CNH: Lower US Tsy Yields Brings Fresh USD/CNH Downside Back Into Focus

The softer US Tsy yield backdrop, post the weaker CPI print (albeit which had meaningful caveats placed against it) has helped reignite USD/CNH downside risks. We got to fresh lows of 7.0309 in Thursday trade and track near 7.0330 in latest Friday dealings. Spot USD/CNY finished up at 7.0413, so still above the 7.0400 figure level, which, along with the USD/CNY fixing bias, will be in focus today. The CNY CFETS basket tracker pushed up to 97.88, but remains under late Nov highs.

- US-CH yield differentials have softened over the past week, but remain within recent ranges, the 2yr spread around +207bps. For USD/CNH if onshore spot can break under 7.0400, that may see USD/CNH test through 7.0300 and bring 7.00 handle risks back into focus before year end. On the topside for USD/CNH note that the 20-day EMA is just above 7.0600.

- Later today we get Nov FX settlement data, which will be eyed for conversion trends. We still await the Nov FDI figures. Next week, the 1yr and 5yr Loan prime rate decisions are out, with no change expected.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

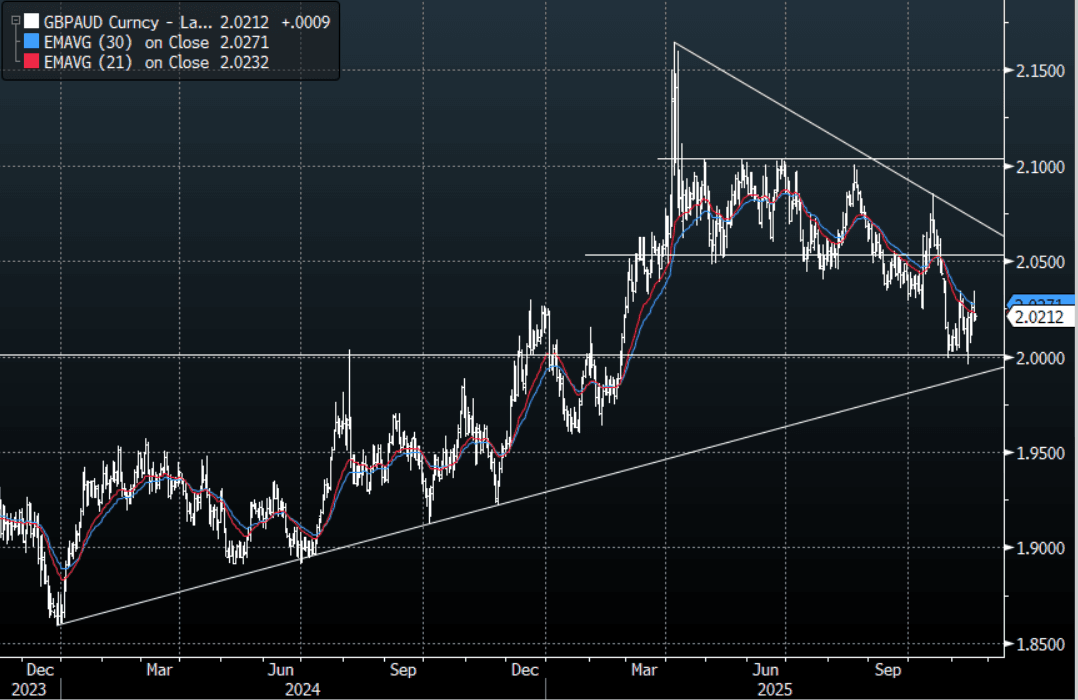

AUD: GBP/AUD - Stalls Around 2.0350 Again

The overnight range was 2.0198 - 2.0318, Asia is trading around 2.0215. The pair stalled again testing some tough resistance just ahead of 2.0400. While risk remains under pressure expect the AUD to underperform in the crosses but should GBP/AUD get back toward the 2.0500 level I would be skewed towards fading the move at the first attempt. On the day it looks like we might consolidate as the market awaits the Nvidia earnings result tomorrow morning to give risk some direction. The range looks to be 2.0000-2.0400 for now with a bias to be skewed from the short side on bounces.

