US TSYS: Late SOFR/Treasury Option Roundup

Volumes gradually picked up Wednesday, SOFR/Treasury options remained mixed. Underlying Tsy futures modestly higher (TYZ5 113-26 +2) while SOFR futures trade mixed. Projected rate cut pricing at/near steady vs. late Tuesday levels (*): Oct'25 at -24.7bp (-24.2bp), Dec'25 at -49.1bp (-49.2bp), Jan'26 at -64.2bp (-64.2bp), Mar'26 at -78.2bp (-78.2bp).

- SOFR Options:

- +4,000 SFRZ5 96.12/96.25 put spds, 2.0 ref 96.375

- +5,000 SFRZ5 95.87/96.00/96.06/96.12 broken put condors, cab

- +5,000 2QX5 97.06/97.25 call spds, 4.0 ref 96.99

- +5,000 SFRH7 97.50/98.00 call spds, 11 ref 97.095

- -5,000 SFRH6 96.50/0QM6 96.62 put strip, 20.0

- +5,000 0QZ5 96.87/97.00 put spds 1.25 over SFRZ5 96.31 put

- +6,000 SFRZ5 96.18/96.25/96.31/96.37 call condors, 1.75

- +5,000 SFRH6 96.75/96.87/97.00/96.12 call condors, 1.75 ref 96.63

- +5,000 SFRX5 96.12/96.25 2x1 put spds, 0.75

- -5,000 SFRZ5 96.25/96.37/96.50/96.62 call condors, 7.25

- +10,000 0QU6 98.00 calls, 7.5

- Block/screen, +100,000 SFRH6 96.31/96.37 put spds, 1.5 vs. 96.625 to -.64/0.06% (Mar'26 options expire March 13, 2026 - the Friday before the FOMC policy annc on March 18.

- 2,500 SFRH6 96.43/96.62/96.68 put trees

- Treasury Options:

- +20,000 FVZ5 110.5/111.5 call spds, 10

- -15,000 TYZ5 114/116 call spds, 28

- Update over -45,000 TYZ5 114 calls, 33 vs. 113-22/0.42% appr 5.03% vol

- 1,150 USF6 118/119/120 call flys

- 1,500 TYX5 112.5/113/113.25/114.25 broken call condors

- 2,500 TYZ5 118 calls, ref 113-24.5

- -1,500 TYZ5 118/121 call strips, 3 vs. 113-22/0.10%

- -3,800 TUZ5 103.5/104/104.37 broken put flys, 5 vs 104-14.87/0.18%

- +5,000 USZ5 123/125 1x2 call spds, 1 net vs. 119-08 to\ -09

- -2,000 TYX5 110.25 calls, 2.5-2.0

- -2,500 TYZ5 114 calls, 35

- 4,000 TYX5 113 puts, 1 last

- 2,500 TYX5 114/114.25 call spds vs, 6 vs. 114-00/0.14%

- 8,000 TYX5 112.5 puts, 1 ref 113-17/0.05%

- over 7,000 Wed wkly 10Y 113.5 puts, expire today

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Musalem Notes Market Expectations For QT Runoff To End In H1 2026

