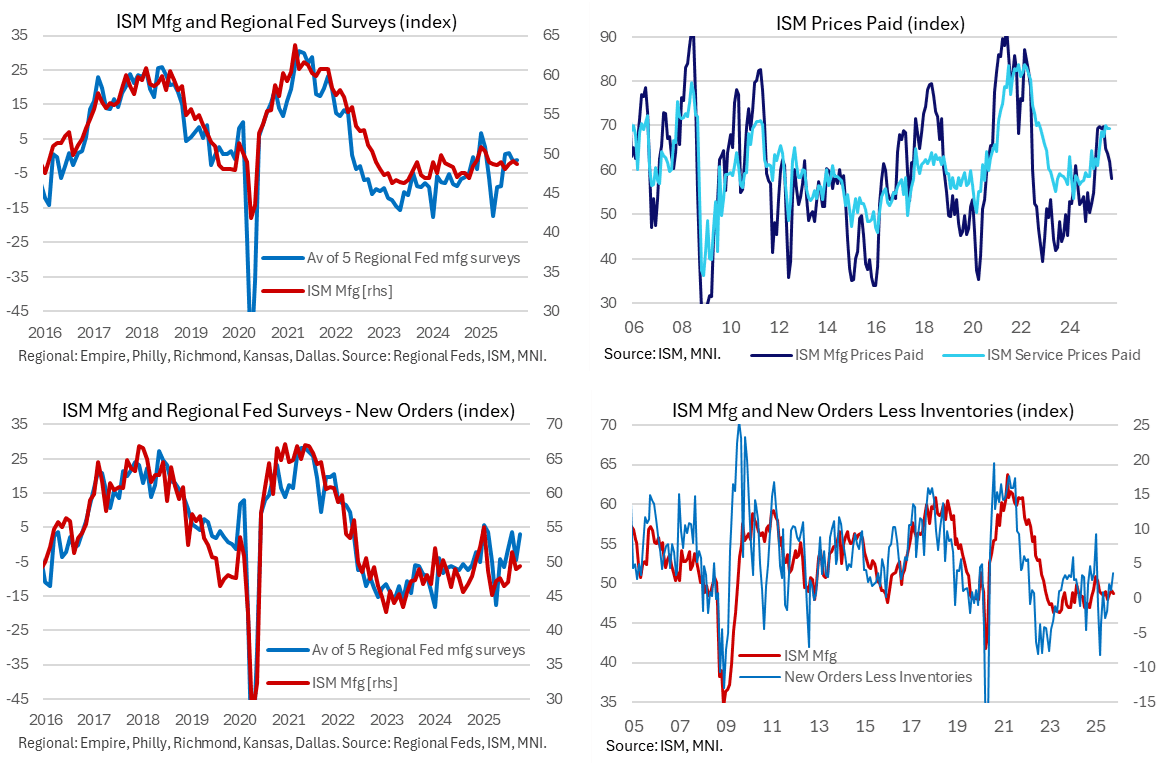

US DATA: A Broadly Disappointing ISM Manufacturing Survey For October

The ISM manufacturing survey for October underwhelmed across the board, undershooting implications from regional Fed surveys, the MNI Chicago PMI and what continues to be a much more optimistic S&P Global PMI. New orders disappointed a bounce seen elsewhere and prices paid fell to the lowest since January, although new orders less inventories did at least point to upside for manufacturing activity ahead.

- ISM manufacturing: 48.7 in Oct (cons 49.5) after 49.1 in Sep

- New orders: 49.4 in Oct after 48.9 in Sep. The small 0.5pt increase after the -2.5 drop in September is disappointing considering the regional Fed surveys along with the MNI Chicago PMI had pointed to a solid bounce in new orders.

- Interestingly however, inventories didn’t echo the sharp increase from the S&P Global US PMI (its sharpest increase since the data started in 2007) but instead fell 1.9pts to 45.8 for the lowest since Oct 2024. That in turn meant that the new orders less inventories metric increased to 3.6 for its highest since January, at least implying some upside to manufacturing activity ahead.

- Prices paid: 58.0 in Oct (cons 62.5) after 61.9 in Sep. Consensus came from a typically limited survey of six analyst estimates but had looked reasonable considering the regional Fed surveys were on average were little changed on the month whilst continuing to run at higher outright levels.

- Prices are an area where the ISM report is more in line with the PMI, with prices paid at their lowest since January vs February in the PMI.

- Employment: 46.0 in Oct after 45.3 in Sep, marking a third consecutive increase for its highest since May but still firmly in contraction territory. The index has been in expansionary territory (>50) in just two months of the past two years, with a high in that period of 50.4. We put much more weight on the ISM services survey for this component.

FED: Chicago's Goolsbee: Worried About Inflation, Not Decided On Dec Cut

Chicago Fed's Goolsbee (a current FOMC voter) says on Yahoo Finance that he sees a higher bar for deciding to cut rates in December than in October. "I'm not decided going into the next meeting. I want to see how things are playing out." But he also points to potential for rates to come down "a fair amount".

- He's "been a little more worried about inflation than the job market" with an economy that "has been pretty strong", and the unemployment rate remaining "pretty stable" and no big rise in layoffs. And "the fact that the last three months inflation is not going down, but is instead going up, including in some categories that are not driven by tariffs, like services, those are areas of concern. And so that's a little bit, you know, the last time you looked out the window, there was a mountain lion sitting in your front yard. So before you let Fluffy out to go run around, just let's at least get one more look."

- Like Powell's analogy last week of driving a car through fog amid the recent lack of federal government data, Goolsbee makes a driving analogy: "one of the hardest things the central bank ever has to do is get the timing right on moments of transition, and that's especially difficult if you have squished bugs covering the windshield and you can't see whether you're still on the road, and when they shut down the data, the official data, that's the circumstance we're in. "

- He concludes: "I'm not decided going into the December meeting, I am nervous about the inflation side of the ledger, where you've seen inflation above the target for four and a half years, and it's trending the wrong way. I believe on the other side, rates can come down a fair amount. It would probably be most judicious to have the rates come down with inflation. So let's get some observations that document that inflation is coming down and that the uptick we've seen is transitory, but we've got to weigh that off if the job market starts to deteriorate in us in a more significant way, then that would change the balance of risks. "