SOUTH AFRICA: Local News Flow Light Over Shortened Trading Day

- Local markets close early today at 09:50GMT/11:50SAST, and will remain shut tomorrow on New Year’s Day. Trade balance data for November is due at 12:00GMT/14:00SAST (Prior: ZAR 15.6bn).

- Eskom has recorded a 40% increase in outages over the festive season, primarily driven by severe weather conditions. The group has warned that the adverse weather is expected to continue into 2026, with heavy rainfall expected through March. Despite the sharp spike in weather-related service interruptions, Eskom says it has not experienced significant outages at its power stations in the affected provinces.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US 10YR FUTURE TECHS: (H6) Corrective Pullback

- RES 4: 114-00 Round number resistance

- RES 3: 113-29+ High Oct 17 and a key resistance

- RES 2: 113-23 High Oct 23

- RES 1: 113-22+ High Nov 25

- PRICE: 113-08 @ 07:30 GMT Dec 1

- SUP 1: 113-01 20-day EMA

- SUP 2: 112-37 50-day EMA

- SUP 3: 112-10+ Low Nov 20

- SUP 4: 112-07 Low Nov 5 and a key support

A bullish theme in Treasuries remains intact despite the latest pullback. The recent breach of the 112-31 level, an area of congestion since Nov 5, marks an important short-term bullish development. Note that the contract is also trading above the 20- and 50- EMAs. A resumption of gains would open 113-29+, the Oct 17 high and a key resistance. On the downside, initial support to watch is at 113.01, the 20-day EMA.

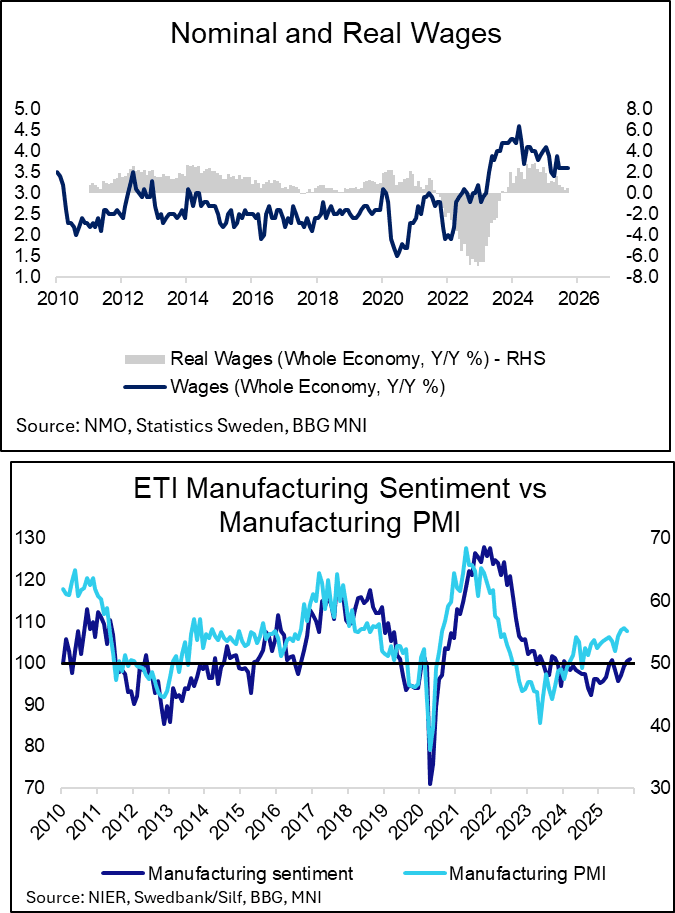

SWEDEN: Wage and Manufacturing PMI Data Consistent With A Cyclical Recovery

This morning’s Swedish data were consistent with the ongoing narrative around an economic recovery. The Riksbank is firmly expected to be on hold at 1.75% for "some time", but today's readings add to the stock of data suggesting medium-term risks to rates are tilted towards hikes.

Real wage growth remains positive, which is expected to support household consumption through the end of 2025 and into 2026.

- Whole-economy nominal wage growth was estimated at 3.2% Y/Y in September, while the National Mediation Office’s (NMO) adjustment to account for retroactive payments predicted growth of 3.6% Y/Y.

- This implied whole-economy real wage growth of 0.5% Y/Y (vs 0.4% prior).

- Private sector wages were estimated at 3.3% Y/Y (vs 3.3% prior), with the NMO’s adjustment predicting growth of 3.5% Y/Y (vs 3.6% prior).

- In the public sector, the NMO’s adjustment played a larger role, with wage growth predicted at 3.9% Y/Y based on an original estimate of 3.2% Y/Y.

The November manufacturing PMI remained comfortably in expansionary territory at 54.6 (vs 55.0 prior). The three analyst estimates submitted to Bloomberg were 55.0, 55.1 and 55.5.

- New orders rose back to 56.7 (vs 55.8 in Oct, 57.7 in Sept), while production eased to 57.6 (vs 60.5 prior). Employment rose to 51.6 (vs 50.9 prior), while future production remained elevated at 66.7 (vs 70.1 prior).

EQUITY TECHS: E-MINI S&P: (Z5) Holding On To The Bulk Of Its Recent Gains

- RES 4: 6953.75 High Oct 30 and bull trigger

- RES 3: 6900.50 High Nov 12

- RES 2: 6852.56 76.4% retracement of the Oct 30 - Nov 21 bear leg

- RES 1: 6863.75 High Nov 28

- PRICE: 6809.50 @ 07:22 GMT Dec 1

- SUP 1: 6674.50/6525.00 Low Nov 25 / 21

- SUP 2: 6500.00 Round number support

- SUP 3: 6476.62 23.6% retracement of the Apr 7 - Oct 30 uptrend

- SUP 4: 6427.00 Low Sep 2

S&P E-Minis are holding on to the bulk of their latest gains following the recovery from the Nov 21 low. The climb has resulted in a breach of the 20- and 50- day EMAs. This highlights a bullish development and the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would signal scope for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low.