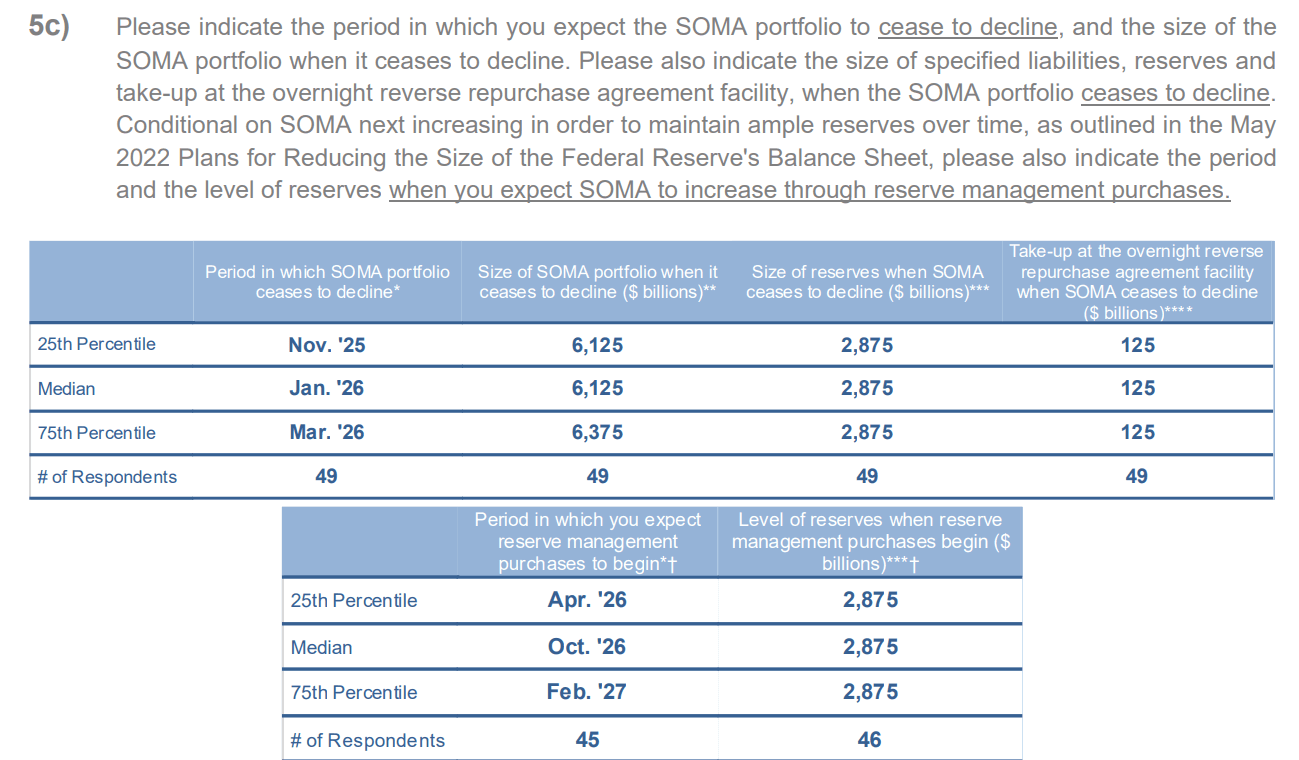

St Louis Fed President Musalem echoed his colleagues Monday that the Fed still sees reserves as "abundant", though highlighted market expectations of an end to QT in H1 2025:

- "The New York [Fed] monitors very carefully whether we are still in an abundant reserves situation, and they publish many indicators that suggest that we are still in an abundant reserve situation. Our balance sheet has been declining gradually. We reduced the rate of rolloff earlier this year, so it's declining gradually. I would expect at some point in the future the committee to make a decision before we, or as we, feel that we are reaching that transition point between abundant reserves and ample reserves to - at that point - potentially pause the balance sheet rolloff. I've seen some market surveys that suggest - and these are not, the committee still needs to decide - but I've seen market surveys that suggest that could happen somewhere in Q1 or Q2 of next year, and could happen at around $2.9 trillion in reserves, plus overnight RRP."

- He may be referencing the NY Fed's Survey of Market Expectations - the latest edition of which is July's. That showed a median expectation for the SOMA portfolio's decline to cease in January 2026, with reserves at $2.875T and ON RRP at $125B for a total $3T.

- That was at the beginning of the Treasury's post-debt limit cash rebuilding process and may be due an update. The deadline for the latest questionnaire (September) was two weeks ago, and the results should be released the same day as the September FOMC Minutes - Oct 8.

