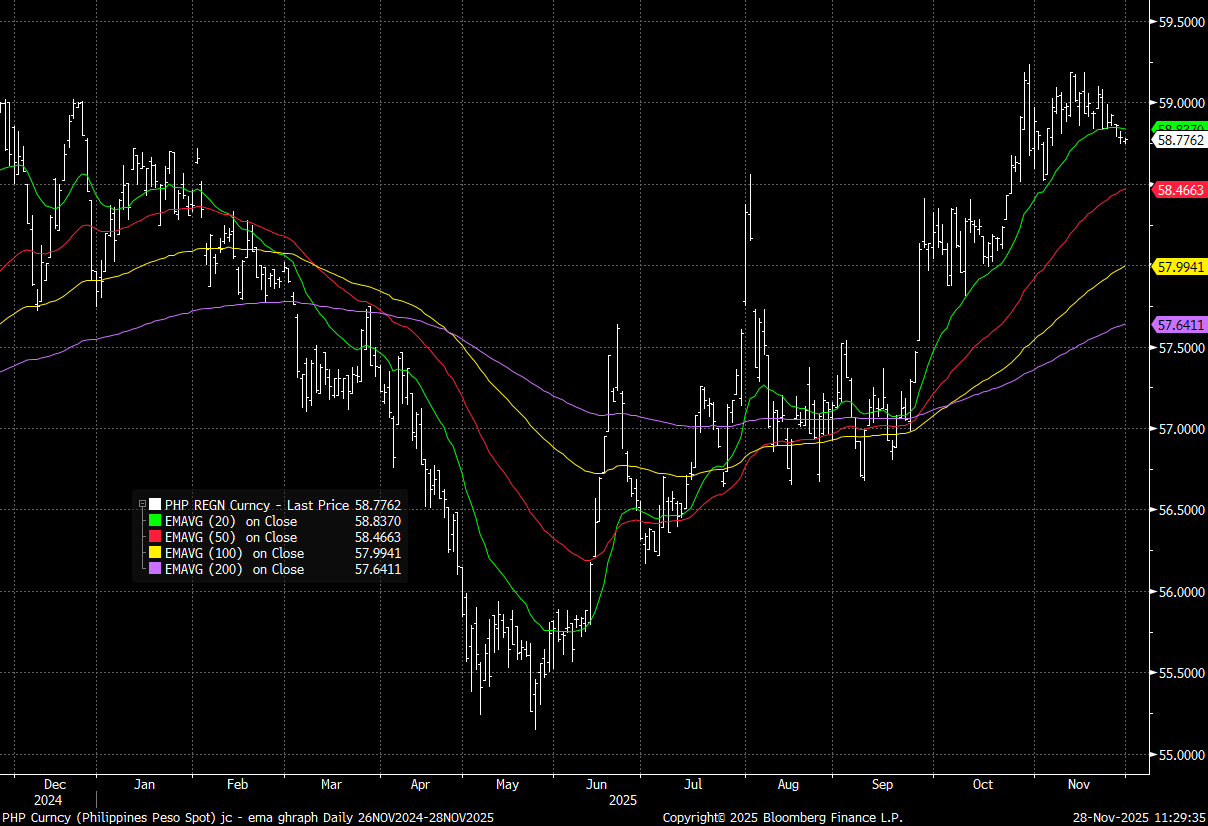

PHP: Looking To Consolidate 20-day EMA Downside Break, Govt See Q1 GDP Firmer

USD/PHP sits down a touch in the first part of Friday dealings, last near 58.75/80. This confirms the recent break under the 20-day EMA support point (around 58.835), see the chart below. We are still some distance from the 50-day EMA support point (58.47), but upside resistance between 59.00/59.20 still looks to be fairly firm at this stage. PHP has benefited recently from renewed Fed easing expectations, as the US real 10yr yield has moved back under 1.80%.

- Positive sentiment may also be filtering in from yesterday's rating affirmation from S&P (BBB+, along with a positive outlook), particularly in light of the recent flood-related fiscal spend scandal.

- The new Finance Secretary also added, via BBG: " The Philippine government has put in place a catch-up plan to manage and direct spending towards high-impact projects to stimulate growth, Finance Secretary Frederick Go says." He added growth may be back to 5.5% as soon as Q1 next year.

- On the data front, a short while ago we had the Oct trade figures, which showed better than expected export growth (19.4%y/y, versus 13.4% forecast), while imports were -6.5%y/y (against a -5.3% forecast and 5.1% prior). The weaker import picture may point to near softer economic growth pressures, but the trade deficit was narrower at -$3828mn (versus -$4400mn forecast).

- The trade deficit remains within recent ranges, but any further improvement into year end could be a PHP positive, particularly when combined with a usually stronger seasonal period for PHP (amidst remittance inflows).

