INR: Low Vol Depreciation Trend Continues, CPI and FX Reserves Out Later

USD/INR sits just off record highs (90.5625 per BBG), last near 90.40/45, off around 0..05% in INR terms for the session so far. Headlines crossed a short while ago, via BBG, that the RBI was selling dollars to curb rupee losses. Controlled INR depreciation via on-going intervention is likely helping keep USD/INR volatility in check. Implied vols in the 1 month space remain very benign at 4.3%, well away from historical extremes.

- RBI's adequate FX reserve position is likely seen as a key credibility in this space. We get data for FX reserves to end Dec 5 later on. Whilst FX reserves spot are off recent cycle highs, measures of FX reserve adequacy still look firm (see this link).

- Also out later is the Nov CPI, with headline expected to tick up to 0.7%y/y, from 0.25%.

- A call between US President Trump and Indian PM Modi hasn't eased pressure in the FX space. Positive headlines emerged following the call, but at a high level rather than concrete details on trade-talk progression.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

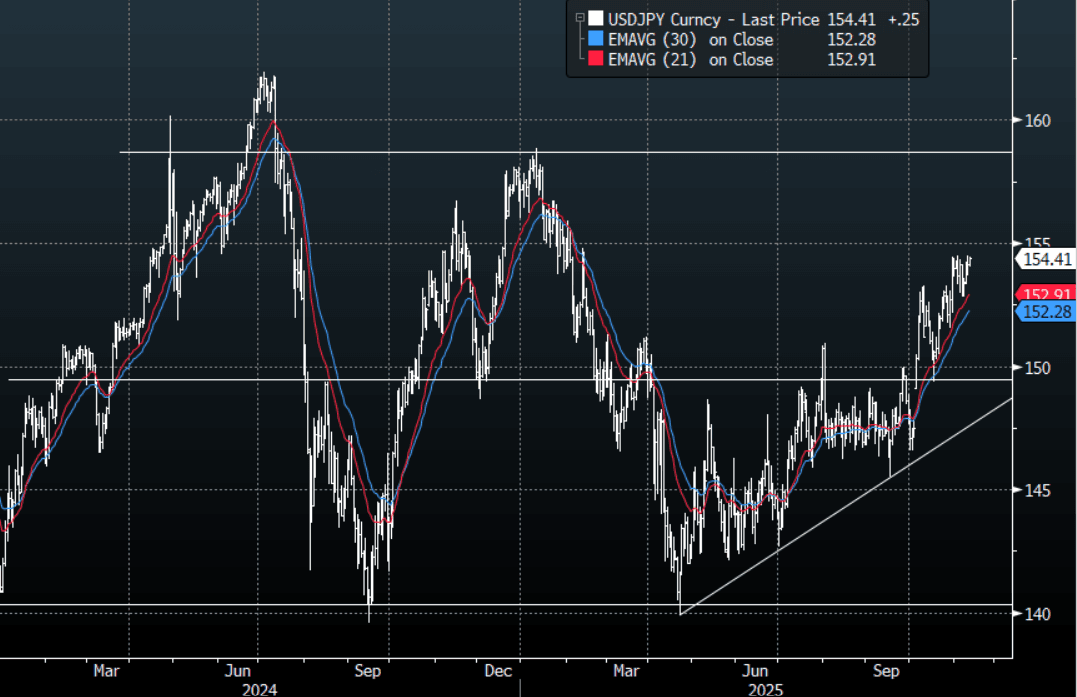

JPY: Asia-Pac: USD/JPY Moves Back To Re-Test The 154.50 Area

The USD/JPY range today has been 154.05 - 154.45 in the Asia-Pac session, it is currently trading around 154.40, +0.20%. The pair drifted higher in our session as it had another look back toward the 154.50 area. The return of a positive sentiment in risk has brought the focus in USD/JPY back to the 154-155 resistance area. A sustained break above here is needed to potentially see the uptrend regain upward momentum, through here the focus would then turn toward the 160 area where I would start to become wary of intervention risks. On the day a break above the 154.50 resistance that has capped recent moves should see it turn toward the 155.00 area. Look for dips back toward 152.00 and then the more important 149.00-150.00 area to be well supported.

