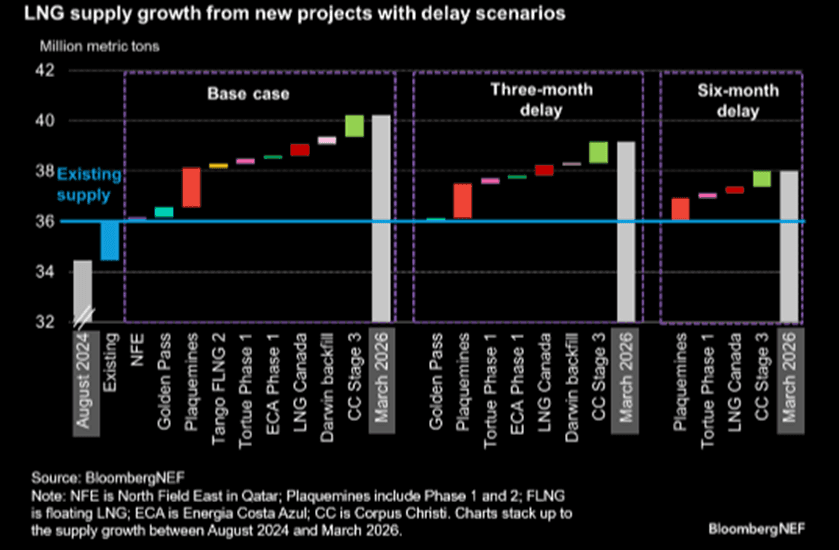

LNG: Six Month LNG Project Delays Could Halve Additional Supply in 2025

Sep-27 15:11

New LNG supply next year could more than halve from 22.8m tons additional supply to 9.3m tons if upcoming projects are delayed by six months as several assets have already pushed back timelines, according to BNEF.

- Nine projects are expected to come online between October 2024 and March 2026 with equivalent to 8% of total global supply last year.

- Longer commissioning could lower production ramp-up rates and reduce cargo loading estimates.

- Venture Global’s Plaquemines Phase 1 is anticipated to start in November, Cheniere Energy’s Corpus Christi Stage 3 in December and BP’s Tortue floating LNG project is aiming for an end-of-year start.

- Other projects possible for mid to late next year are Shell’s Canada LNG project, Sempra’s Energia Costa Azul in Mexico, Darwin LNG restart and Golden Pass.

Source: BNEF

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Little Changed, Futures Stick Within Yesterday’s Range

Aug-28 15:04

Futures (Z4) have stuck with yesterday’s range, last -6 at 98.74.

- Yields little changed to 1bp higher.

- Gilts have followed the lead of wider core global FI markets today.

- The initial rally came alongside some weakness in crude oil.

- A move away from session highs was then seen as EGBs came under some hedging pressure stemming from pricing of some large EUR IG/sovereign deals.

- A panel appearance from BoE hawk Mann failed to generate headlines.

- We suggested this may be the case ahead of time, as there was no livestream of the event. A recording of the discussion will be released at some point, although we don’t have a firm time.

- BoE-dated OIS pricing has been sticky, showing just under 40bp of cuts through the Dec MPC at typing.

- Recent BoE communique has remained non-committal when it comes to the idea of follow up easing, providing some hawkish impetus for GBP STIRs.

- The local calendar is empty on Thursday, with participants looking ahead to the release of DMO’s quarterly issuance calendar on Friday.

| BoE Meeting | SONIA BoE-Dated OIS (%) | Difference Vs. Current Effective SONIA Rate (bp) |

| Sep-24 | 4.911 | -3.9 |

| Nov-24 | 4.697 | -25.3 |

| Dec-24 | 4.559 | -39.2 |

| Feb-25 | 4.361 | -58.9 |

| Mar-25 | 4.222 | -72.9 |

| May-25 | 4.059 | -89.1 |

| Jun-25 | 3.966 | -98.4 |

STIR: Limited Moves In ECB Pricing Today, ES/DE Inflation and Lane Eyed Tomorrow

Aug-28 14:49

EUR STIRs have largely tracked wider core FI through today, with ECB-dated OIS pricing 66bps of easing through the remainder of this year (vs 65bps this morning). Tomorrow’s focus is on flash inflation data from Spain and Germany, alongside panel appearances from ECB’s Lane and Nagel.

- Tomorrow’s inflation data will feed into the Eurozone-wide release on Friday. Our full inflation preview is here: https://roar-assets-auto.rbl.ms/files/66994/August2024EZCPIPreview.pdf

- Markets will be watchful of any policy signals from ECB Chief Economist Lane, who did not give explicit policy signals at his Jackson Hole speech on Saturday. Nevertheless, it is likely safe to assume that he supports a 25bp cut at the Sep 12 meeting, alongside many other Governing Council members.

- Euribor futures are flat to +3.0 ticks through the blues, off intraday highs alongside Bunds at typing.

| Meeting Date | ESTR ECB-Dated OIS (%) | Difference Vs. Current Effective ESTR Rate (bp) |

| Sep-24 | 3.415 | -25.0 |

| Oct-24 | 3.291 | -37.4 |

| Dec-24 | 3.005 | -66.0 |

| Jan-25 | 2.822 | -84.3 |

| Mar-25 | 2.585 | -108.1 |

| Apr-25 | 2.457 | -120.8 |

| Jun-25 | 2.292 | -137.4 |

| Jul-25 | 2.220 | -144.5 |

| Source: MNI/Bloomberg. | ||

US EIA: CRUDE OIL STOCKS EX SPR -0.85M TO 425.2M AUG 23 WK

Aug-28 14:30

- US EIA: CRUDE OIL STOCKS EX SPR -0.85M TO 425.2M AUG 23 WK

- US EIA: DISTILLATE STOCKS +0.28M TO 123.1M IN AUG 23 WK

- US EIA: GASOLINE STOCKS -2.2M TO 218.4M IN AUG 23 WK

- US EIA: CUSHING STOCKS -0.67M TO 27.5M BARRELS IN AUG 23 WK

- US EIA: SPR +0.74M TO 377.9M BARRELS IN AUG 23 WK

- US EIA: REFINERY UTILIZATION WEEK CHANGE +1% TO 93.3% IN AUG 23 WK

Trending Top

May-29 20:10