EM ASIA CREDIT: LG Chem (LGCHM): LG Energy stake to be monetised

(Baa2/BBB/-)

"*LG CHEM TO MAINTAIN OWNERSHIP OF LG ENERGY AT AROUND 70% LEVEL" - BBG

"*LG CHEM TO GRADUALLY UTILIZE LG ENERGY STAKE OVER LONG-TERM" - BBG

LG Energy stake to be monetised overtime, shareholders main beneficiaries, neutral read for now.

LG Chem currently owns around 79% of LG Energy Solution and indicated in a filing that this could fall to roughly 70%. The company has not provided guidance on the planned use of proceeds, although activist shareholder Palliser Capital, which recently disclosed a stake of just over 1% in LG Chem, has urged management to deploy part of the LG Energy Solution stake to fund share buybacks.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Futures Down Post Bessent BoJ Comments, 2/30s Curve Continues To Flatten

JGB futures hold weaker, last at 136.04, -.18 versus settlement levels. Negative spill over has been evident from comments made by US Tsy Secretary Bessent (via X: "The Government’s willingness to allow the Bank of Japan policy space will be key to anchoring inflation expectations and avoiding excess exchange rate volatility."), along with a sharp fall in Aussie bond futures (post the CPI beat), have been factors in play. We haven't broken sub 136.00 yet, while recent highs above just above 136.30.

- In the cash JGB space, firmer yield trends are evident for the belly of the curve, with 5-7yr up more than 1bps, like wise for the 1yr (although liquidity is poorer at this benchmark).

- The 10yr is higher, but 20-40yrs are softer in yield terms, off close to 2bps, the 30yr under 3.05% is back challenging 100-day EMA support. These moves are seeing the 2/30s curve flattening trend continue, now +210bps.

- Bessent's earlier remarks also helped push USD/JPY lower. Bessent is essentially arguing, in our view, the government shouldn't push back on BoJ normalizing policy, as if they do it risks slipping behind the inflation curve.

- Market pricing for tomorrow's meeting outcome is a touch firmer, but still only +5bps of hike risks priced in. A full hike is not priced in until around March next year.

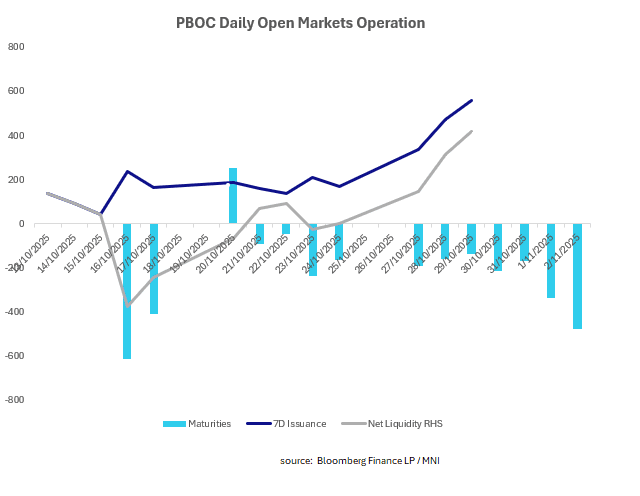

CHINA: Central Bank Injects CNY419.5bn via OMO

Ahead of a period of sizeable maturities, the PBOC issued it's largest sale of 7-day reverse repo in some time, getting ahead of upcoming maturities and continuing to keep liquidity well contained.

The CFETs 7-day weighted average index had begun to drift higher yesterday, in advance of the upcoming maturities, resulting in the increase sales during the open market operations.

Money market rates had begun to rise Monday ahead of the upcoming maturities. They have remained elevated yesterday with the O/N interbank repo rate at its highest in several weeks this morning.

- The PBOC issued CNY557.7bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY138.2bn.

- Net liquidity injection CNY419.5 bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.40%, from prior close of 1.55%, the highest since last September.

- The China overnight interbank repo rate is at 1.40%, from the prior close of 1.30%.

- The China 7-day interbank repo rate is at 1.60%, from the prior close of 1.48%.

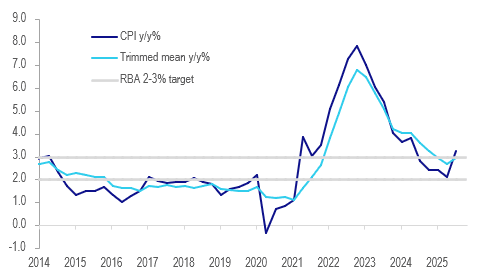

AUSTRALIA DATA: RBA Likely To Wait After Higher Core & Sticky Services Prints

Q3 CPI printed higher than expected with the underlying trimmed mean rising 1.0% q/q to be up 3.0% y/y up from 0.7% q/q (revised +0.1pp) & 2.7% y/y. In August the RBA forecast Q4 at 2.6% and now a 0.2% q/q rise is needed to achieve that which hasn’t happened since 2016 outside of Covid. Thus there is likely to be a near-term upward revision to its inflation forecasts at a minimum and given the Board’s cautious stance it looks like rates will be on hold on 4 November as it waits for more data.

Australia CPI y/y%

- The RBA also looks at the 2q/2q annualised rate, which printed at 3.4% in Q3, above the top of the 2-3% band and up from Q2’s 2.8%. At 3.0%, trimmed mean rose for the first time since Q4 2022. The quarterly rate was the highest since Q1 2024, when policy was being tightened.

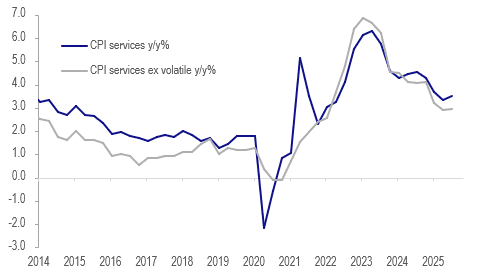

- Governor Bullock sounded worried about services inflation in September given trends in the July/August data and stickiness overseas. Australia’s headline services rose 1.3% q/q and 3.5% y/y up from Q2’s 3.3% due to rents and medical services. Market services also increased 1.3% q/q, in line with Q3 2023 & 2024, leaving the annual rate at 2.9% - both quarterly & annual rates tentatively suggest stickiness in Australia too.

- Headline continues to be impacted by government electricity rebates and jumped 1.3% q/q & 3.2% y/y in Q3 up from Q2’s 0.7% & 2.1%. The ABS noted that electricity prices rose 9% q/q. Other contributors to the quarterly CPI rise were housing (+2.5%), recreation (+1.9%) and transport (+1.2%).

- There are a lot of key data before the December meeting which the RBA may want to wait for, including October jobs on 13 November, Q3 wages 19 November, October CPI 26 November (first full sample monthly CPI) and Q3 GDP 3 December.

Australia services CPI y/y%

Source: MNI - Market News/LSEG