- The GBP/AUD Average True Range(ATR) for the last 10 Trading days: 145 Points

Fig 1: GBP/AUD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

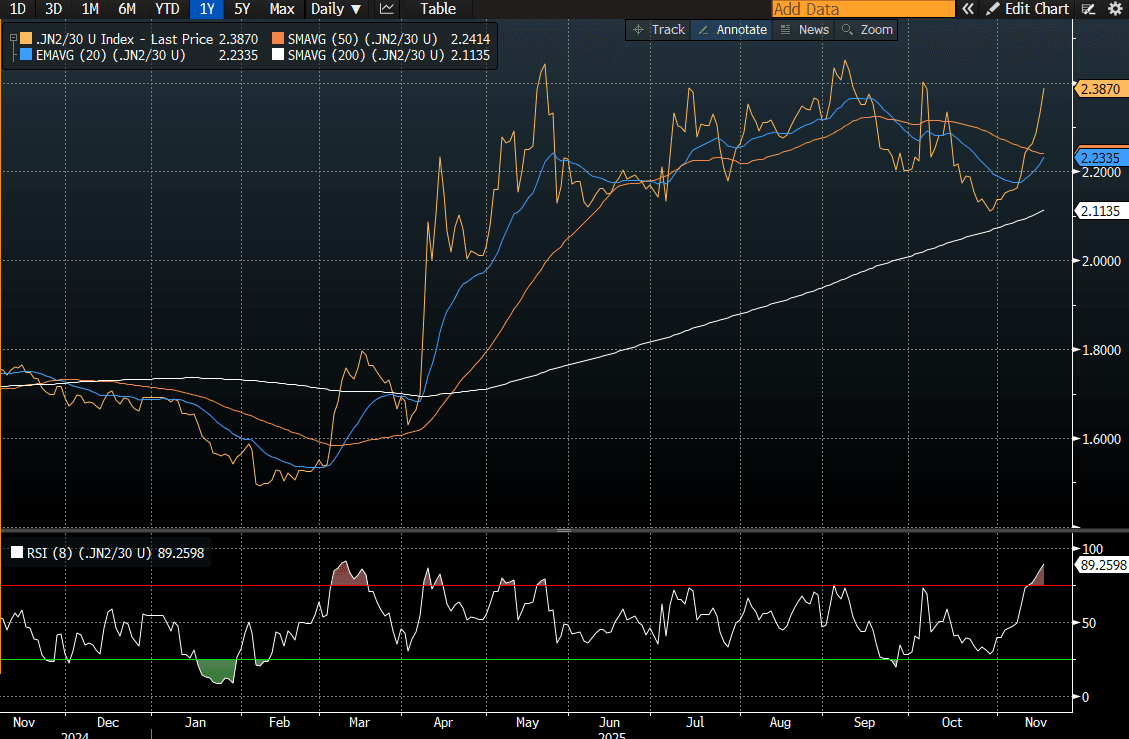

JGBS: cheaper, 2/30 YC Back Near Highs Ahead Of 20Y Supply

In Tokyo morning trade, JGB futures are weaker, -14 compared to settlement levels.

- Japan's Sep core machine orders were comfortably above market forecasts, although arguably this was a risk after the recent Q3 GDP preliminary print (which showed stronger than expected business spending in Q3). From a policymaker's standpoint, it suggests resilience/strength in the business/capex sector (reinforcing what the Q3 GDP print stated).

- Focus will be on if these trends sustain into Q4, while the wage outlook is also a key BoJ watchpoint. Our policy team notes that key wage data will not be available until the Jan policy meeting next year. This sets up a possible Dec hold from the BoJ (although sharp yen weakness could prompt a move).

- Cash US tsys are little changed in today's Asia-Pac session. Nvidia’s earnings are in focus and due after the market close on Wednesday.

- Cash JGBs are 1-2bps cheaper across benchmarks. The benchmark 20-year yield is 1.3bps higher at 2.80% versus the cycle high of 2.816%, set yesterday.

- Moreover, the 2/30 yield curve moved back to September highs. (see chart)

- Swap rates are 2bps higher to 1bp lower, with a flattening bias.

Source: Bloomberg Finance LP

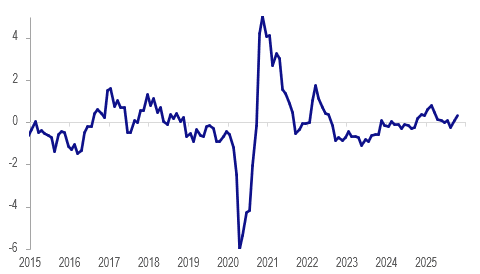

AUSTRALIA DATA: Westpac Lead Indicator Consistent With Ongoing Recovery

The Westpac leading index rose 0.11% in October up from -0.01% bringing the 6-month annualised rate to 0.35% from 0.1%. The increase was due to stronger consumer confidence. The 6-month rate leads detrended growth by 3-9 months and so is consistent with the recovery gaining into H1 2026. The index had been around neutral since April, when the US announced reciprocal tariffs.

- Westpac expects the RBA to resume easing policy in May and August next year bringing rates back to around “neutral” as there will be enough inflation data by then to show it has moderated again.

- It is forecasting growth to improve to 2.4% y/y over 2026 from Q2’s 1.8% y/y. Recently RBA Deputy Governor Hauser said that trend growth is expected to be around 2% over the rest of the 2020s. Stronger-than-expected growth is a risk to the RBA’s forecast of core inflation trending back towards the band mid-point.

- Since April, consumer sentiment, Australian equities and hours worked have driven the recovery in the lead index. There is likely to be payback for the November jump in confidence and given the size of the rally in stocks, there could be a correction.

Australia Westpac lead indicator 6m/6m annualised %

Source: MNI - Market News/LSEG