US TSYS: Late SOFR/Treasury Option Roundup: Better Calls as Curve Bear Steepen

SOFR & Treasury option flow segued from downside put structures to calls as underlying curves bear steepen, modest overall volumes. Projected rate cut pricing hold steady to mildly firmer vs. late Thursday levels (*): Jan'26 steady at -6.1bp, Mar'26 at -14bp (-13.2bp), Apr'26 at -20.6bp (-19.6bp), Jun'26 at -33.3bp (-33.3bp).

- SOFR Options:

- -4,000 SFRH6 96.37/96.50/96.62/96.75 call condors, 3.75

- Pit/screen +30,000 SFRH6 96.37/96.50/96.62/96.75 call condors, 3.5

- +20,000 SFRH6 96.12 puts, 0.5

- +10,000 SFRH6 96.25 puts, 0.75

- +10,000 SFRH7 97.25 calls, 19.0 ref 96.835

- +5,000 SFRM6 97.00/97.50 call spds, 4.5

- 6,600 SFRH6 96.37/96.43/96.50 put trees ref 96.455 to -.45

- -2,000 SFRG6 96.43/96.56 1x2 call spds, 0.5 vs. 96.455/0.08%

- 1,250 SFRZ5 96.12/96.18/96.25/96.31 call condors ref 96.29

- 8,455 SFRF6 96.37/96.43 2x1 put spds, 1.0 ref 96.455

- 1,000 0QG6 96.43/96.68/96.93/97.06 broken put condors ref 96.835

- 2,000 SFRG6 96.25/96.37/96.43/96.50 broken put condors, 1.0 ref 96.46

- 2,000 SFRG6 96.18/96.43/96.56/96.68 broken put condors, 4.0 ref 96.46

- Treasury Options:

- -2,500 USH6 113/115 2x1 put spds, 20

- 1,300 FVH6 108 puts ref 109-04.75

- -4,000 TYF6 113 calls, 9-10

- over 6,900 TYF6 112.75 calls, 17 last

- over 5,600 USH6 113 puts, 102 ref 115-04

- -2,800 FVH6 109.5/110 call spds, 10.5 ref 109-05.75

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURJPY TECHS: Fresh Cycle High

- RES 4: 180.37 1.500 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 3: 180.00 Psychological round number

- RES 2: 179.73 1.382 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 1: 179.45 High Nov 12

- PRICE: 179.19 @ 17:19 GMT Nov 12

- SUP 1: 177.05/175.52 20- and 50-day EMA values

- SUP 2: 174.82 Low Oct 17

- SUP 3: 173.98 Bull channel support drawn from the Feb 28 low

- SUP 4: 173.92 Low Oct 6 and a gap high on the daily chart

The trend in EURJPY remains bullish and today’s gains reinforce current conditions. The cross has cleared the bull trigger at 178.82, the Oct 30 high, to confirm a resumption of the medium-term uptrend. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 179.73, a Fibonacci projection, and the 180.00 psychological handle. First support lies at 177.05, the 20-day EMA.

COMMODITIES: Crude Falls Amid Oversupply Concerns, Precious Metals Rally

- Crude has fallen sharply today amid oversupply concerns after OPEC flipped its Q3 view to a surplus.

- WTI Dec 25 is down by 4.3% at $58.4/bbl.

- The November OPEC Monthly Oil Market report showed a switch from a deficit to a surplus of 500kb/d in Q3 as US production exceeded expectations.

- Excess oil supply driven by increased OPEC and non-OPEC output also remains in focus, while uncertainty remains over the impact of the latest sanctions on Russia.

- With today’s move, price has fallen below initial support at $58.83, the Nov 6 low, narrowing the gap to key support and the bear trigger at $55.96, the Oct 20 low.

- Meanwhile, spot gold has risen by a further 1.7% to $4,197/oz on Wednesday, taking it to its highest level since Oct 21.

- The move comes ahead of a US House vote to end the government shutdown this evening. A final vote is expected at around 1900ET(0000GMT).

- Today’s rally in gold has seen price rise above initial resistance at $4,161.4, the Oct 22 high. A stronger recovery would refocus attention on $4,381.5, the Oct 20 high and bull trigger.

- Elsewhere, silver has also jumped by 4.4% to $53.5/oz, taking the precious metal to its highest since Oct 17, when it reached an all-time high of $54.48.

- Trend signals in silver remain bullish and a clearance of this record high would open $55.444, a Fibonacci projection point.

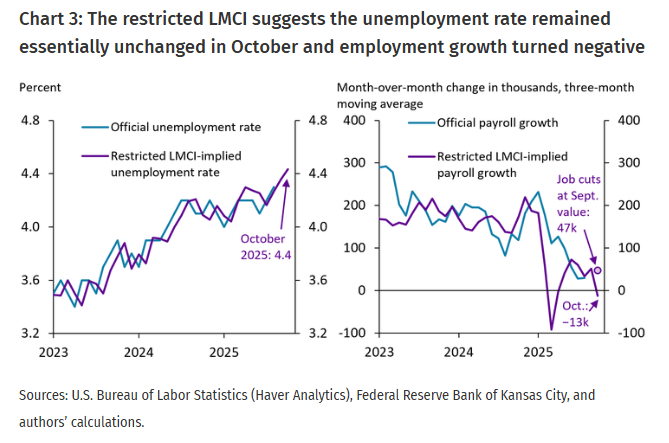

US DATA: KC Fed’s Alternative Labor Index Echoes Steady U/E Rate Increase

- Updated for October two days ago, we add the “Alternative Version” of the KC Fed’s Labor Market Conditions Index (LMCI) to the broad list of labor indicators we have focused on for labor market clues under the government shutdown. Atlanta Fed's Bostic today described it as one of his favorite gauges of the labor market.

- This Alternative Version, which excludes delayed government series, “suggests little change in the labor market, but a deceleration in labor market momentum caused by a high number of announced job cuts [in the Challenger report]. This has pushed down our model's forecast of payroll employment growth for October.”

- This restricted model points to an unemployment rate of 4.4% in October, broadly chiming with the 4.36% from the Chicago Fed’s unemployment rate nowcast for a very mild deterioration from the 4.32% reported in latest BLS data for August.

- It also sees the economy losing an average of 13k jobs per month from Aug-Oct, “driven entirely by the aforementioned announced job cuts in October”.

- We see a high likelihood of the delayed September payrolls report being released between Friday to early next week although the White House has called into question whether the October jobs report will be published.

- See the MNI US Shadow Employment Report here, noting that it was published prior to Tuesday’s slide in the weekly ADP series (see US DATA: Weekly ADP Series Rolls Over – Nov 11, 1016ET).