US LABOR MARKET: Macro Since Last FOMC: Payrolls Slowly Rise After Oct Hit [1/3]

We take an early look at what economic data the FOMC has received since the Dec 9-10 meeting, starti...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

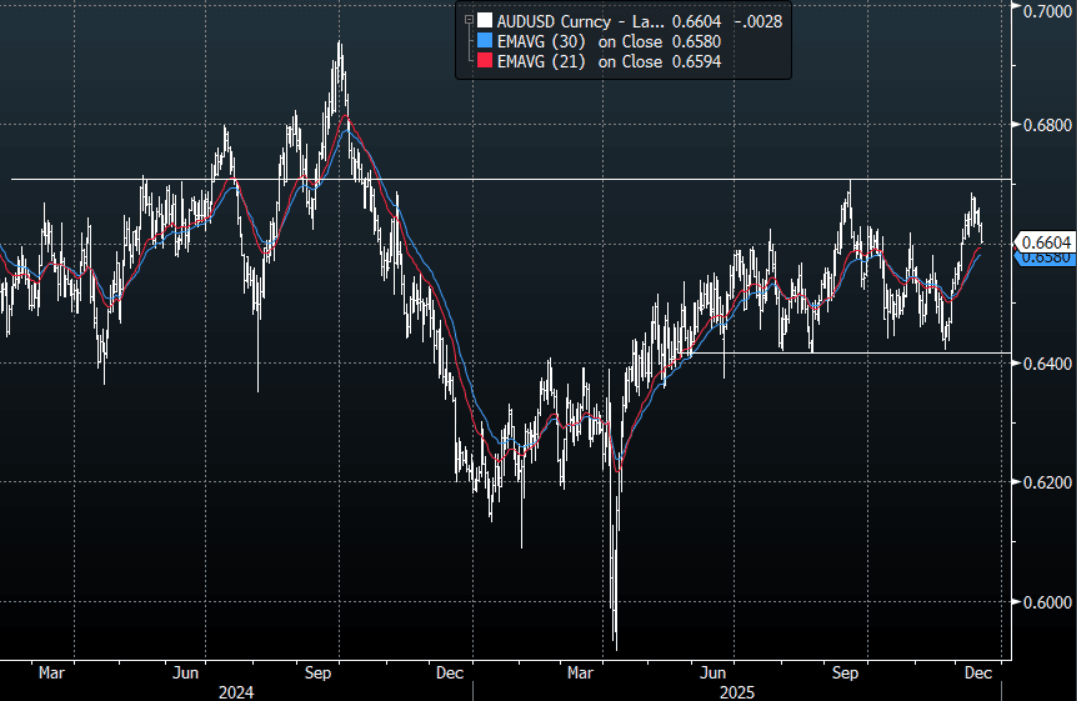

AUD: AUD/USD - Trades Heavy Around 0.6600 As Risk Sentiment Sours

The AUD/USD had a range overnight of 0.6599-0.6629, Asia is trading around {AUDUSD Curncy}. The bounce in AI lasted 1 day and is lower again, the move is starting to turn ugly as sentiment is quickly changing. The NASDAQ and the S&P both look to potentially be putting in double tops and the likes of Nvidia is approaching some pivotal levels as well. This does not augur well for risk and creates significant headwinds for the AUD which trades with a high correlation to it. The AUD price action for the moment remains constructive, but I do remain wary of what seems to be happening in US stocks. Technically while the AUD remains above 0.6500-0.6550 dips should continue to be supported. In the Asian session, watch to see if this 0.6600 area can continue to hold in the face of this souring in sentiment, if not we could see a deeper pullback towards the 0.6500-50 support. On the day I suspect sellers would be looking to fade a bounce back toward the 0.6625-0.6645 area initially looking to see if we can break back below 0.6600.

- Bloomberg reports, “China Vanke asked some commercial banks to accept delayed interest payments on certain borrowings, people familiar said. At least one lender was asked to let the developer delay an interest obligation by one year.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6550(AUD1.07b), 0.6625(AUD849m), 0.6675(AUD989m). Upcoming Close Strikes : 0.6675(AUD1.31b Dec 19), 0.6700(AUD1.57b Dec 19) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 40 Points

