BRAZIL: Lower House Approves Bill To Cut Tax Benefits, BCB MPR Tomorrow

Dec-17 11:58

- The Brazilian real underperformed peers yesterday as mounting political uncertainty continued to dominate short-term sentiment. USDBRL rose ~0.9%, narrowing the gap to key resistance at 5.5214, the Oct 10 high. On the downside, support to watch lies at 5.2638, the Nov 11 low.

- The move came as a poll yesterday showed that President Lula leads ahead of next year’s election. Lula would receive 41% of votes, according to a survey from Genial/Quaest, while Flavio Bolsonaro would receive 23% and Sao Paulo Governor Tarcisio de Freitas 10%. Lula would also win in run-off scenarios against both.

- Meanwhile, DI swaps rates also underperformed, with yields up as much as 13bp, while local equities fell 2.4%, as the Copom minutes reinforced the hawkish lean of the committee and offered no signs that it is considering a January Selic rate cut. Most analysts see the first rate cut coming in March.

- In other news, the Lower House has approved a bill today that reduces federal tax benefits for various sectors by 10%. It also increases taxation on betting companies, which will rise from 12% to 13% in 2026, 14% in 2027, and 15% in 2028.

- No macro data are due, with focus on tomorrow’s BCB Q4 monetary policy report, in particular on the CPI forecasts for Q3 2027, which will be the policy relevant estimate for the coming Copom meetings.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Extending Highs

Nov-17 11:53

- Treasury futures extended the top end of the overnight range in the last 5 minutes, Dec'25 10Y tapped 112-24 before trading back to 112-23 (+6), 10y yield slips to 4.1173% low (-.0310).

- Treasuries last week challenged resistance at the 113-02 level, an area of congestion since Nov 5. This hurdle remains intact, however, a clear move above it would be a bullish signal and shift focus on resistance at 113-18+, the Oct 28 high. A break would also cancel a short-term bearish theme.

- The German 10Y Bund gained as well - but remains off overnight highs, Bbg US$ index firmer at 1217.70 (+1.42), stocks mildly higher (SPX eminis +19.75 at 6,775.00).

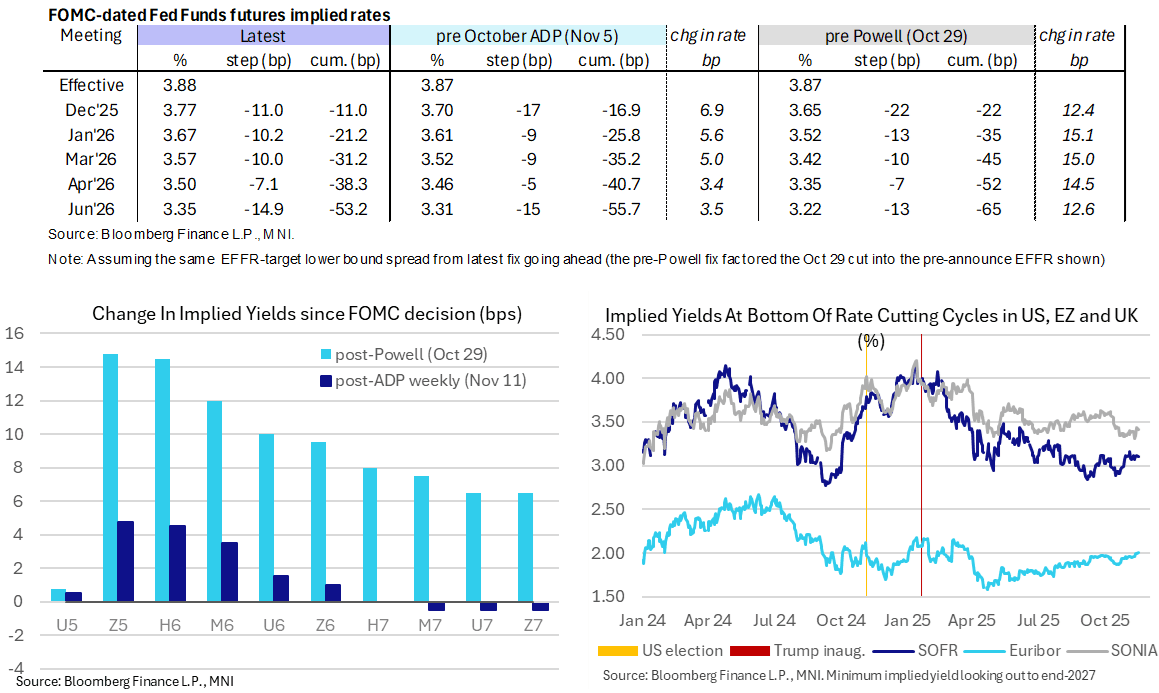

STIR: Fed December Pause Seen As ~50/50 Call As Official Data Resumes

Nov-17 11:52

- Fed Funds implied rates are unchanged from Friday’s close, holding last week’s push to a close call for December’s FOMC meeting between another 25bp cut or pausing.

- A pause is now seen as slightly more likely, supported by multiple Fed speakers with patient rhetoric.

- Cumulative cuts from an assumed 3.88% effective: 11bp Dec, 21bp Jan, 31bp Mar, 38.5bp Apr and 53bp Jun.

- SOFR futures are +0.005-0.025, with increases led by 2027 contracts.

- It sees the terminal implied yield remain within recent ranges, at 3.10% (SFRH7) between 3.06-3.16% that has been defined primarily by labor data and a strong ISM services report.

- Today’s data is light – Empire manufacturing for Nov and a delayed construction spending report for Aug – with some Fedspeak updates possibly more important (noted a little earlier). Nonfarm payrolls for September looms large on Thursday even if it is now two months old.

EURIBOR OPTIONS: Risk Reversal

Nov-17 11:50

ERM6 97.8125/98.3125RR, bought the Call for 0.75 in 8k.