- Nick Timiraos published an article in the WSJ on a fractured Fed, “Fed officials are fracturing over a December rate cut after inflation-focused hawks pushed for a pause after last month's rate reduction. Officials are divided on three questions that come down to judgment calls: Will tariff-driven cost increases truly be a one-off? Does weak hiring reflect a demand slump or reduced supply? Are rates still restrictive?”

- “The answers can lead to very different views of which poses the greater threat—persistent inflation or a sluggish labor market—and how to calibrate risk tolerance.”

- Options : Close significant option expiries for NY cut, based on DTCC data: 152.00($668m). Upcoming Close Strikes : none - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

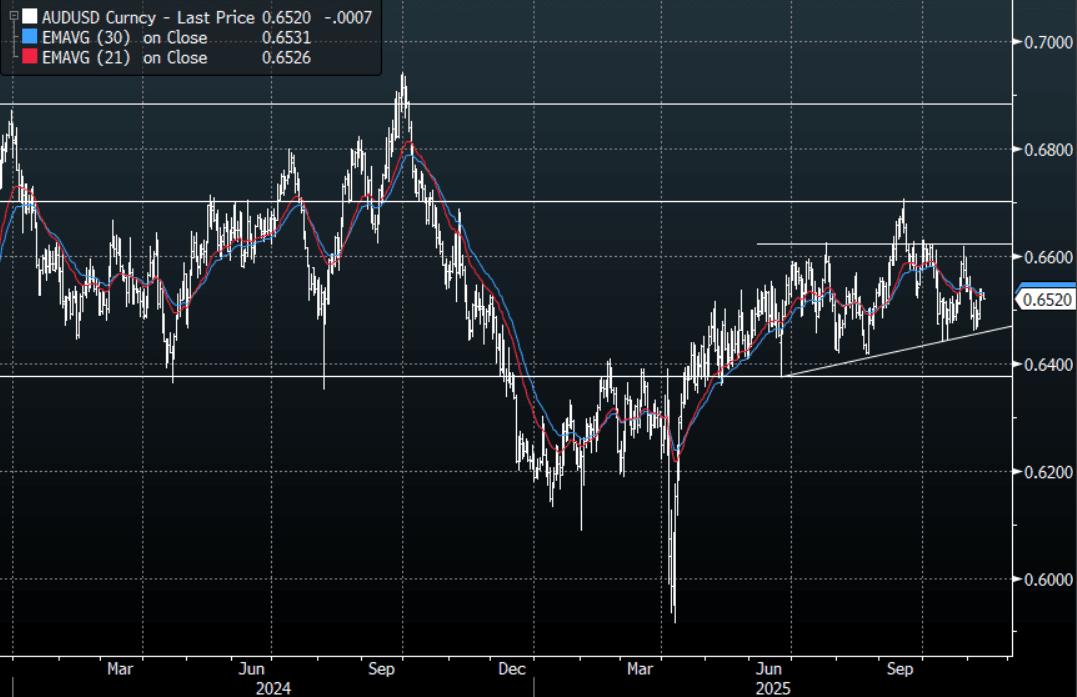

AUD: Asia-Pac: AUD/USD Drifts Lower

The AUD/USD has had a range today of 0.6520 - 0.6532 in the Asia- Pac session, it is currently trading around 0.6520, -0.10%. The AUD/USD has drifted sideways in our session consolidating its gains above 0.6500. The AUD will be one of the main beneficiaries while this positive sentiment dominates the market. The AUD/USD needs a sustained push above the 0.6550 area for the focus to turn back toward the 0.6650/0.6700 year highs. Look for intra-day dips toward 0.6480-0.6500 to be supported if this move higher is to come to fruition.

- MNI AU - Strong Home Lending May Contribute To Extended RBA Hold. The RBA noted this month that “the housing market is continuing to strengthen, a sign that recent interest rate reductions are having an effect”. The lending data is consistent with this and likely to add to its caution about easing further.

- Hauser Says RBA Debating Current Policy Stance - Per RTRS: Headlines have crossed from an Rtrs interview with RBA Deputy Governor Hauser. Rtrs notes: "A top Australian central banker said on Wednesday that there was increasing debate about whether the current cash rate of 3.6% is restrictive enough to keep inflation in check, adding that the question is critical for the policy outlook."