- Data/Event: Consumer Inflation Expectation

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

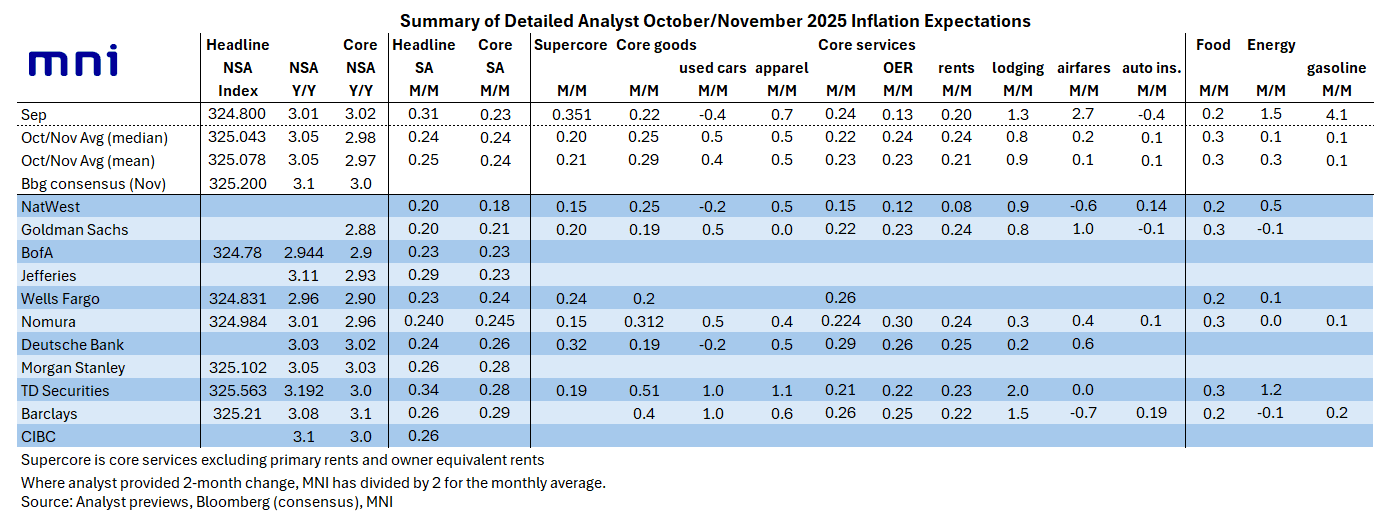

US PREVIEW: Analysts Generally Expect Upside CPI Pressure Coming From Core Goods

Our compilation of sell-side analyst expectations for Thursday's CPI report uses a narrower range of previews - namely, those that included core CPI forecasts to two decimal places or more for the 2-month or Oct and Nov % M/M changes. Within a range of 0.18-0.29% for average core CPI % M/M over October and November, Barclays is at the high end of expectations while NatWest is at the low end. A few summaries below:

- Barclays: Core CPI to average 0.29% M/M across Oct-Nov (two-month cumulative increase of 0.58%), with headline averaging 0.26% M/M (two-month cumulative of 0.52% M/M). “We expect the uptick to be led mainly by core goods prices, which we forecast to have sequentially accelerated over the prior two months, led by a rebound in used cars prices and firmer inflation across the remaining core goods basket. We estimate services inflation to have also gathered steam, partly led by a rebound in OER CPI following the downside surprise in September.”

- Nomura: Core CPI to average 0.245% M/M across Oct-Nov (0.228% Oct, 0.263% Nov); headline 0.24%. "We expect core goods inflation remained strong due to tariff effects as well as higher used vehicle prices...The recent firming of import prices and further tariff passthrough likely pushed up non-auto core goods prices, which leads us to forecast continued strength in apparel and other goods prices in October and November...Supercore service inflation likely slowed due to lower health insurance prices and other volatile service prices, while inflation of rent-related components likely rebounded after a temporary slowdown in September."

- Goldman Sachs: Core CPI to average 0.21% M/M across Oct-Nov (0.16% Nov, 0.25% Oct), headline CPI to average 0.20% M/M across Oct-Nov (0.27% Nov, 0.14% Oct). “we have penciled in upward pressure from tariffs on goods categories that are particularly exposed worth +0.08pp on core inflation on average across October and November”

- NatWest: Core CPI to average 0.18% M/M across Oct-Nov (cumulative 0.35%), headline CPI to average 0.20% M/M across Oct-Nov (cumulative 0.40%)."we suspect it will be extremely challenging to try to draw many firm conclusions and suggest market participants use caution interpreting any surprises in the upcoming report...Within the details, we project that core goods prices increased 0.5% and core services advanced 0.3% (and core services ex rents +0.3%).”

ASIA: Coming Up In Asia Pac Markets On Thursday

| 2145BST | 0545HKT | 0845AEDT | New Zealand Q3 GDP |

| 2350BST | 0750HKT | 1050AEDT | Japan Weekly Investment Flows |

| 0000BST | 0800HKT | 1100AEDT | Australia Dec Consumer Inflation Expectation |

| 0100BST | 0900HKT | 1200AEDT | China Nov Swift Global Payments CNY |

| 0330BST | 1130HKT | 1430AEDT | Japan 3mth Bill Sale |

Source: Bloomberg Finance L.P./MNI