Fig 1: USD/PHP Versus Key EMAs

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

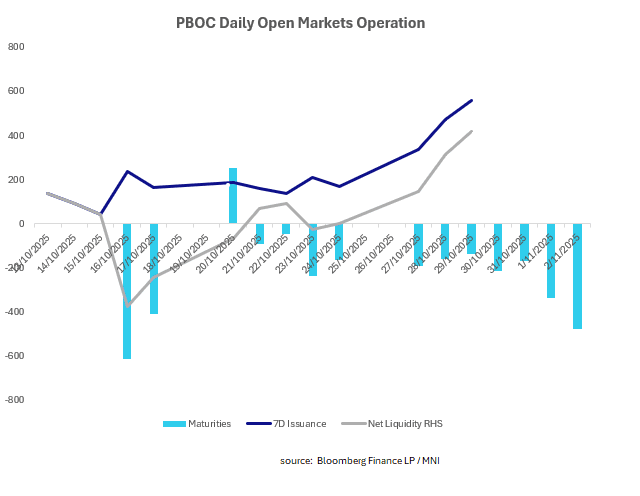

CHINA: Central Bank Injects CNY419.5bn via OMO

Ahead of a period of sizeable maturities, the PBOC issued it's largest sale of 7-day reverse repo in some time, getting ahead of upcoming maturities and continuing to keep liquidity well contained.

The CFETs 7-day weighted average index had begun to drift higher yesterday, in advance of the upcoming maturities, resulting in the increase sales during the open market operations.

Money market rates had begun to rise Monday ahead of the upcoming maturities. They have remained elevated yesterday with the O/N interbank repo rate at its highest in several weeks this morning.

- The PBOC issued CNY557.7bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY138.2bn.

- Net liquidity injection CNY419.5 bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.40%, from prior close of 1.55%, the highest since last September.

- The China overnight interbank repo rate is at 1.40%, from the prior close of 1.30%.

- The China 7-day interbank repo rate is at 1.60%, from the prior close of 1.48%.

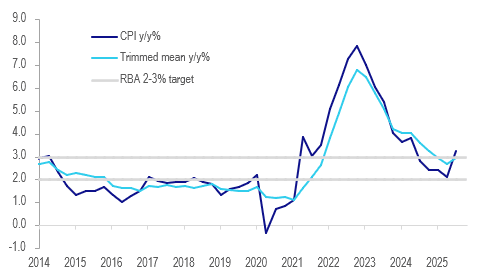

AUSTRALIA DATA: RBA Likely To Wait After Higher Core & Sticky Services Prints

Q3 CPI printed higher than expected with the underlying trimmed mean rising 1.0% q/q to be up 3.0% y/y up from 0.7% q/q (revised +0.1pp) & 2.7% y/y. In August the RBA forecast Q4 at 2.6% and now a 0.2% q/q rise is needed to achieve that which hasn’t happened since 2016 outside of Covid. Thus there is likely to be a near-term upward revision to its inflation forecasts at a minimum and given the Board’s cautious stance it looks like rates will be on hold on 4 November as it waits for more data.

Australia CPI y/y%

- The RBA also looks at the 2q/2q annualised rate, which printed at 3.4% in Q3, above the top of the 2-3% band and up from Q2’s 2.8%. At 3.0%, trimmed mean rose for the first time since Q4 2022. The quarterly rate was the highest since Q1 2024, when policy was being tightened.

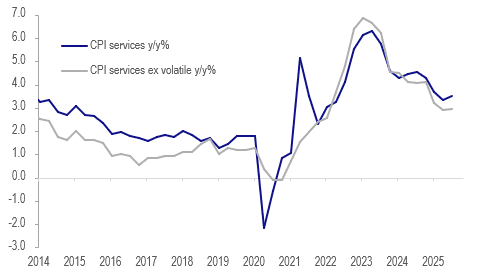

- Governor Bullock sounded worried about services inflation in September given trends in the July/August data and stickiness overseas. Australia’s headline services rose 1.3% q/q and 3.5% y/y up from Q2’s 3.3% due to rents and medical services. Market services also increased 1.3% q/q, in line with Q3 2023 & 2024, leaving the annual rate at 2.9% - both quarterly & annual rates tentatively suggest stickiness in Australia too.

- Headline continues to be impacted by government electricity rebates and jumped 1.3% q/q & 3.2% y/y in Q3 up from Q2’s 0.7% & 2.1%. The ABS noted that electricity prices rose 9% q/q. Other contributors to the quarterly CPI rise were housing (+2.5%), recreation (+1.9%) and transport (+1.2%).

- There are a lot of key data before the December meeting which the RBA may want to wait for, including October jobs on 13 November, Q3 wages 19 November, October CPI 26 November (first full sample monthly CPI) and Q3 GDP 3 December.

Australia services CPI y/y%

Source: MNI - Market News/LSEG

MNI: CHINA PBOC CONDUCTS CNY557.7 BLN VIA 7-DAY REVERSE REPO WEDS

- CHINA PBOC CONDUCTS CNY557.7 BLN VIA 7-DAY REVERSE REPO WEDS