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD1.37b), 0.6530(AUD 939m). Upcoming Close Strikes : 0.6520(AUD852m Nov 13), 0.6750(AUD2.17b Nov 14) - BBG

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

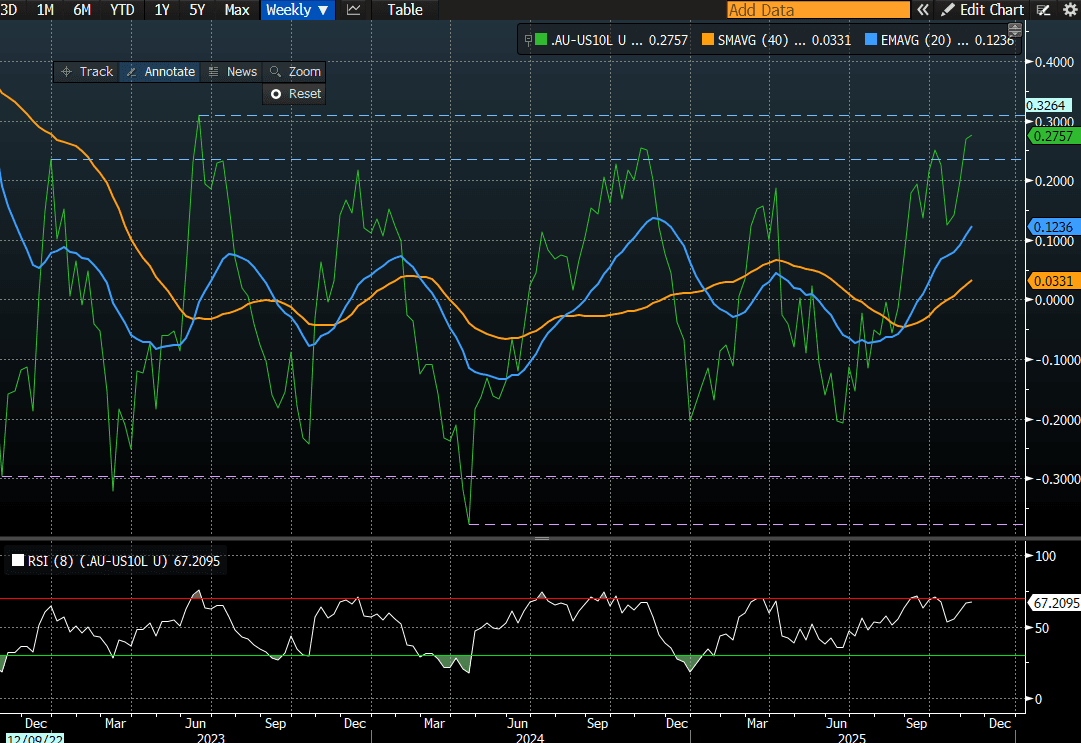

AUSSIE BONDS: Richer But AU-US 10Y Diff At Range Top Ahead Of Jobs Data

ACGBs (YM +1.5 & XM +2.0) are modestly stronger despite today’s much stronger-than-expected home loan data.

- The recovery in home lending began in Q2 after the RBA began easing in February and the 75bp to August appears to have contributed to the sharp rise.

- Cash ACGBs are 1-2bps richer with the AU-US 10-year yield differential at +29bps. At this level, investors may be tempted to position for a narrowing in the differential, as it sits near the top of its well-defined ±30bps trading range (see chart).

- However, such trades carry meaningful risk ahead of tomorrow’s October employment data. The unemployment rate rose 0.2pp to 4.5% in September.

- The unemployment rate is widely expected to normalise somewhat at 4.4% but there are a few economists who expect it to stay at 4.5% or fall back to 4.3%.

- Last month's weak employment data triggered a solid ACGB rally, but those gains were more than fully reversed after the much hotter-than-expected Q3 CPI report.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 9% probability, with a cumulative 16bps of easing priced by mid-2026.

- The AOFM plans to sell A$800mn of the 1.75% 21 November 2032 bond on Friday.

Bloomberg Finance LP