FED: Market Participants Eye Bill Buying, With MBS Running Off "Indefinitely"

The anecdotes of expectations for Fed balance sheet policy in the September Survey of Market Expectations suggest participants were slightly divided on the criteria that the Fed is likely to use to determine when to end balance sheet runoff.

- "Many respondents indicated they expected the end of balance sheet runoff to be determined by liability management considerations; some respondents cited the level of reserves as the primary factor influencing their estimate for the end of runoff, some respondents emphasized funding market indicators and several emphasized assessments of certain thresholds of reserves as a share of nominal GDP or bank assets."

- Additionally, there was uncertainty in both directions as to the timing of runoff ending, as well as to the ultimate size of SOMA holdings. It seems that the plurality of respondents saw risks of an earlier end to runoff ("several" vs "some"): "Some respondents viewed the distribution of outcomes as skewed toward a later end to runoff or a smaller SOMA portfolio versus their baseline expectations. In explaining these risks of a later end to runoff, several cited funding market or reserves dynamics while several cited the Standing Repo Facility as potentially enabling balance sheet runoff to continue longer. Several respondents viewed the distribution of outcomes for the end of runoff as skewed toward an earlier end of runoff or a larger SOMA portfolio versus their baseline expectations."

- The anecdotes also eyed potential post-QT balance sheet policy prospects - the key expectations were for reserve management purchases to involve primarily bills, with MBS running off "indefinitely": "Some respondents expected maturing MBS would be reinvested in Treasury securities once the reduction in the size of the balance sheet has been completed. Some respondents discussed expectations for reserve management purchases; several expected those purchases to be primarily composed of U.S. Treasury Bills. Several respondents expected the runoff of MBS holdings to continue indefinitely."

- Another question asked is "Please provide your expectation for each of the selected money market rate spreads* for the day after each of the FOMC meetings".