- While Fed Chair Powell suggested last week the FOMC remains comfortable with the pace of QT, as he notes they are inevitably "getting closer" to an "ample" reserve level. In the latest week, reserves fell $131B, and over the last 4 weeks have fallen $277B. With reverse repo facility takeup nearing zero, that leaves reserves + ON RRP at just above $3T ($3.034T) as of last Wednesday. That was the lowest since November 2020 and very close to the $3.0T implied by the NY Fed's survey.

- Musalem also commented that QE shouldn't combine cooperation with Treasury: "I think it's very important to only use QE to support the dual mandate and to not be perceived as direct or indirectly, be helping with debt management responsibilities."

US TSYS: Late SOFR/Treasury Option Roundup: Large 10Y Call Volume

Large Tsy 10Y call buying highlight of Monday's FI option trade. Underlying futures mildly weaker, near late session lows. Projected rate cut pricing near flat vs. early morning levels (*): Oct'25 at -22.3bp (-22.9bp), Dec'25 at -43.1bp (-44.6bp), Jan'26 at -54.1bp (-56.2bp), Mar'26 at -66bp (-69.1bp).

- SOFR Options:

- -3,000 0QZ5 97.37 calls, 5.0 vs. 96.985/0.18%

- +17,000 SFRV5 96.31 calls, 5.5 vs. 96.33/0.56% (adds to +5k earlier at 5.0)

- -6,000 SFRV5 96.31 calls, 5 vs. 96.33/0.62%

- 2,000 SFRZ5 96.00/96.12/96.25 put flys, 2.5

- 3,000 SFRV5 96.37/96.73/96.50 call trees, 0.75 ref 96.37

- 1,250 SFRZ5 96.37/96.50 call spds vs. 96.12/96.25 put spds ref 96.345

- 1,000 SFRV5 96.37/96.43 call spds vs. 0QV5 97.00/97.06 call spds

- 2,750 SFRH6 95.86/96.06/96.25 put flys, ref 96.57

- 3,000 SFRZ5 95.62/95.75 2x1 put spds ref 96.345

- Treasury Options:

- over 7,500 TYX5 113.5/114.5/115.5 1x3x2 call flys, 2 net on the package (total volume 114.5 call over 40k)

- over +155,000 TYV5 114 calls, 31-33 ref 112-27 to -24.5

- 8,197 USV5 117 calls, 13

- 3,000 TYV5/Wed wkly TY 112 put spd on a 1x2 put spds

- 1,500 FVV5 109/109.25 2x1 put spds ref 109-16.5

- 1,800 TYZ5 113 straddles vs. TYX5 112/114 strangles (1x3 ratio)

- 2,400 TYX5 110.5 puts ref 112-26

- 3,800 TYZ5 113 calls ref 112-26.5 to -25.5

- 2,000 FVV5 109.5 calls, 8.5 ref 109-14.25

- 1,000 USV5 114.5/115.5 2x3 put spds ref 116-08

- 2,000 TYV5 112.25 puts, 5 ref 112-23

AUSSIE 10-YEAR TECHS: (Z5) Bull Cycle Intact

- RES 3: 95.995 - 1.618 proj of the Sep 3 - 9 - 10 price swing

- RES 2: 95.865 - 1.000 proj of the Sep 3 - 9 - 10 price swing

- RES 1: 95.780 - High Sep 12, 18 and 19

- PRICE: 95.685 @ 19:09 BST Sep 22

- SUP 1: 95.510 - Low Sep 3

- SUP 2: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 3: 95.275 - Low Nov 14 (cont) and a key support

A short-term bull cycle in Aussie 10-yr futures remains in play and the latest pullback is considered corrective. Near-term resistance to watch is 95.780 high, the Sep 12 high. A clear break of this level would signal scope for a continuation higher and open 95.865, a Fibonacci projection. On the downside, key short-term support has been defined at 95.510, the Sep 3 low. Clearance of this level would instead be bearish.