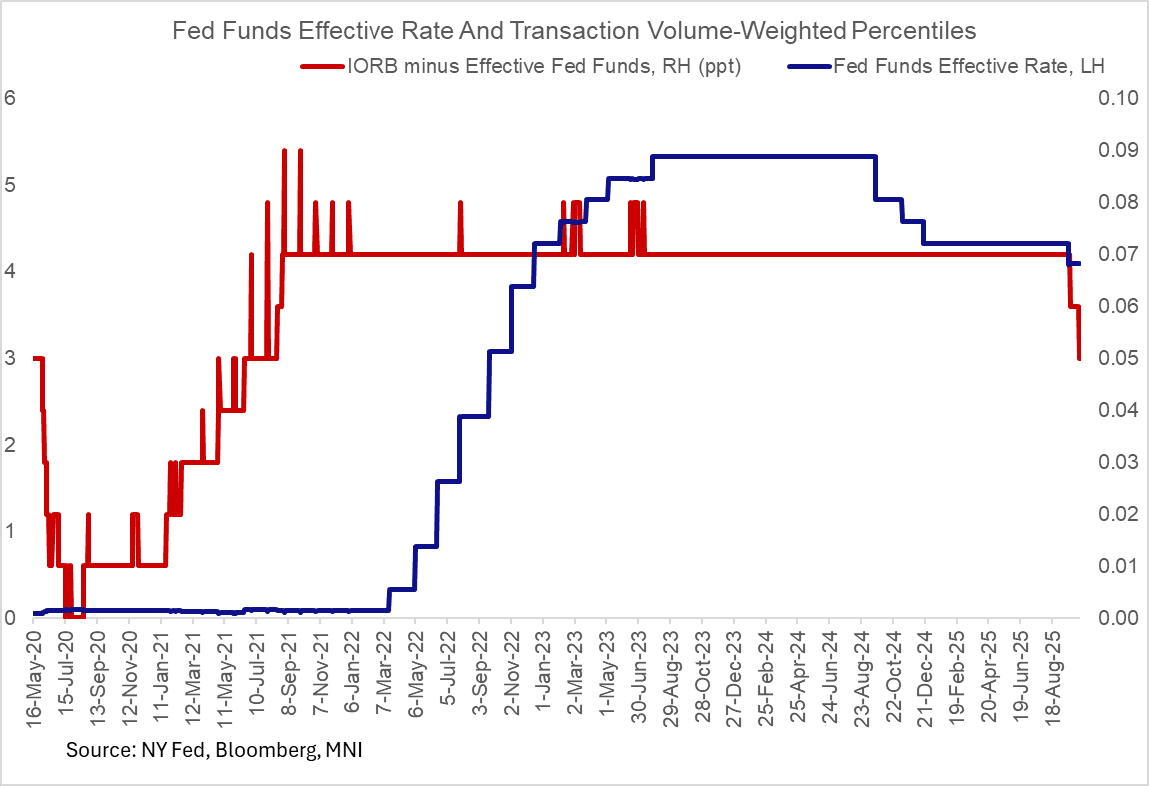

- There were no evident expectations for the moves in money markets we've seen in the last couple of weeks, for example Effective Fed Funds minus IORB was seen at a steady -7bp through January, however that's already moved to -5bp (EFFR 4.10% vs IORB 4.15%). That could potentially suggest that market dynamics are shifting more quickly than participants expected in a direction that would warrant Fed action.

- There were no expectations in the medians or the 25th/75th percentile respondents that there would be any shift in the Fed's administered rates through at least January, including ON RRP (seen = to the bottom of the Fed funds target range) and IORB (seen remaining 10bp below the top of the Fed funds target range).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Trading Above Support

- RES 4: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 3: 1.3925 High Aug 22 and the bull trigger

- RES 2: 1.3868 High Aug 26

- RES 1: 1.3854 High Sep 05

- PRICE: 1.3838 @ 17:43 BST Sep 9

- SUP 1: 1.3727 Low Aug 27 and a bear trigger

- SUP 2: 1.3709 61.8% retracement of the Jul 23 - Aug 22 bull cycle

- SUP 3: 1.3658 76.4% retracement of the Jul 23 - Aug 22 bull cycle

- SUP 4: 1.3637 Low Jul 25

A bull cycle in USDCAD remains intact. Near term, the recovery from the Aug 29 low highlights a potential early reversal signal and if correct, the end of the corrective pullback between Aug 22 - 29. An extension higher would open the bull trigger at 1.3925, the Aug 22 high. Support lies at 1.3727, the Aug 29 low. Clearance of this level would instead reinstate a short-term bear theme and expose 1.3709 initially, a Fibonacci retracement.

US TSYS: Eyes on PPI, Cash 2s10s Remains Dis-Inverted, 3Y Stops Through

- Treasuries look to finish weaker, off late morning lows with rates paring losses after a decent $58B 3Y Note auction broke a four consecutive auction run of tails w/ 3.485% high yield vs. 3.492% WI; 2.73x bid-to-cover vs. 2.53x prior.

- After some sharp two-way action - Tsys retreated after BLS Prelim Benchmark Revision to Establishment Survey Data comes out much lower than anticipated: -911k vs. -682k est from -818k prior.

- Meanwhile, Johnson Redbook Retail Sales Index rose 6.6% Y/Y in the first week of September (ending Sep 6), running a little above retailers' targeted 6.3% gain for the month.

- Currently, the Dec'25 10Y trades -6.5 at 113-11 (yld 4.0722 +.0324) vs. 113-07 low -- Initial firm support to watch is 112-11+, the 20-day EMA. Yield curves flatter: 2s10s -2.311 at 52.831, 5s30s -1.536 at 114.416. Cash 2s10s adjusted for carry/rolldown remains dis-inverted 58.9.

- US$ off lows, BBG index BBDXY currently +2.6 at 1201.15 vs. 1196.68 post data low.

- Focus turns to US price data, as PPI and CPI releases are expected across Wednesday and Thursday respectively. China CPI and PPI figures will be released during APAC hours tomorrow.

AUDUSD TECHS: Approaching The Bull Trigger

- RES 4: 0.6688 High Nov 7 ‘24

- RES 3: 0.6677 0.764 proj of the Jun 23 - Jul 11 - 17 price swing

- RES 2: 0.6625 High Jul 24 and the bull trigger

- RES 1: 0.6620 High Sep 9

- PRICE: 0.6595 @ 17:42 BST Sep 9

- SUP 1: 0.6522 20-day EMA

- SUP 2: 0.6463/6415 Low Aug 27 / Low Aug 21 / 22 and a bear trigger

- SUP 3: 0.6373 Low Jun 23

- SUP 4: 0.6354 38.2% retracement of the Apr 9 - Jul 24 upleg

AUDUSD traded higher again Tuesday to build on the latest gains and remains firm. The current bull cycle confirms the end of a corrective phase that started on Jul 24. Resistance at 0.6569, the Aug 14 high, has been cleared. This exposes key resistance and the bull trigger at 0.6625, the Jul 24 high. Support to watch is 0.6415, the Aug 21 / 22 low. A clear break of it would instead resume a bear leg and highlight a stronger reversal.